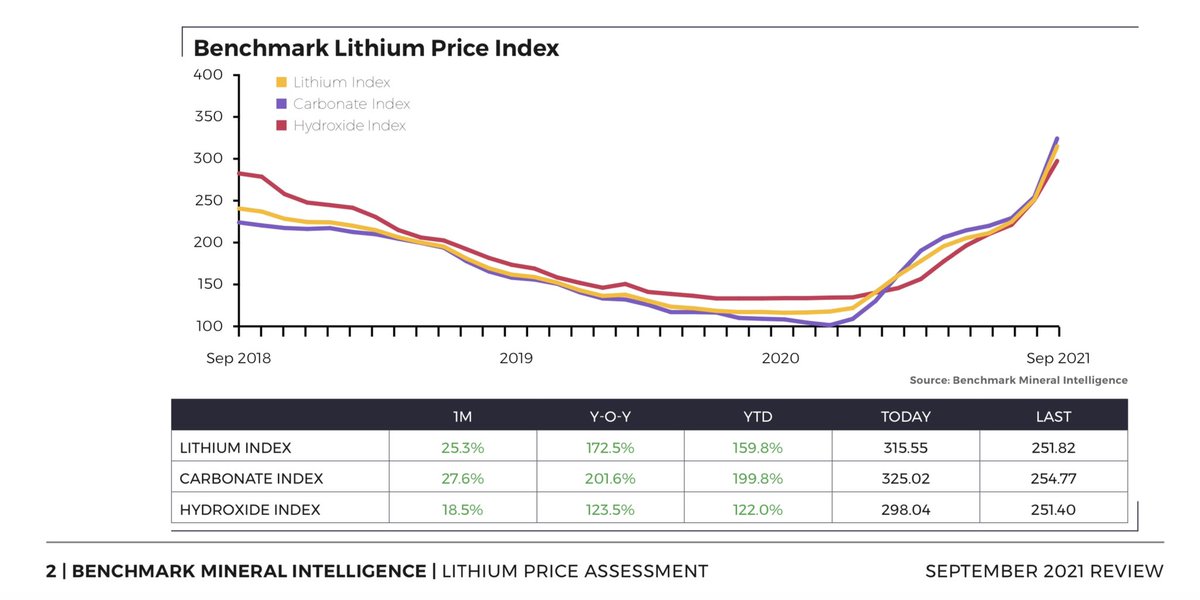

We’ve seen this before, we will see it again. Goldman Sachs: you can’t just add up all the #lithium mine level potential & make an oversupply call

The speciality chemicals world is more nuanced than iron ore

It’s why the world doesn’t rely investment banks for research any more

The speciality chemicals world is more nuanced than iron ore

It’s why the world doesn’t rely investment banks for research any more

To make forecast calls especially for Nickel and Lithium at the moment should be regulated.

Much like our IOSCO price assessments.

There should be a min amount of expert work required to make such high profile calls that impact investors, esp the retail community.

Much like our IOSCO price assessments.

There should be a min amount of expert work required to make such high profile calls that impact investors, esp the retail community.

Slapdash forecasts do a disservice to the all the work the professional publishing world conduct - including our competitors

We have spent so much time, money and effort building our Forecasts division that everything published has to go thru many hurdles & be a professional, considered opinion.

Banks (high profile) should be required to do a similar amount of work before publishing.

Banks (high profile) should be required to do a similar amount of work before publishing.

In response to a lot of requests: @benchmarkmin will be putting out its response to the Goldman Sachs call very soon. #lithium #nickel #cobalt

• • •

Missing some Tweet in this thread? You can try to

force a refresh