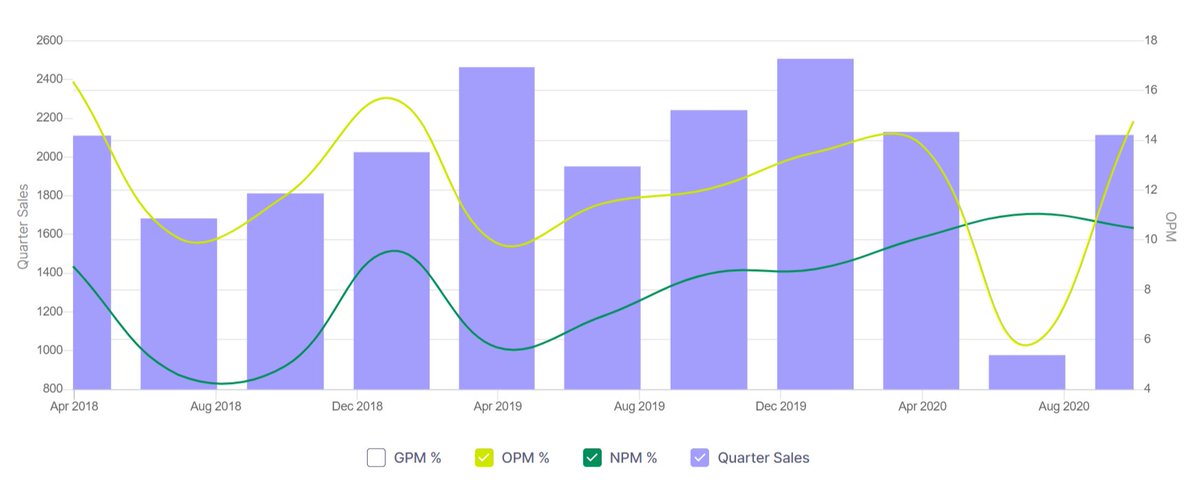

Profit trends suggest that it has been in a 10Y stagnation

Any breakout from here will start a multi-year rally.

Any breakout from here will start a multi-year rally.

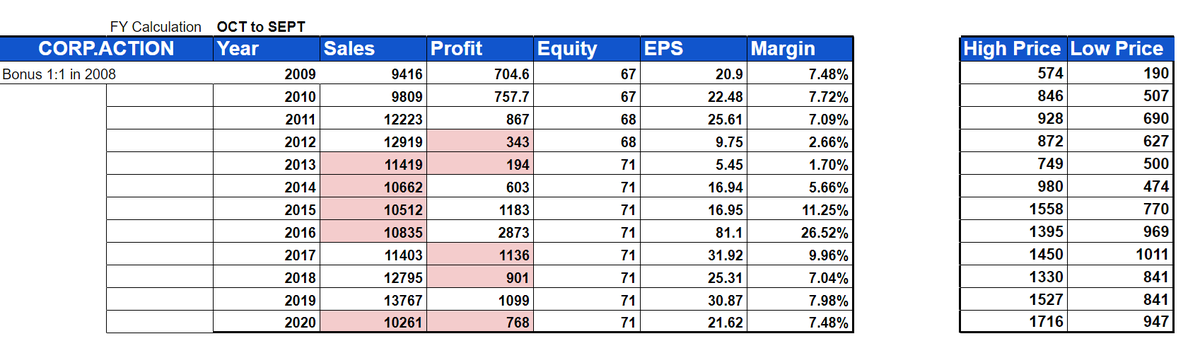

Raw materials constitute 70% of its operating costs.

Any breakout/breakdown depends more on raw material price cycle rather than sales/demand growth.

If copper becomes cheaper, Siemens will capitalize on it. Conversely, if Copper becomes costly, the consolidation will continue.

Any breakout/breakdown depends more on raw material price cycle rather than sales/demand growth.

If copper becomes cheaper, Siemens will capitalize on it. Conversely, if Copper becomes costly, the consolidation will continue.

Not giving any price targets for 2030 as the organic profit growth of this company is only 3.5% CAGR. Its fortunes depend on raw material prices so take a calculated view based on how you think commodity prices will behave.

Personal opinion : Best avoided.

Personal opinion : Best avoided.

• • •

Missing some Tweet in this thread? You can try to

force a refresh