Fed funds futs are showing an 87.5% probability of a 75 bps hike going into the FOMC decision tdy at 2 pm ET.

At this time during prior meetings the futs were showing 100 or high 90s % probability of a 75 bps hike.

Do traders reflecting the 12.5% know sth we don't?

#Fed

1/8

At this time during prior meetings the futs were showing 100 or high 90s % probability of a 75 bps hike.

Do traders reflecting the 12.5% know sth we don't?

#Fed

1/8

Can the #Fed opt for 50 instead of 75?

#nikileaks tweeted the #Fed is thinking about slowing down the hikes but tried to downplay that afterwards.

This points to sort of a confusion at the #Fed and that some members may not have made the final decision on the rate hike yet

2/8

#nikileaks tweeted the #Fed is thinking about slowing down the hikes but tried to downplay that afterwards.

This points to sort of a confusion at the #Fed and that some members may not have made the final decision on the rate hike yet

2/8

Also some politicians have written letters to the #Fed calling them to focus more on the jobs creation, i.e. opt for easier hikes.

Of course we have the midterms next week.

Adding to that is the BoC decision last week to hike 50 when every1 expected them to go 75.

3/8

Of course we have the midterms next week.

Adding to that is the BoC decision last week to hike 50 when every1 expected them to go 75.

3/8

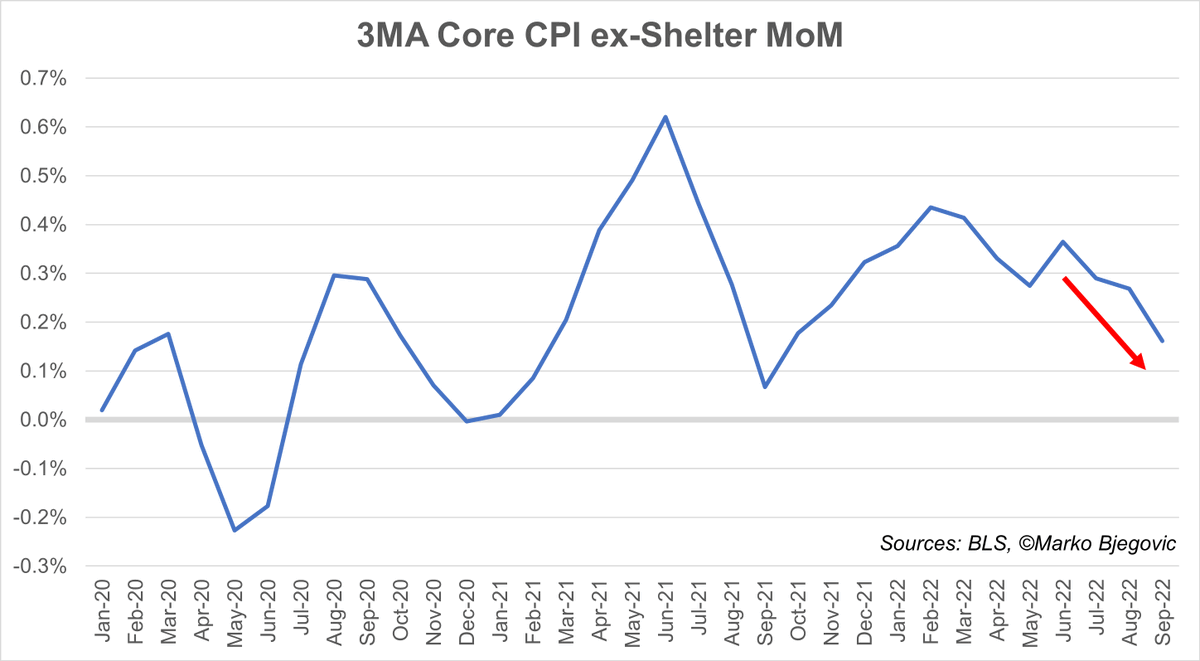

Then there are economic developments like the ISM prices paid that fell into contraction in Oct showing the lowest reading since May 2020 when we still had lockdowns.

ISM manufacturing at 50.2 is just a tad above contraction and it may dip below 50 as soon as this month.

4/8

ISM manufacturing at 50.2 is just a tad above contraction and it may dip below 50 as soon as this month.

4/8

OTOH Sep JOLTS report came in much above expectations. Job openings came in at 10.7M vs 10M exp while Aug was revised up to 10.3M from 10.05M.

This is not great for the #Fed that wants to see lower gap between job openings and ppl that are unemployed.

5/8

This is not great for the #Fed that wants to see lower gap between job openings and ppl that are unemployed.

5/8

Finally we come to sth that many omit but may be significant for Jay Powell and the #Fed.

Remember how they announced their pivot from "transitory" to hiking/QT in Nov last year.

Maybe this Nov may again be the month-of-choice for Jay Powell to make policy changes.

6/8

Remember how they announced their pivot from "transitory" to hiking/QT in Nov last year.

Maybe this Nov may again be the month-of-choice for Jay Powell to make policy changes.

6/8

These threads take a lot of time and effort to write.

If you like the content, please love and retweet to help me spread the message.

7/8

If you like the content, please love and retweet to help me spread the message.

7/8

Of course there is not enough compelling evidence to say for sure the #Fed will blink tdy and opt for 50.

Still there are reasons pointing into that direction:

1) midterms

2) confusion at the #Fed

3) BoC

4) ISM prices paid

5) Nov may be a good month for a policy change

8/8

Still there are reasons pointing into that direction:

1) midterms

2) confusion at the #Fed

3) BoC

4) ISM prices paid

5) Nov may be a good month for a policy change

8/8

• • •

Missing some Tweet in this thread? You can try to

force a refresh