𝟭/𝟲 𝗥𝘂𝘀𝘀𝗶𝗮 𝘁𝗼 𝗰𝘂𝘁 𝗴𝗮𝘀 𝘀𝘂𝗽𝗽𝗹𝘆 𝘁𝗼 𝗣𝗼𝗹𝗮𝗻𝗱 𝗮𝗻𝗱 𝗕𝘂𝗹𝗴𝗮𝗿𝗶𝗮 𝗼𝗻 𝗔𝗽𝗿𝗶𝗹 𝟮𝟳𝘁𝗵 𝟮𝟬𝟮𝟮.

𝗗𝗼𝗲𝘀 𝗻𝗼𝘁 𝗽𝗼𝘀𝗲 𝗮 𝘀𝘆𝘀𝘁𝗲𝗺𝗶𝗰 𝗴𝗮𝘀 𝘀𝘂𝗽𝗽𝗹𝘆 𝗿𝗶𝘀𝗸 𝘁𝗼 𝗣𝗼𝗹𝗮𝗻𝗱 & 𝗕𝘂𝗹𝗴𝗮𝗿𝗶𝗮.

#gas

@JavierBlas

𝗗𝗼𝗲𝘀 𝗻𝗼𝘁 𝗽𝗼𝘀𝗲 𝗮 𝘀𝘆𝘀𝘁𝗲𝗺𝗶𝗰 𝗴𝗮𝘀 𝘀𝘂𝗽𝗽𝗹𝘆 𝗿𝗶𝘀𝗸 𝘁𝗼 𝗣𝗼𝗹𝗮𝗻𝗱 & 𝗕𝘂𝗹𝗴𝗮𝗿𝗶𝗮.

#gas

@JavierBlas

2/6 Poland (40%) and Bulgaria (77%) have traditionally been dependent on Russian Gas (numbers are from 2020 and are estimated somewhat higher for 2021).

3/6 Both countries have planned well ahead. Poland is opening a gas link with Lithuania in May and the Baltic Pipe connecting to Norway is planed to be operational in October.

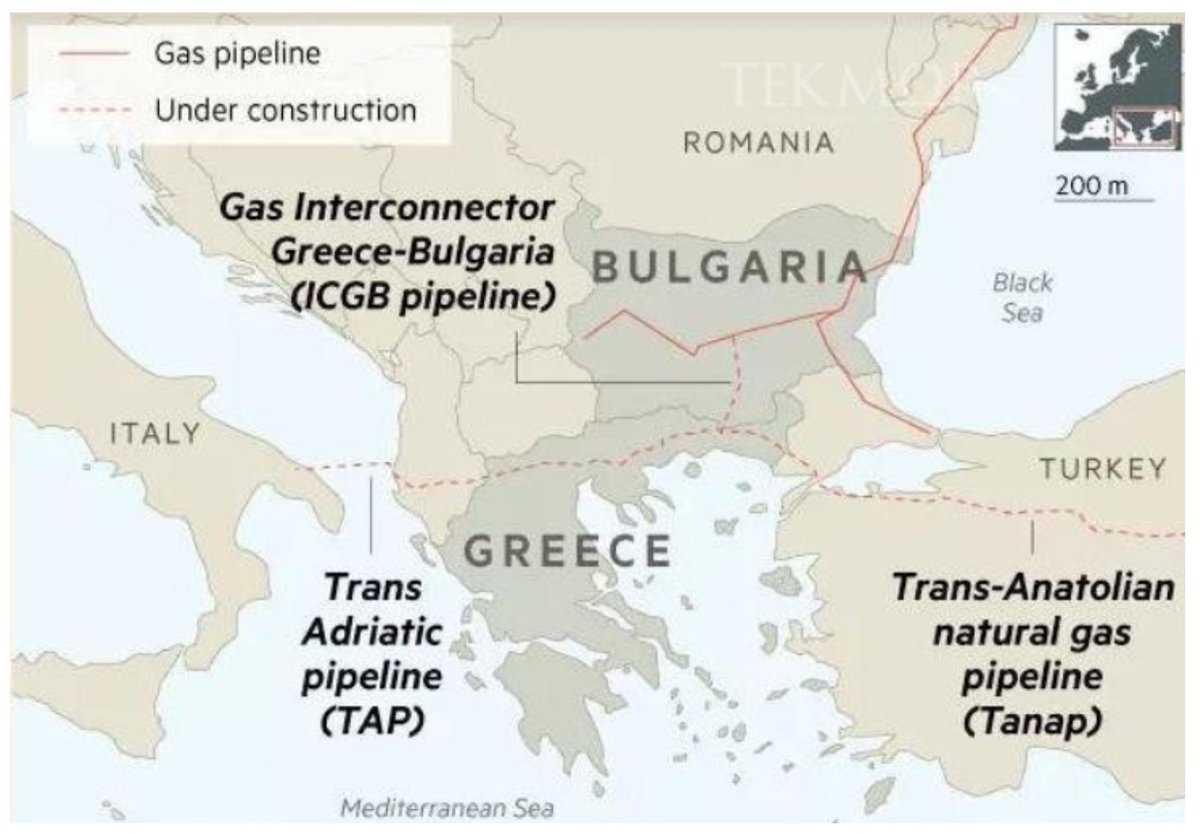

4/6 Bulgaria is connecting to Greece via the Greece-Bulgaria Gas Interconnector. Commercial operation is planed to start in September. The Tanap pipeline connecting Azerbaijian via Turkey to Greece is operational since 2018.

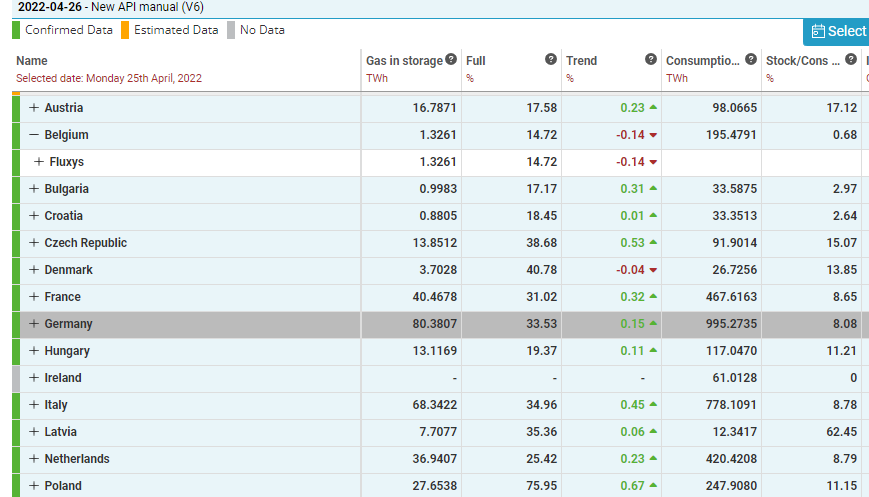

5/6 Furthermore Poland has planed well ahead with its gas storage as of April 26th at over 75%. Bulgaria gas storage level at just over 17%. However total Bulgarian gas imports are only 3bcm and new Gas Interconnector pipeline has capacity of 3 to 5 bcm.

6/6 This is not to say that there will be no price & economic impacts. Decrease of Russian gas supply does tighten overall supply and could put upward pressure on price. However systemic risk/no gas available to Poland & Bulgaria are vastly overstated.

• • •

Missing some Tweet in this thread? You can try to

force a refresh