On Saturday I had a chance to reflect on the consequences of the Tax Cuts and Jobs Act and the path forward at the ASSA meetings. A slightly updated version of my presentation is here. A short version in this thread. piie.com/commentary/spe…

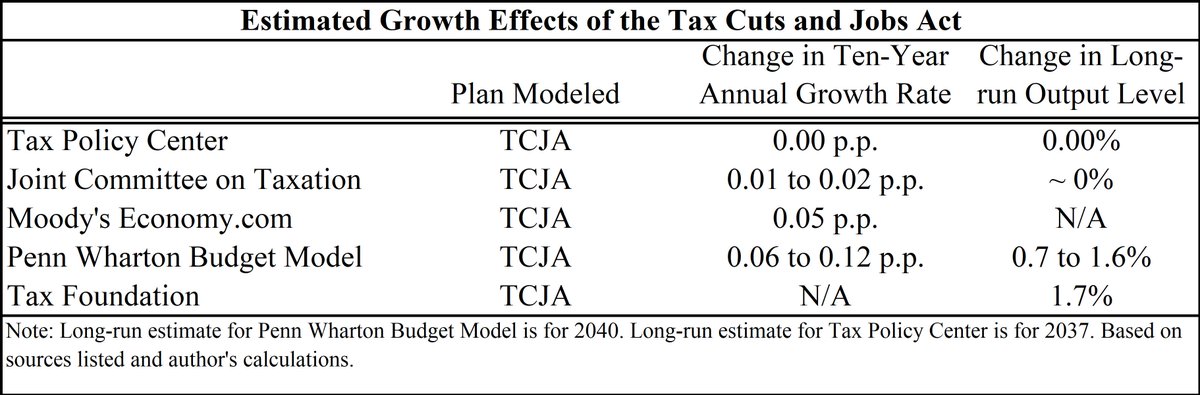

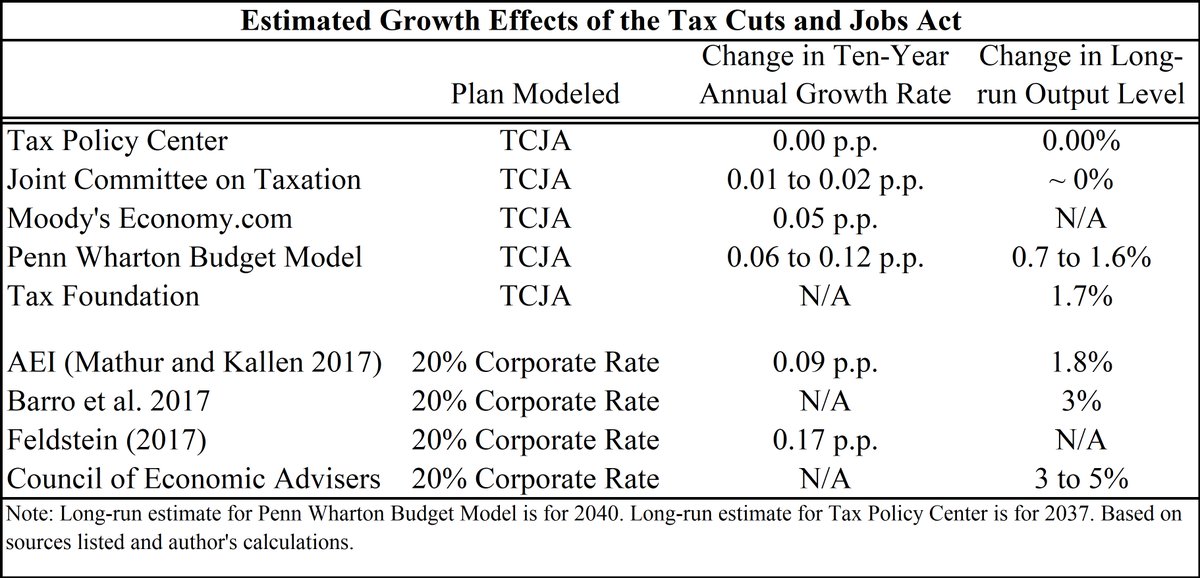

The bulk of the non-political estimates of the Tax Cuts and Jobs Act put the annual growth increase over the next decade at 0.0 to 0.1 pp. That is consistent with the FOMC, SPF, Blue Chip, others not updating long-run potential growth.

Estimates focusing just on the corporate rate reduction (with or without expensing) have tended to find larger estimates—although even these estimates are generally consistent with only a 0.1 to 0.2 pp increase in the annual growth rate over the next decade.

Normally when economists debate they are using different models or elasticities. In most of these cases, however, the models/elasticities are the same. The differences are: (1) crowd out; (2) correctly modeling the size of the corporate sector; and (3) modeling the full plan.

CROWD OUT. Most debate about this but not most important factor. And is more than just borrowing driving up interest rates & reducing investment. Includes diversion of capital from residential/non-corporate & increased foreign borrowing lowering GNP/NI relative to GDP.

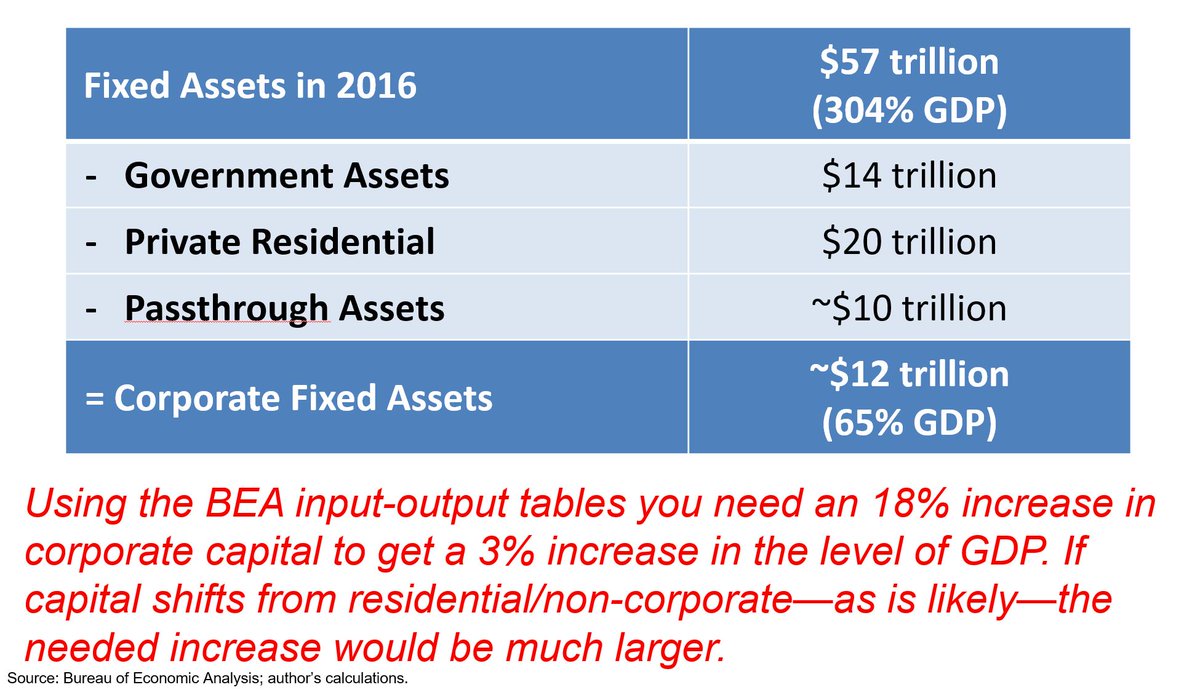

CORRECTLY MODELING THE CORPORATE SECTOR. Economists all know K/Y ≈ 3 but forget corporate capital is only about two-thirds of GDP. Need an 18% increase to get 3% more GDP—and much more needed if capital comes from residential/non-corporate sectors as is likely/desirable.

MODELING THE FULL PLAN. The biggest issue is that the larger estimates generally just cover the rate reduction part of the plan & ignore the rest. Is like saying that a tax reform that cut rates in half but required people to pay on twice their taxable income would boost growth.

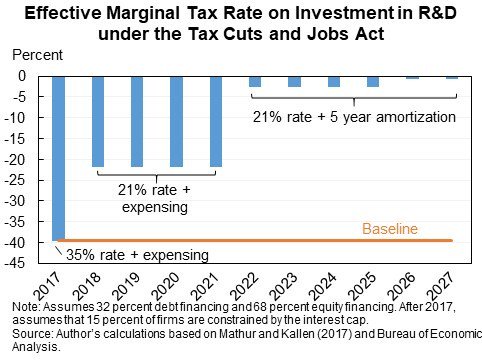

Repealing the manuf deduction, capping interest dedn, ending expensing of R&D and limiting NOLs may be good or bad (and I would put the first two in the good category and last two in the bad), but all have economic consequences that must be incorporated in any macro analysis.

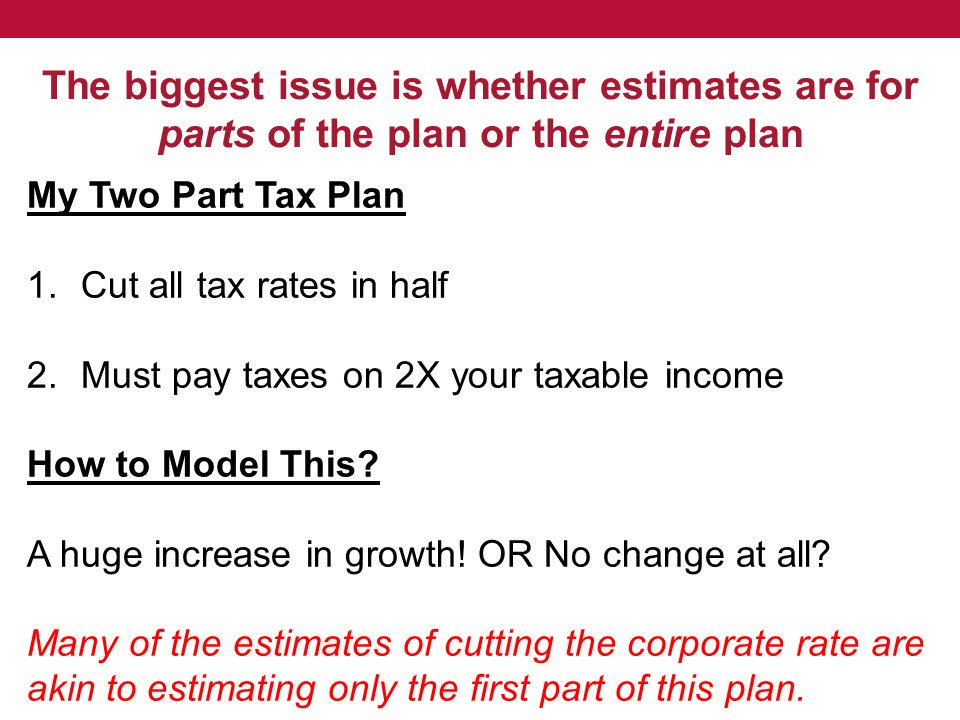

Taking all of these into account, the overall marginal tax rate on corporate investment falls at first but then rises—well above current rates and somewhat above the baseline.

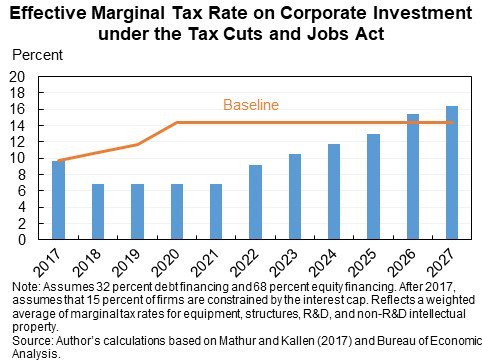

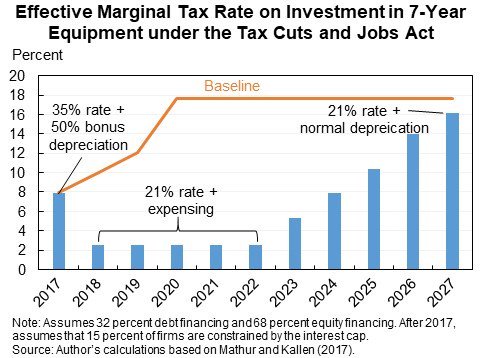

The EMTR falls then rises for equipment, falls for structures, and rises and rises more for R&D.

I should say, I am indebted to AEI researchers and ospc.org for the models underlying many of these calculations. Their spreadsheet is available at aei.org/wp-content/upl…, I will be making my analysis available as well.

Modeling just the redn of the corporate rate to 21% predicts a 1.64% boost in long-run GDP, or a 0.08 pp increase in the annual growth rate over 10 yrs. This is similar to the conclusion of AEI researchers @aparnamath & Cody Kallen for a 20% rate. aei.org/wp-content/upl…

But adding in the other provisions & a modest amount of crowd out (interest rates up 15 bp) reduces the growth effects to a 0.3 percent increase in the long-run level of output, which would be imperceptible in annual growth rates.

Note that all of this growth comes from lower AVERAGE rates, the effect of MARGINAL rates on long-run growth is negative. Important because this growth could disappear or reverse if other countries cut their rates in response.

Some qualifications on all of this analysis, the most important being that future legislation will matter a lot.

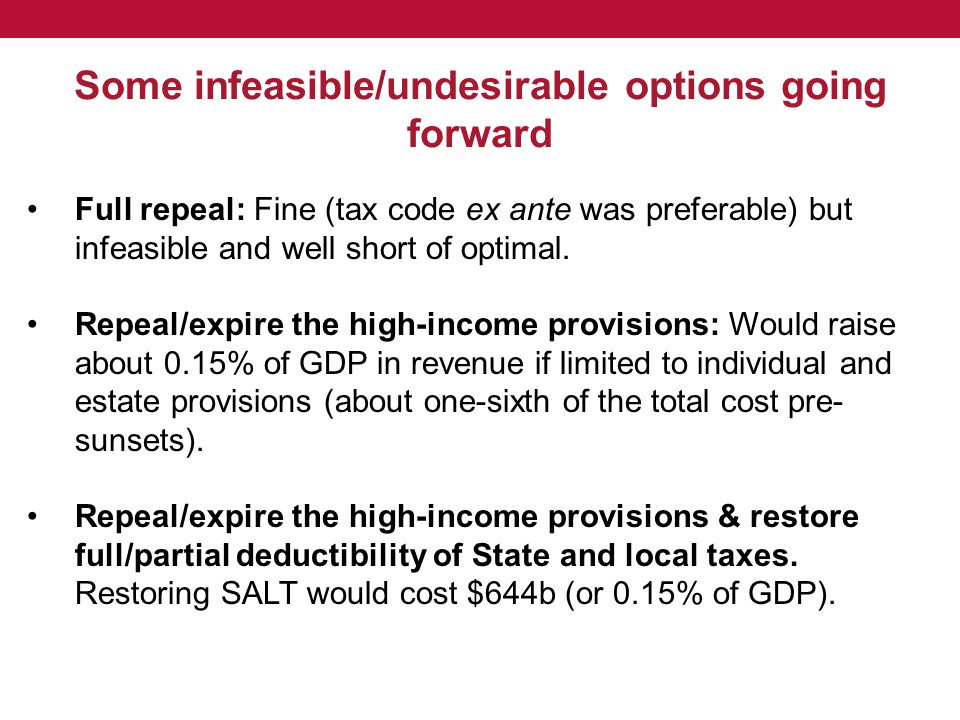

Here are some infeasible or undesirable options for tax changes going forward.

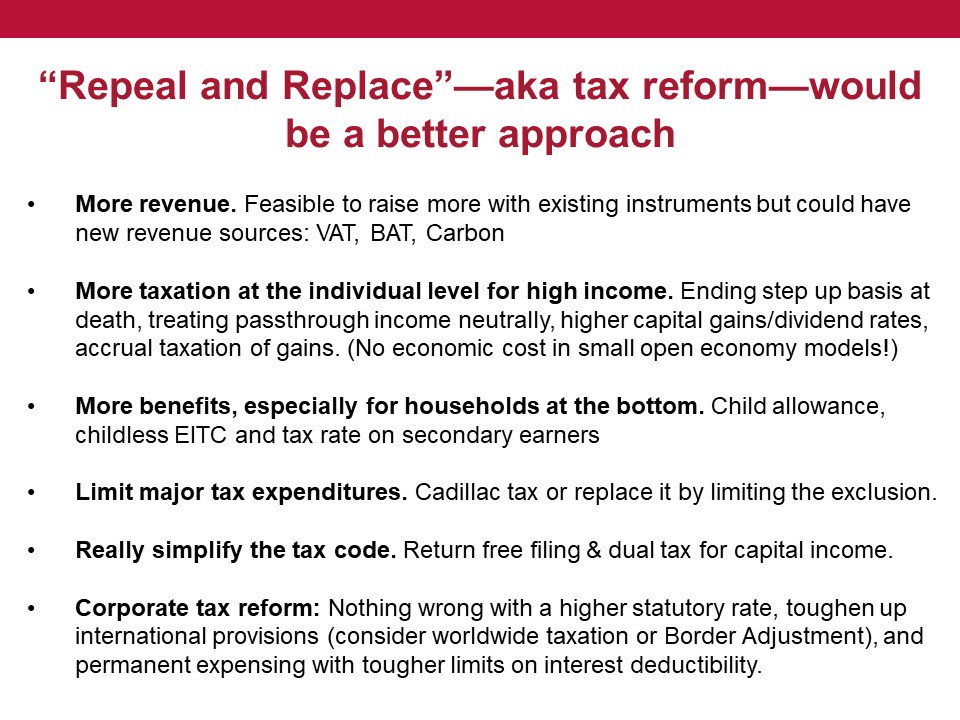

“Repeal and Replace”—aka tax reform—would be a better approach going forward. END THREAD.