I shall be live tweeting TIA India 20-20 ideas summit and investing ideas discussed today !

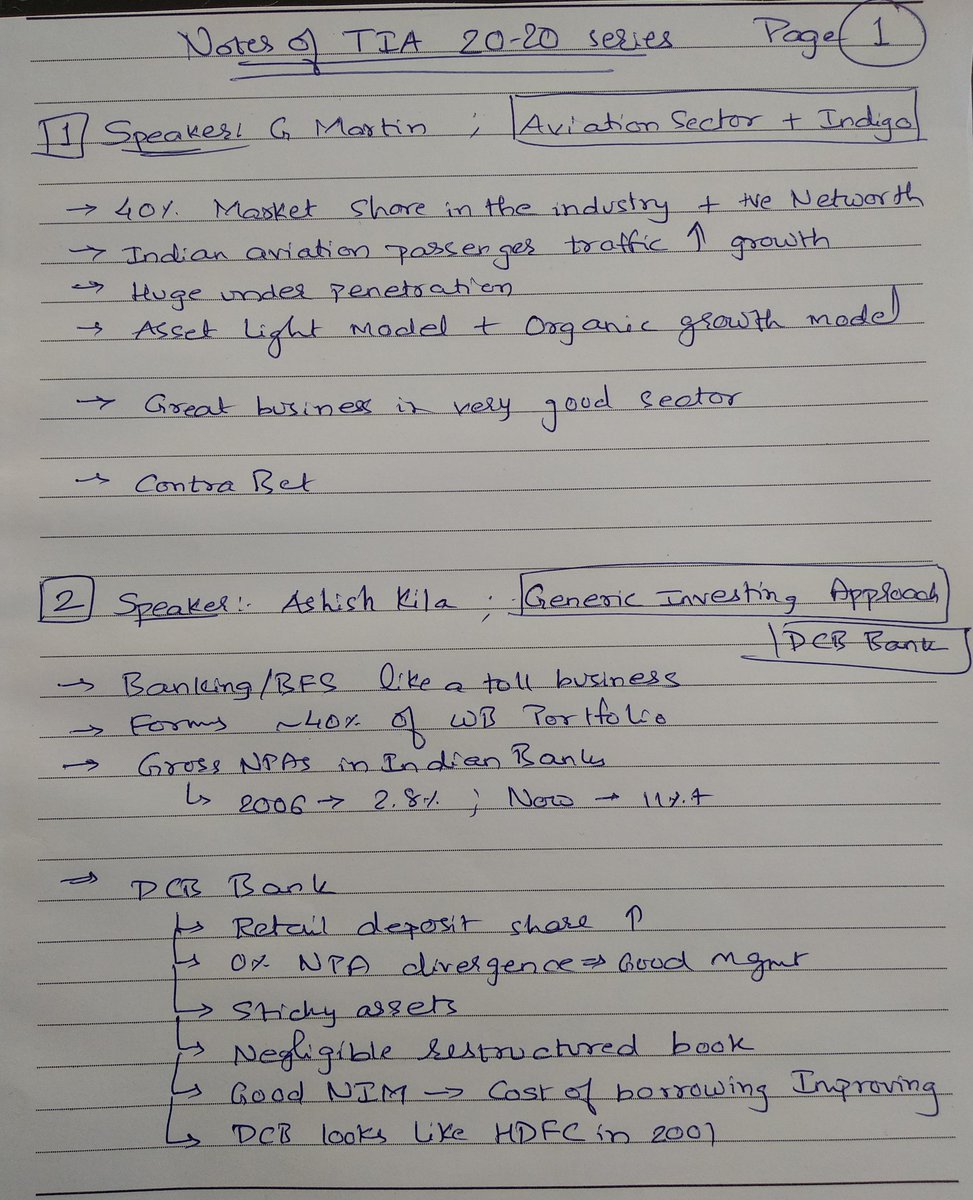

First speaker G Marian talks about Indian Aviation sector.

Indigo with 40+% market share is only player with positive net worth !

Indigo with 40+% market share is only player with positive net worth !

Phenomenal growth in domestic passenger traffic for Indian Aviation last 25 years !

Total capacity of Indian Aviation just few hundred flights vs 25000+ for US !

Asset light model, did not gain mkt share through acquisition !

10000+ cr cash reserve on BS ! Wow !

A great business in great sector can't be bought at good price during Good times !!

Indigo Looks good given very less D/E ratio + low EV/Sales .

Surprised !!

Surprised !!

Good to see him end with APJKalam quote !!

Overall Indigo looks a sound Contrarian investing Idea !!

Next speaker Ashish Kila.

Talks of generic investing approach.

Banking /BFS is more than 40% of Warren Buffets portfolio.

It is like toll business.

It is like toll business.

Gross NPAs in Indian banks : 2.8% in 2006, now 11+% !

Value migration from PSU banks to Pvt banks is happening last many years.

Base effect catching up on HDFC bank. CAGR used to be 170% in 90s !!

DCB Bank is his investing idea.

Retail deposit share increasing over years.

DCB Bank has 150 branches now.

0% NPA divergence for DCB bank , indicating transparent management.

DCB 79% retail deposits, CUB 67% retail. Looks sticky assets. Good.

Share of top borrowers in book not much . Negligible restructured book.

DCB scores well on good NIM. Cost of borrowing improving but best is ICICI bank !

For valuing banks, ROA matters more than Book Value.

Buffett view : Don't buy bad banks at cheap prices but we'll run banks at fair prices.

Conclusion view : DCB on numbers looks akin to HDFC bank in 2001.

Ekansh Mittal next speaker. Is founder of katalystwealth.com

His idea is Manappuram finance.

His idea is Manappuram finance.

PE 8, dividend yield 2.8% !! Interesting

NPA is less than 0.5%

2nd largest Gold loan NBFC. 74% AUM from Gold loans. Trying to diversify.

Gold prices started correcting from.

FY12. That impacted the business.

Add to it RBI regulations.

FY12. That impacted the business.

Add to it RBI regulations.

This all guided management to push for de risking

Very little ALM in gold loan business.

Business will easily survive current liquidity crunch faced by other NBFCs today.

Now growth mainly coming from new segments.

Insider buying into Mana Finance also a good sign.

Ends with disclaimer , he has vested interest in the stock .

Next speaker Sanjay Santhanam speaks about sector idea : AMCs

HDFC AMC and Reliance Nippon

Former has 39 PE, latter is 19.

Significant PAT margin. And great growth last few years.

Former has 39 PE, latter is 19.

Significant PAT margin. And great growth last few years.

Huge AUM Growth from 2000 to 2018 for industry.

Particularly last 6-7 years.

Particularly last 6-7 years.

Main competition for AMCs is safer investing aka Bank FDs.

Now MF AUM is 20% of FD AUM, same as 2008 but vs 12% in 2012

(Interesting )

Now MF AUM is 20% of FD AUM, same as 2008 but vs 12% in 2012

(Interesting )

Key observation : Regardless of model of distribution, AMCs don't need to care, they make money.

Also all are well capitalised so bottom line doesn't need to correlate into forward capex.

Also all are well capitalised so bottom line doesn't need to correlate into forward capex.

ETFs (passive management) is a Challenger to AMCs ?

Could be a long term threat but 10+ years per speaker.

Could be a long term threat but 10+ years per speaker.

Rel Nippon vs HDFC AMC. Two different approaches.

Former has hold on ETFs !

Significant operating leverage is +ve.

-ve is regulatory actions.

Former has hold on ETFs !

Significant operating leverage is +ve.

-ve is regulatory actions.

DCF calculations at pessimistic scenario point to both AMCs trading at discount.

Ends saying can be high dividend play stocks , as they don't need fresh capital to grow .

In short, a Beta play on capital markets in India.

In short, a Beta play on capital markets in India.

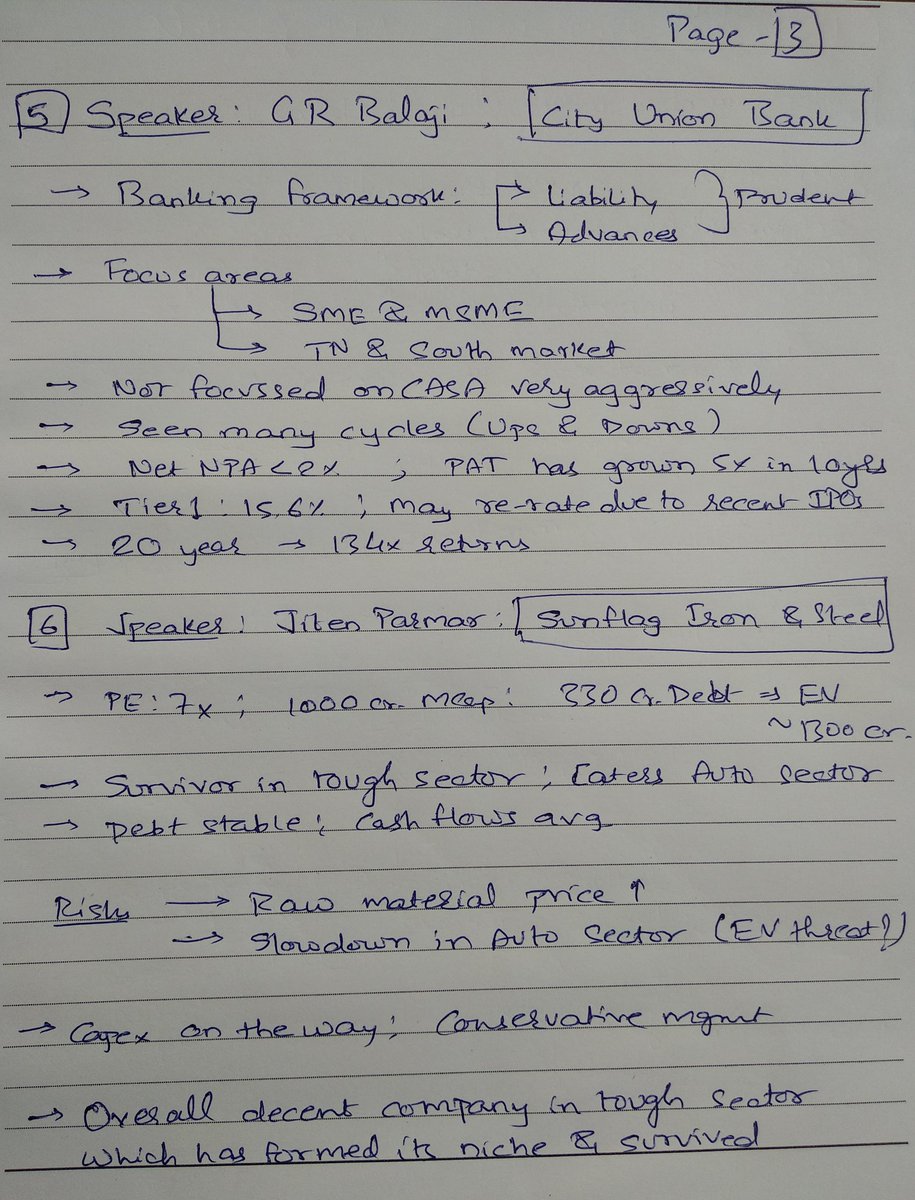

Next presenter is GR Balaji.

His is a banking stock.

Framework for success in banking :

Build granular liability, grow advances prudently.

Framework for success in banking :

Build granular liability, grow advances prudently.

Paying less dividend is prudent in banking.

City Union Bank is the stock idea.

Focus area : SME and MSME , in TN and South India.

Growth charts (10 yr) look very impressive !!

Bank says they are not CASA focussed. That's new !!

100+ yr history means they hv seen many many cycles. Good !

Cost to Income ratio of < 40 % seems one of best in industry.

NPA Net < 2% looks ok

PAT 5x in 10 yrs.

PAT 5x in 10 yrs.

100 yrs , 7 CEOs only . Seems one of best stability.

Focussed on Trading and MSME segments

Focussed on South India esp TN.

100+ yrs of profit and dividend record 👍👍

Focussed on Trading and MSME segments

Focussed on South India esp TN.

100+ yrs of profit and dividend record 👍👍

Tier 1 capital 15.6%. looks healthy.

Recent NBFC issues may help CUB like banks.

Ends by pointing 20 yr return is 134x.

Awesome !!

Awesome !!

Among investing ideas discussed so far in TIA 20-20, Indigo Air and City Union Bank look most Interesting to me (My personal view ).

Indigo Air because it is making money and has positive net worth in a Industry that is notorious for capital destruction.

And CUB because of a rare older era private bank that gave 100+x returns in 20 years. If I recall correct HDFC bank 50x in 18 years.

(My view)

And CUB because of a rare older era private bank that gave 100+x returns in 20 years. If I recall correct HDFC bank 50x in 18 years.

(My view)

Next speaker is veteran investor @jitenkparmar from Aurum Capital.

His stock idea is Sunflag Iron and steel.

His stock idea is Sunflag Iron and steel.

PE of 7 1000 cr MCap 330 cr Debt .

Specialty steel maker.

Survivor among many peers in a tough sector .

Specialty steel maker.

Survivor among many peers in a tough sector .

Mainly caters to Auto Sector. Now expansion outside here

Customer list - mostly Automobile names.

Cash flow looks ok. One bad yr in 10 yrs. Debt stable. Quite surprise in a sector known for debt binging.

Risks - Raw material price hike, and any slowdown in Indian Auto sector. Second one unlikely imo.

Capex coming but quite conservative MGMT (which is why they HV survived so long) !!

EV threat is also mentioned but while away !

Concludes taking questions.

Next Speaker Vijay Anand, CFA

Was hedge fund manager in HK.

His stock idea is Cummins India and has a 4-5 yr view on it .

Was hedge fund manager in HK.

His stock idea is Cummins India and has a 4-5 yr view on it .

Last 4 yr flat show in Revenue, Profits for Cummins India

Capital goods cyclical co. Buying at right time is key

Products are BS6 engines for Trucks, Generators, construction etc.

BS6 is big positive.

Products are BS6 engines for Trucks, Generators, construction etc.

BS6 is big positive.

Exports to parent as well.

After Sales Service also a biz.

No debt.

After Sales Service also a biz.

No debt.

It's growth synchs with IIP growth.

And that synchs with capex cycle. So nice play on capex cycle.

Power deficit gone down meant flat growth.

Now on any growth in power demand will help Cummins.

Now on any growth in power demand will help Cummins.

Forward PE in comfort zone.

Company has good correlation with Construction Capex

BS6 deferment may help competition.

BS6 deferment may help competition.

Concludes with BS6 mention.

Additional mention - Cummins India has huge RnD backing , will be competing well with rising pollution /AGW concerns

Additional mention - Parent may hike stake in future

Next presenter is Jatin Khemani.

he owns stalwartvalue.com

His stock idea : 25% CAGR last 10 yrs.

Is into maize processing. Makes starch and it's derivatives.

Which are inputs into processed foods, toothpaste etc.

Also input to medical syrups (liquid glucose)

Supplier to Top FMCG and Pharma companies

Raw material input is maize, abundantly produced in India .

Multi location plants.

Multi location plants.

Competition : Anil Ltd, Riddhi Siddhi, Cargill India all loss making or bankrupt

New product , HFCS, sweetener substitute to sugar . Huge scope

Legacy business is edible oil extraction.

Turnaround in this biz due to duty revamp by guvt .

Good scuttlebutt feedback .

2700 cr MCap, 12 PE. Bet on high earning growth.

Logistics prevents any China threat. Bulky product .

Risk : Keyman risk .

Logistics prevents any China threat. Bulky product .

Risk : Keyman risk .

Stock name : Gujarat Ambuja Exports !!

Next presenter : Balaji Vaidyanathan

CEO of crest wealth.

Was with Sundaram Fin group.

Was with Sundaram Fin group.

His idea : Sanghvi Movers

480 cr MCao, EV 1000+ cr.

Crane rental company , 6th largest in world

Cater to 100+ Metric Tonne segment.

Wind mainly . Then metro, infra, etc

480 cr MCao, EV 1000+ cr.

Crane rental company , 6th largest in world

Cater to 100+ Metric Tonne segment.

Wind mainly . Then metro, infra, etc

10 yrs return. Very cyclical.

Company fortunes fluctuates with policy change on depreciation and wind energy .

Major impact due to wind tariff policy change .

Spot power prices increase in recent times, Renewable power target for 2022 all positive for wind and thus for Sanghvi

Spot power prices increase in recent times, Renewable power target for 2022 all positive for wind and thus for Sanghvi

Sanghvi story seems correlated to wind power story. But company trying to diversify.

Gross monthly yield on asset 1.95% last qtr vs 3% in fy16.

Best case yield gives 133% upside in EV.

Worst case yield gives 33% downside from current EV.

Best case yield gives 133% upside in EV.

Worst case yield gives 33% downside from current EV.

Case made to invest in Sanghvi than a Suzlon as they can use cranes elsewhere if wind sector falters !

Ends presentation, mentioning other 10 yr financial Details.

Next speaker is VS Venkatesan.

Starts with nice disclaimer (Tamil saying)

Is a banker turned broker , distributor. Seen in Tamil Media, regular TIA speaker .

Starts with nice disclaimer (Tamil saying)

Is a banker turned broker , distributor. Seen in Tamil Media, regular TIA speaker .

Characters of multibaggers : Low equity capital, high promoter holding, high sales to net profit % , high reserve and surplus, zero debt, pricing power, inelastic demand

Company name is : CRISIL.

Qualifies on all these parameters.

Shares technical view as well.

Shares technical view as well.

Concludes sharing tech view !!

Next speaker is @AnandMohan1977

Investor and mentor at @equitybulls

His investing idea is a apparel retail chain

Debt free, expanding now. Focus on tier 2 and 3.

V2 Retail is the stock.

Businesses learning from past mistakes.

Investor and mentor at @equitybulls

His investing idea is a apparel retail chain

Debt free, expanding now. Focus on tier 2 and 3.

V2 Retail is the stock.

Businesses learning from past mistakes.

Originally called Vishal Retail.

Past history detailed.

Past history detailed.

Till 2011 was multi product company. Emulating Wal-Mart.

Then course corrected, sold units .

Now focus only on fashion retail in tier 2 and 3 cities.

Slower expansion to avoid excess borrowing.

6 store to 49 last 7 yrs

Then course corrected, sold units .

Now focus only on fashion retail in tier 2 and 3 cities.

Slower expansion to avoid excess borrowing.

6 store to 49 last 7 yrs

Improved in inventory mgmt, WC mgmt etc. Gross margins have improved.

MCap doubled to 1000 last 1.5 yrs.

Focus on private labels, now 12% want to double in few years.

Store presence mostly in small towns . Less competition + less Real estate costs

49 to 70 stores in last many months .

Store presence mostly in small towns . Less competition + less Real estate costs

49 to 70 stores in last many months .

Org retail share last 10 yrs up from 4 to 10%

Huge opportunity for it to grow further esp in small towns.

Huge opportunity for it to grow further esp in small towns.

What can go wrong - among others, thread from online retail mentioned.

Concludes sharing PL details etc.

Now breaking for Lunch. Other speakers post lunch .

TIL , Indigo Air is already among top 20 (or 25) airlines in World. This is from a country where half population hasn't owned a personal vehicle and 3/4 th would have not have even seen an airport (except in movies etc). Hmm.

Resuming the 20-20 session.

Next speaker is Shagun Jain.

Corporate banker with 14+ yrs experience.

Next speaker is Shagun Jain.

Corporate banker with 14+ yrs experience.

His stock idea is Vinati Organics.

CAGR sales 16%

PAT 21%

Over last 10 yrs

CAGR sales 16%

PAT 21%

Over last 10 yrs

20x returns in 10 yrs.

In hottest sector, specialty chemicals.

In hottest sector, specialty chemicals.

So being hottest sector and one good company in this sector , very impressive nos. ROE 30+%though declining.

Then CFO up 30x in 10 yrs.

No debt . Wish invested this in 2009

But not even heard of it .

Then CFO up 30x in 10 yrs.

No debt . Wish invested this in 2009

But not even heard of it .

Passes all standard quality checks.

RPT, Receivable, Group co operations, share pledge, Cash flow from operation etc.

RPT, Receivable, Group co operations, share pledge, Cash flow from operation etc.

Analogy with who earns more : doctor , specialist or super specialist.

Likewise Commodity chem vs super specialty chemicals . Latter most profitable.

Likewise Commodity chem vs super specialty chemicals . Latter most profitable.

What they produce : Speciality monomers, aromatics. ATBS, IBB.

Most of them, mkt share of Vinati is very high !

IBB used in painkillers !!

Lot of fresh capacity on these coming up from Vinati.

+ import substitution angle .

Import substitution => Reduce hedging cost => hi margins!

Most of them, mkt share of Vinati is very high !

IBB used in painkillers !!

Lot of fresh capacity on these coming up from Vinati.

+ import substitution angle .

Import substitution => Reduce hedging cost => hi margins!

Unique differentiators : Green manufacturing, focus in high margin products .

Risks : Crude oil derivatives but cost is pass thru

Concentrated customer profile. Global biggies like Dow Chemicals etc. Time to market is high.

Risks : Crude oil derivatives but cost is pass thru

Concentrated customer profile. Global biggies like Dow Chemicals etc. Time to market is high.

Ends presentation mentioning huge cash flows they make !

Next speaker is Dhruvesh Sanghvi of Prospero tree.

His idea is JM Financials.

His idea is JM Financials.

JM Financials mainly into Investment Banking, Wealth Management biz.

Last 6 yr Sales 2+x, profit 6+x.

Into developer finance mkt. Quite a place today !!

Last 6 yr Sales 2+x, profit 6+x.

Into developer finance mkt. Quite a place today !!

Credit mkt of India today :

PSU banks 57%, Pvt Banks 25% NBFC 18%

PSU banks 57%, Pvt Banks 25% NBFC 18%

Current crisis can lead to lower competition in future , good for prudent players in long run.

14000 cr loan book today .

14000 cr loan book today .

ARC biz is also not factored into valuation. 12000 cr AUM in ARC

PAT 4-5x in 5 yrs.

Well capitalised NBFC with multiple biz lines. 6000 cr MCap.

Concluding remarks : Well funded, high liquidity NBFC with worst case priced in (shows a table to justify same).

Well capitalised NBFC with multiple biz lines. 6000 cr MCap.

Concluding remarks : Well funded, high liquidity NBFC with worst case priced in (shows a table to justify same).

New capacities announced in distillery side by sugar Industries.

Due to recent guvt measures wrt Sugar and ethanol blending .

Ethanol blending from 0.3% to 4% last 7 years (impressive ) !

Due to recent guvt measures wrt Sugar and ethanol blending .

Ethanol blending from 0.3% to 4% last 7 years (impressive ) !

Ethanol now profitable .

Now talks about sugar Industry .

High cyclicality so far.

Sugar is cyclical but Distillery and Power is stable wrt EBIT.

Now talks about sugar Industry .

High cyclicality so far.

Sugar is cyclical but Distillery and Power is stable wrt EBIT.

New capacity addition happening next 3 yrs after gap of 5-6 years !

Balrampur forecast ethanol output will be 2x in next 3 yrs.

Balrampur forecast ethanol output will be 2x in next 3 yrs.

Dhampur more ethanol less sugar.

BCL Industries also mentioned.

BCL Industries also mentioned.

Speaker says to play safe on Ethanol blending theme, stick to leader which is Balrampur Chini.

Dhampur has debt .

BCL has real estate biz in addition.

Global peers trade at 10-20 PE.

Dhampur has debt .

BCL has real estate biz in addition.

Global peers trade at 10-20 PE.

Risks : Guvt changing policy, execution risks.

Ends by quoting Warren buffet "No body wants to get rich slow !!"

Ends by quoting Warren buffet "No body wants to get rich slow !!"

Next speaker is Ravi Padmanabhan.

Speaker and trainer in personal finance .

His investing idea is Tata Elixi.

Speaker and trainer in personal finance .

His investing idea is Tata Elixi.

Tata Elixi into design and Tech services for products.

Into IOT etc.

Gives description of what IOT is.

Into IOT etc.

Gives description of what IOT is.

Industry served:

60% Auto, 30% into Media and broadcast.

More into design side of business.

60% Auto, 30% into Media and broadcast.

More into design side of business.

Tata Elixi in auto , focussing on Connected cars, health innovation etc.

Working on SW for cutting edge tech. E.g Autonomous driving.

Product could be a middlrware for OEMs.

Working on SW for cutting edge tech. E.g Autonomous driving.

Product could be a middlrware for OEMs.

Disruption in Auto industry is defined as : Someone born today, may never learn to drive a car .

Now financials are shown.

Debt free company. Consistent dividend. Good ROE

But last few years growth is tepid.

Europe 50% , US 30 % revenues.

Stock has correct last few months (35%)

Debt free company. Consistent dividend. Good ROE

But last few years growth is tepid.

Europe 50% , US 30 % revenues.

Stock has correct last few months (35%)

Triggers : Parents, IP

PE 21, debt free, good to add at CMP.

Speaker concludes with this note.

PE 21, debt free, good to add at CMP.

Speaker concludes with this note.

Next speaker is : Mrs Nalinakanthi.

Columnist in BL, Consultant , writes in Monday edition of Portfolio.

She presented in last year 20-20 session Sun pharma that was when stock bottomed out !

Pharma she focussed on

This year, her pick is Divi Laboratories.

Columnist in BL, Consultant , writes in Monday edition of Portfolio.

She presented in last year 20-20 session Sun pharma that was when stock bottomed out !

Pharma she focussed on

This year, her pick is Divi Laboratories.

She mentions pharma stocks have turned around last few months

After few years of bad run !

A sector that cannot be ignored .

After few years of bad run !

A sector that cannot be ignored .

Divis IPO in 2003. 25% CAGR in price.

In CRAMS space.

Focus on differentiated products .

Margins if patented product can be as high as 80%

Generics 57% rest Custom synthesised.

Investment case : RnD capablity. Debt free, cash rich, 500 cr FCF this year , 30% dividend payout !

In CRAMS space.

Focus on differentiated products .

Margins if patented product can be as high as 80%

Generics 57% rest Custom synthesised.

Investment case : RnD capablity. Debt free, cash rich, 500 cr FCF this year , 30% dividend payout !

Kakinada Greenfield expansion growth driver .

4x growth in revenues and profits last 5 yrs (approx)

Good promoter holding of 52%, highest after Sun Pharma. "Skin in the Game".

Financials : OPM peaked in 2014. Then dipped. Things now improved. Next 2 yrs ratios must be better.

4x growth in revenues and profits last 5 yrs (approx)

Good promoter holding of 52%, highest after Sun Pharma. "Skin in the Game".

Financials : OPM peaked in 2014. Then dipped. Things now improved. Next 2 yrs ratios must be better.

Stock now at 39 PE. Forward PE 20+. (FY20) . Justifiable due to growth potential.

Only concern can be adverse regulatory development. Management has managed to come out of regulatory issues in past. E.g 2015-17 .

Concludes mentioning currency fluctuation may also be a concern.

Only concern can be adverse regulatory development. Management has managed to come out of regulatory issues in past. E.g 2015-17 .

Concludes mentioning currency fluctuation may also be a concern.

Next speaker is @varadhar1

He starts by identifying (rightly) that idea of these stock idea sessions is not so much about the stock picks but more about the thought process behind it.

Underlying process must be understood is his view !

He starts by identifying (rightly) that idea of these stock idea sessions is not so much about the stock picks but more about the thought process behind it.

Underlying process must be understood is his view !

He is a passionate part time investor, focussed on forensic investing .

His stock idea is Majesco .

IT Service co now turned into a IT product company

Into insurance space .

Illustration of example of how insurance cos using tracking technology to offer differentiated services.

His stock idea is Majesco .

IT Service co now turned into a IT product company

Into insurance space .

Illustration of example of how insurance cos using tracking technology to offer differentiated services.

Preference model : Business where capex is done and operating leverage kicks in.

Where rising sales leads to accelerated cash flows .

Majesco has a cloud based subscription service

Last 3 yr PL - Op leverage kicking seen.

Where rising sales leads to accelerated cash flows .

Majesco has a cloud based subscription service

Last 3 yr PL - Op leverage kicking seen.

Other merits. Ample liquidity. No debt. QIP completed. Evidence of Good Corp governance.

Margins will grow with sales

Marquee customers : Allianz, MetLife etc.

Valuation 60-70% of peers. Can catch up with peers

Margins will grow with sales

Marquee customers : Allianz, MetLife etc.

Valuation 60-70% of peers. Can catch up with peers

Low analyst coverage, undiscovered space. So can catch analyst fancy and rerate.

Mentioned about S and J curve in biz.

J Curve - When capex done EPS takes off on sales takeoff.

Mentioned about S and J curve in biz.

J Curve - When capex done EPS takes off on sales takeoff.

Legacy biz 60% and Cloud 40%.

Latter growing impressively.

Scuttle butt favorable esp on PnC side of biz.

Risk : Keyman risk, Trump /H1B.

Concludes saying : Low analyst coverage is the big opportunity to rerate !!

Latter growing impressively.

Scuttle butt favorable esp on PnC side of biz.

Risk : Keyman risk, Trump /H1B.

Concludes saying : Low analyst coverage is the big opportunity to rerate !!

Next speaker is R Vetrivel.

Starts with disclaimer.

25 year investor in markets. Into full time investing in last few years.

Starts with disclaimer.

25 year investor in markets. Into full time investing in last few years.

Took early retirement , now full time investor.

Views on LT winner stocks :

Franchisee, demand supply demography , beneficiary of GDP growth. Or aligns as part of India or Global LT trend.

Example of such trend : Scooter to Motorcycle , Gums to Feviquick stick adhesive.

Views on LT winner stocks :

Franchisee, demand supply demography , beneficiary of GDP growth. Or aligns as part of India or Global LT trend.

Example of such trend : Scooter to Motorcycle , Gums to Feviquick stick adhesive.

Other enablers : Long product cycle, low sales cycle (Buffett principle).

+ Leverage to improve margins.

His Stock idea is : Zee Learn.

Main biz segment : Kisses,learning kits , school infra biz, flexible staffing etc.

+ Leverage to improve margins.

His Stock idea is : Zee Learn.

Main biz segment : Kisses,learning kits , school infra biz, flexible staffing etc.

KidZee : Asia's largest pre School chain !

Present in 700+ cities.

Franchisee model .

Present in 700+ cities.

Franchisee model .

Financial oplev : last few years Sales CAGR 25% , profit CAGR 70%

Structural tailwind.

Only 11% Indians preschooled.

Structural tailwind.

Only 11% Indians preschooled.

Income elasticity on education is 1.5

Only 11% market share in pre school market in India

Annual spend on Pvt sector school in India is 3.5 L crore Rs.

Only 11% market share in pre school market in India

Annual spend on Pvt sector school in India is 3.5 L crore Rs.

Speaker Expecting 3x in 5 yrs, 10x 10 yrs in Zee learn.

Switching costs leads to a moat.

Risks - Guvt fixing fees, high pledge of shares by Zee Group.

Concludes saying it is a must have B2C stock.

Switching costs leads to a moat.

Risks - Guvt fixing fees, high pledge of shares by Zee Group.

Concludes saying it is a must have B2C stock.

Next speaker is : Saurabh Kumar.

Part time investor. Value investor type.

Stock idea is Apollo Hospitals.

Revenues 5x but profits 3.4 x and now down.

Debt up, cash flow up but margins fallen big .

Part time investor. Value investor type.

Stock idea is Apollo Hospitals.

Revenues 5x but profits 3.4 x and now down.

Debt up, cash flow up but margins fallen big .

Apollo Hospital also has India's biggest Pharmacy chain

10000 bed chain. Many business within.

CAGR over long period good, last 3 yrs not good.

Regulation, politics , recent policy changes are negatives.

All these have impacted profits but not revenues .

Rising interest rates .

10000 bed chain. Many business within.

CAGR over long period good, last 3 yrs not good.

Regulation, politics , recent policy changes are negatives.

All these have impacted profits but not revenues .

Rising interest rates .

Stock is best when worst is seen and froth is gone .

Share of revenue : 2015 to 2018

Pharmacy gaining.. EBIDTA of pharmacy 3x in recent years.

If this trend continues: it may be called as a Pharmacy biz that also owns Hospitals !!

Share of revenue : 2015 to 2018

Pharmacy gaining.. EBIDTA of pharmacy 3x in recent years.

If this trend continues: it may be called as a Pharmacy biz that also owns Hospitals !!

Margins of store and Hospitals improve with age

Current pharmacy ROE 15% but older stores have 20+% ROE.

Likewise Hospitals over 5 yrs EBIDTA is better

Half beds are less than 5 yrs !

10% beds still not used falling

Recent expansion has depressed returns!

Current pharmacy ROE 15% but older stores have 20+% ROE.

Likewise Hospitals over 5 yrs EBIDTA is better

Half beds are less than 5 yrs !

10% beds still not used falling

Recent expansion has depressed returns!

Mgmt done with capex, will focus on ROE and profits and less debt next few years.

1600 stores in 2014 vs 3000+ today !

India has 6Lakh pharmacies today.

1600 stores in 2014 vs 3000+ today !

India has 6Lakh pharmacies today.

Historical valuation 16-30 PE except in 2008.

Fair value per speaker is 1300 around. Mispricing valuation story .

Concludes mentioning risks as debt and regulations and disruption due to predictive machine learning Heath care etc.

Fair value per speaker is 1300 around. Mispricing valuation story .

Concludes mentioning risks as debt and regulations and disruption due to predictive machine learning Heath care etc.

Next speaker is Subash R.

His stock idea is Colgate Palmolive.

Terms it as very boring business

Investing process must be simple.

His stock idea is Colgate Palmolive.

Terms it as very boring business

Investing process must be simple.

Argument in favor : Steady compounder. Non discretionary daily use. Strong brand. Not a rapid CAGR type but asset light, debt free market leader. Demand steady.

Close to 50% mkt share in toothpaste + brushes .

2-3x sales, profit last 9 years.

Calls this business "Rahul Dravid"

Says entry decision can be made based on PE.

Use dips to accumulate the stock.

Concludes recommending having 20% of PF on basket of FMCG stocks. (HUL, Britannia)

2-3x sales, profit last 9 years.

Calls this business "Rahul Dravid"

Says entry decision can be made based on PE.

Use dips to accumulate the stock.

Concludes recommending having 20% of PF on basket of FMCG stocks. (HUL, Britannia)

Now the last (but most anticipated) speaker of the day : @shyamsek .

Topic of his presentation : Wealth Network

Introduces a company of 8000 cr MCap and 3% dividend yield.

Name's not shared yet !

Topic of his presentation : Wealth Network

Introduces a company of 8000 cr MCap and 3% dividend yield.

Name's not shared yet !

Speaks of Broad trend of more money going into Financial Assets.

Now at 40% for India, should cross 50% in next 10 yrs. Share of equity in savings will continue to increase.

Likewise digital infrastructure will also expand . Convergence is the theme.

Now at 40% for India, should cross 50% in next 10 yrs. Share of equity in savings will continue to increase.

Likewise digital infrastructure will also expand . Convergence is the theme.

Financialisation is the theme

And stock to ride is : ICICI securities .

Best tech platform.

+ Client base doubling every 5 years

1 cr client in 5 yr possible.

IPO overpriced but selloff over done.

And stock to ride is : ICICI securities .

Best tech platform.

+ Client base doubling every 5 years

1 cr client in 5 yr possible.

IPO overpriced but selloff over done.

Brokerage biz very profitable but a risk.

Financial product distribution is also a big LOB.

Private wealth mgmt, estate planning also good.

Next 5-10 yrs broking will become less dominant LOB.

Concludes that ICICI sec

High quality ROE biz at good price .

Financial product distribution is also a big LOB.

Private wealth mgmt, estate planning also good.

Next 5-10 yrs broking will become less dominant LOB.

Concludes that ICICI sec

High quality ROE biz at good price .

Additional info by ShyamS : PE 14 for high ROE biz. EV 7300 crore. Worth looking.

This brings end of @TIA_Investors 20-20 investing ideas session for 2018. Shall add my views on some of these stock ideas in coming days .

Special thanks to @TIA_Investors for organizing this great session. Highly informative and highly useful for all investors. Kudos 🙏🙏🙏🙏

Special thanks to @TIA_Investors for organizing this great session. Highly informative and highly useful for all investors. Kudos 🙏🙏🙏🙏

Addendum : In post session speech @shyamsek opines that next 5 years manufacturing may surprise on positive side. Quite a contrary view. He recalls how in 2009 he ignored commodities in favor of Consumer franchises. That was also good insight. 👍👍

Some notes from yesterday's TIA 20-20 session shared in this tweet by Invest Books.

Pls take time to read even if u don't agree.

Note - My own views will post soon maybe separate thread.

Pls take time to read even if u don't agree.

Note - My own views will post soon maybe separate thread.