After last night's initial pass, reading through the Tax Cuts and Jobs Act legislative text in deeper detail today. Full write-up coming to Nerd's Eye View blog on Monday morning.

In the meantime, will be sharing some (threaded) highlights here...

In the meantime, will be sharing some (threaded) highlights here...

Original Tax Reform proposal from President Trump would have narrowed from 7 tax brackets down to 3. The House GOP proposal would have kept 4 brackets (plus a 5th phase-out bracket of 45.6% for upper income folks).

Final TCJA keeps the 7 tax bracket structure, but trims rates.

Final TCJA keeps the 7 tax bracket structure, but trims rates.

Top tax bracket for individuals comes down to 37% under TCJA (from 39.6%), but the removal of the Pease limitation (which was effectively a 1.2% income surtax on the top bracket) means the top rate cut is really from ~40.8% down to 37%.

Original 7 tax brackets from Senate proposal would have repealed the marriage penalty, but final TCJA brings it back for top bracket. 37% rate starts at $500k for individuals, $600k for couples.

But impact is limited. $1M couple each earning $500k pays "just" $8k more in taxes.

But impact is limited. $1M couple each earning $500k pays "just" $8k more in taxes.

While new lower tax brackets under TCJA are "temporary" & will sunset after 2025, shift to chained-CPI for indexing tax bracket thresholds is permanent.

This is the primary reason most individuals pay more by 2027. New brackets gone, but lower C-CPI-U bracket thresholds remain.

This is the primary reason most individuals pay more by 2027. New brackets gone, but lower C-CPI-U bracket thresholds remain.

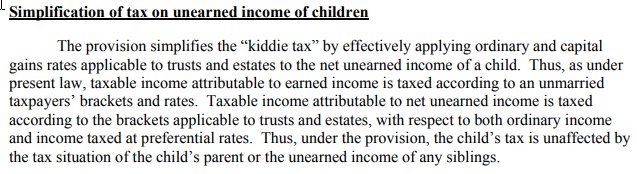

Major change that hasn't been discussed: TCJA revamps the Kiddie Tax rules, in what will be a big increase for most.

Under new rules, unearned income of children is taxed at Trust tax rates (top bracket at $12,500), NOT just stacked on parents' income brackets. #Ouch

Under new rules, unearned income of children is taxed at Trust tax rates (top bracket at $12,500), NOT just stacked on parents' income brackets. #Ouch

To reduce the #GOPTaxPlan cost, the "old" bracket thresholds will continue to apply to long-term capital gains & qualified dividends, which means those rates won't align to ordinary income brackets anymore.

Instead, top 20% cap gains will start in the middle of the 35% bracket.

Instead, top 20% cap gains will start in the middle of the 35% bracket.

The consolidation of Personal Exemptions into a new Standard Deduction under #GOPTaxPlan results in (slightly) higher deductions for individuals & couples, but LESS for families w/ at least 1 child.

However, in practice, the expanded Child Tax Credit makes up for this for most.

However, in practice, the expanded Child Tax Credit makes up for this for most.

While the expansion of the standard deduction already would have limited how many itemize deductions, the curtailment of SALT & mortgage deductions & repeal of miscellaneous itemized will REALLY drive MOST taxpayers to claim the standard deduction in the future.

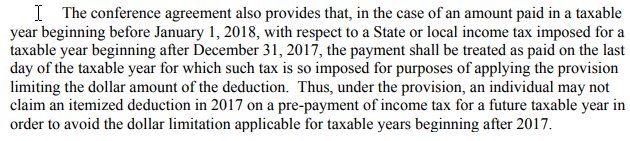

New $10,000 cap on state/local income & property taxes in 2018 has many tempted to prepay in 2017. But #GOPTaxPlan explicitly prohibits prepayment of 2018 income taxes in 2017.

Can still deduct 2017 4th quarter estimated in 2017, though. And prepaid property taxes (if possible).

Can still deduct 2017 4th quarter estimated in 2017, though. And prepaid property taxes (if possible).

The #GOPTaxPlan grandfathers existing mortgages over the new $750k limit (using the old $1M debt limit) for the mortgage interest deduction.

However, interest on home equity indebtedness is NOT grandfathered. Starting 2018, it's just not deductible anymore, period.

However, interest on home equity indebtedness is NOT grandfathered. Starting 2018, it's just not deductible anymore, period.

After all the #GOPTaxPlan debate about whether to repeal or retain the medical expense deduction, the final legislation not only keeps it, but actually EXPANDS the deduction temporarily, reducing the 10%-of-AGI threshold to just 7.5%-of-AGI for 2017 & 2018 (for regular & AMT).

Hrm. #GOPTaxPlan stipulates that in the future, casualty losses will ONLY be deductible if they are part of a Federally-declared disaster area. Mere 'personal' disaster losses will no longer be deductible, even if exceeding 10% of AGI.

Was this really an area of abuse??

Was this really an area of abuse??

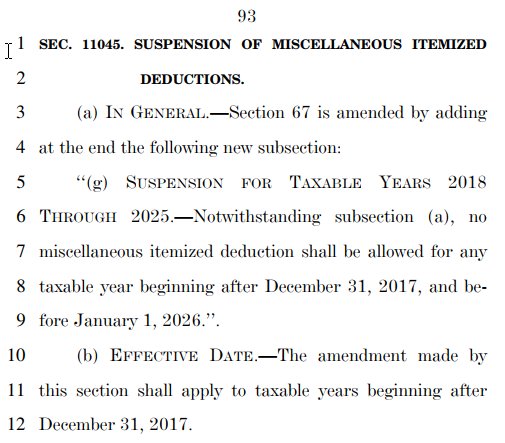

Final advisors will be upset that the final #GOPTaxPlan fully repeals IRC Section 67 - miscellaneous itemized deductions subject to the 2%-of-AGI floor. Which includes both tax prep fees, unreimbursed employee business expenses, annuity losses... and investment advisory fees!

Ironically, #GOPTaxPlan repeal of investment advisory fee deduction means consumers paying advisors via commissions (subtracted pre-tax from investment and annuity products) get better tax treatment than paying fees. Even as advisors trend towards fiduciary fees over commissions.

Ok, taking a break for a few hours. Will be back to more writing (and live-tweeting) later today! :)

Ok, back for another round of deep-diving into the #GOPTaxPlan legislative text!

Original #HouseGOPTaxPlan would have consolidated educational tax credits into (slightly-expanded) American Opportunity Tax Credit, along w/ eliminating deductibility of student loan interest. Senate version would have taxed grad student tuition assistance. None of these passed.

#HouseGOPTaxPlan would have consolidated Coverdell Accounts into 529 plans. Final rules dropped this.

HOWEVER, 529 plans can now be used for elementary/secondary school (like Coverdells).

And 529 plans can now be used for homeschooling expenses!

$10k/student annual limit.

HOWEVER, 529 plans can now be used for elementary/secondary school (like Coverdells).

And 529 plans can now be used for homeschooling expenses!

$10k/student annual limit.

Probably not directly intended, but #GOPTaxPlan rules allowing homeschooling expenses for 529 distributions redefined "qualified higher education expenses" entirely. Which means Coverdell Education Savings Accounts should be able to make tax-free homeschooling distributions too.

Very sad when parents save in a 529 college savings plan for a child, and the child ends out disabled and unable to go to school. A new provision of #GOPTaxPlan will permit rollovers from 529 to 529A ABLE accounts. Still constrained to 529A contribution limits though.

Nice to see this #GOPTaxPlan provision - disabled beneficiaries who work can contribute their earned income TO their 529A plan (up to $12,060 Federal poverty line). Get the Saver's Credit too. But only permitted if they do NOT contribute to an employer retirement plan as well.

While AMT is not repealed under the #GOPTaxPlan, its impact is substantially diminished. The AMT exemption amounts were increased by $15k-$23k, the exemption phaseouts were boosted dramatically (to $500k indiv/$1M couples), and common AMT adjustments are curtailed (e.g., SALT).

One nice plus of the expanded AMT exemption under the #GOPTaxPlan is that households that have been carrying forward an unusable Minimum Tax Credit will likely get to unwind and use most/all of their AMT credits in 2018!

Lots of buzz on the parts of #GOPTaxPlan that were included. But notable what stayed on the cutting room floor (i.e., still permitted under law):

- $250 schoolteacher deduction

- Tax credit for plug-in electric vehicles

- Adoption Assistance tax credit

- $250 schoolteacher deduction

- Tax credit for plug-in electric vehicles

- Adoption Assistance tax credit

Both House & Senate #GOPTaxPlan limited Section 121 rules allowing up to $500k of primary residence capital gains to be excluded by requiring residence to be owned/used in 5-of-8 years (instead of 2-of-5). House had an income phaseout clause too. NOT included in the final bill.

Boon for life settlements market tucked into #GOPTaxPlan - cost of insurance charges do NOT reduce basis for the seller of an existing life insurance policy, reduced gains. However, life settlements are now all "reportable policy sales" so IRS can track transfer-for-value gains.

#GOPTaxPlan crackdown on Roth recharacterizations is a real bummer for the multiple-accounts Roth conversion strategy (see kitces.com/blog/using-sys…). But not surprising this provision was killed, since original purpose was moot once conversion income limits were repealed in 2010.

Fortunately the #GOPTaxPlan crackdown on Roth recharacterizations only limits recharacterizations of a CONVERSION, but not of a CONTRIBUTION. So "mistaken" Roth contributions can still be fixed (switched to a traditional IRA) w/ the recharacterization rules.

Finishing up our full write-up of #GOPTaxPlan. Will go live on Nerd's Eye View at kitces.com on Monday morning.

In the meantime, a few more provisions of note from my read-through of the full legislative text...

In the meantime, a few more provisions of note from my read-through of the full legislative text...

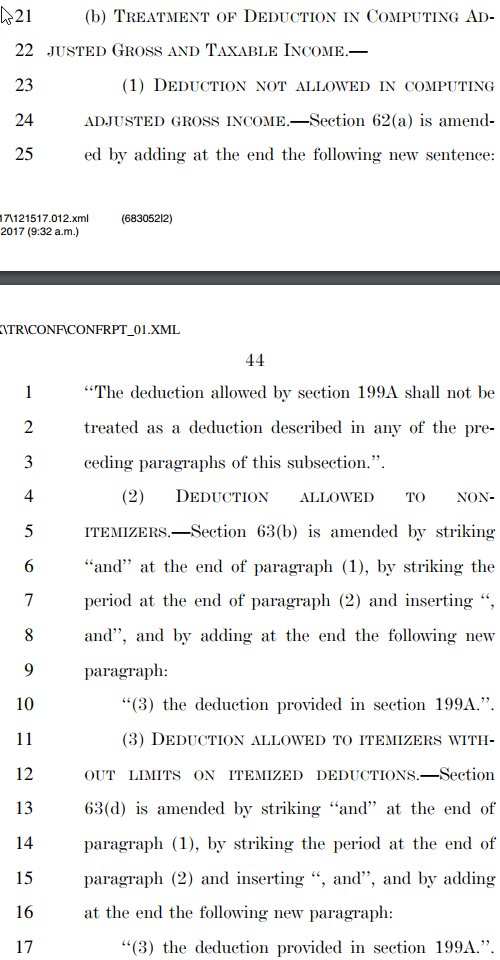

Interesting note on #GOPTaxPlan pass-thru rules: although the deduction is associated w/ a pass-through business, rules are based on the owner's individual tax return. And the QBI deduction will be claimed there, NOT on the business return.

QBI deduction for pass-through businesses in #GOPTaxPlan will essentially create a new category of deduction: below-the-line non-itemized deduction. Final legislation is explicit: it's NOT above-the-line (doesn't impact AGI), but NOT itemized either (can claim on top of std ded).

Another notable aspect of the limitations on pass-through deduction under #GOPTaxPlan - the income limit is calculated individually for each partner/owner. Thus, high-income partners might lose the deduction, even as lower-income minority partners keep it.

As it pertains to financial advisors in our own businesses, the #GOPTaxPlan pass-through deduction is messy. Most larger advisory firms can't benefit. "Smaller" advisors can, if they're below the income thresholds for specified service business ($157,500 indiv, $315k couples).

Broker-dealer (and large RIA) fears about the #GOPTaxPlan pass-through may be justified, though. "Lower-income" employees (under $157,500 indiv, $315k couples) will get QBI deduction as sole proprietors, but not as employees. Pressure to go totally independent will rise.

Overall, the pass-thru deduction under #GOPTaxPlan is substantially disruptive to financial advisory firms. Lower-income employees at RIAs and B/Ds will want to become independent contractors. Large RIAs will want to become C corps (or Check The Box to be taxed that way).

#GOPTaxPlan has a minor tweak for divorces - alimony will no longer be deductible to payors and taxable to recipients in the future (which allowed tax savings since payor tends to be higher income/brackets). Only for divorces after 2018, though. Existing alimony grandfathered.

Surprising crackdown under the #GOPTaxPlan - tax preferences for moving expenses. Starting 2018, your moving expenses won't be deductible anymore. And employer reimbursements for moving expenses will become taxable income (not excluded anymore, as they are now).

After years of crackdowns on the deductibility of cars used in a business, #GOPTaxPlan increases the deduction limits significantly. Will be more appealing to buy a car within the business next year. May even cause some to decide to buy instead of lease for business purposes?

Another #GOPTaxPlan crackdown: business entertainment expenses. While 50% of food & beverage expenses will remain deductible, TCJA eliminates the deduction for "any activity generally considered to be entertainment, amusement, or recreation". So much for "business" sports events.

Interesting. #GOPTaxPlan provides employers a 12.5% (and up to 25%) tax credit if they will actually pay their employees at least 50% (and up to 100%) of wages while they're out on FMLA. Wonder how many employers will take the gov't up on this FMLA tax credit?

Charitable planning under #GOPTaxPlan - most households will have trouble clearing the new higher standard deduction, eliminating tax benefits for charitable giving. New strategy: charitable lumping. Contribute to donor-advised fund all at once to deduct, then dole out over time.

Ok, wrapping up on #GOPTaxPlan review (and live-tweet) for now!

Full article with all the details coming first thing tomorrow (Monday) morning at kitces.com. Stay tuned! :)

Full article with all the details coming first thing tomorrow (Monday) morning at kitces.com. Stay tuned! :)