,

37 tweets,

11 min read

Read on Twitter

1/ Sometimes I find myself giving the bull case for venture capital as an asset class.

I thought y'all might find the pitch interesting so I'm going to share it

Note If you're pitching your market/asset class you've already lost. I just refuse to surrender so 🤷♂️

I thought y'all might find the pitch interesting so I'm going to share it

Note If you're pitching your market/asset class you've already lost. I just refuse to surrender so 🤷♂️

2/ *Disclaimer: I’m not offering investment advice here and everyone should make their own investment decisions. This is just an overview of the bull case for VC.*

Here we go!

Here we go!

3/ Always the #1 question and one that is really hard to answer. How should I slice the market? How general should I be? There is so much variance in venture.

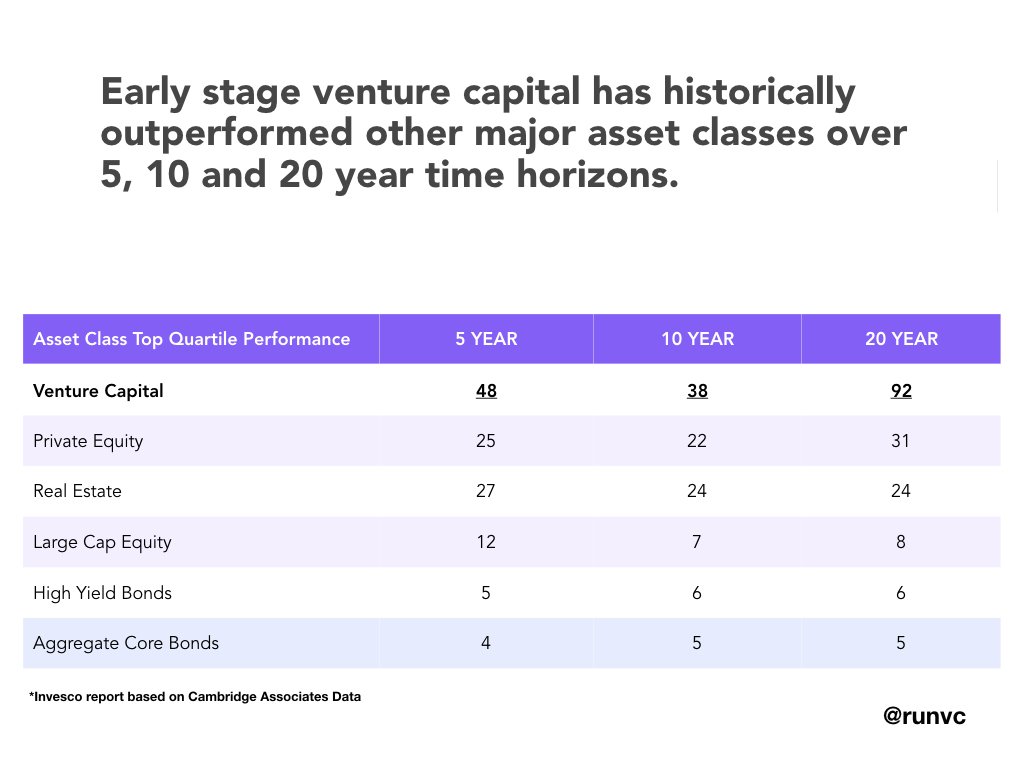

4/ Lets start with some aggregate stats. Important to caveat here that these are top quartile numbers and VC is a top quartile (or top decile) business. You should only play if you have a real, sustainable, valuable edge. MEDIAN RETURNS DON’T CUT IT

5/ You’ve probably heard that VC is a power law business before & that returns are generated by a tiny fraction of opportunities. Its hard to grasp how true that really is but this @HorsleyBridge and @a16z slide really drives it home. In VC, if you aren’t winning, you are losing

6/ Just as a point of comparison (not part of the VC asset class pitch). Bottom quartile fund returns are around 5%- 7%.

5%-7% isn’t terrible for something that is safe, reliable & fairly liquid but for an asset class that locks your capital up for ~10 years, its garbage.

7/ This is the next most common question. There is something of a myth that VC is super risky. It depends on how you define risk. The variance is high, and each underlying investment is highly risky but It’s hard to lose all your money in a fund. Let’s dig in

8/ Here I highlight some older fund vintages that are nearing completion and as you can see, only the bottom quartile in the worst performing vintage is actually losing money.

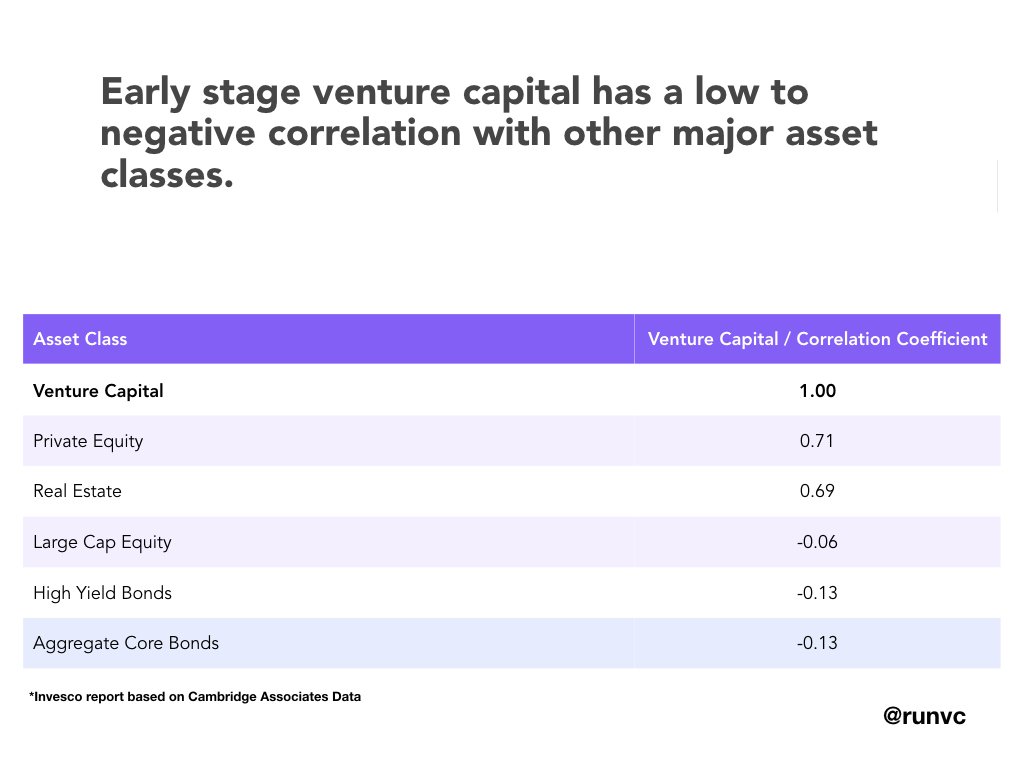

9/ Moreover, we should be looking at risk from an even broader perspective, an investor’s portfolio risk and for that, we need to know the correlation between all of the assets in an investor’s portfolio, this slide comes from @invescous and is based on Cambridge Associate data.

10/ You can actually de-risk your overall portfolio AND increase your expected returns by adding a riskier asset class (like VC) to your portfolio, if the correlation is low or negative. In a simplified example if you owned Blockbuster (public) and Netflix (VC) you made out O.K.

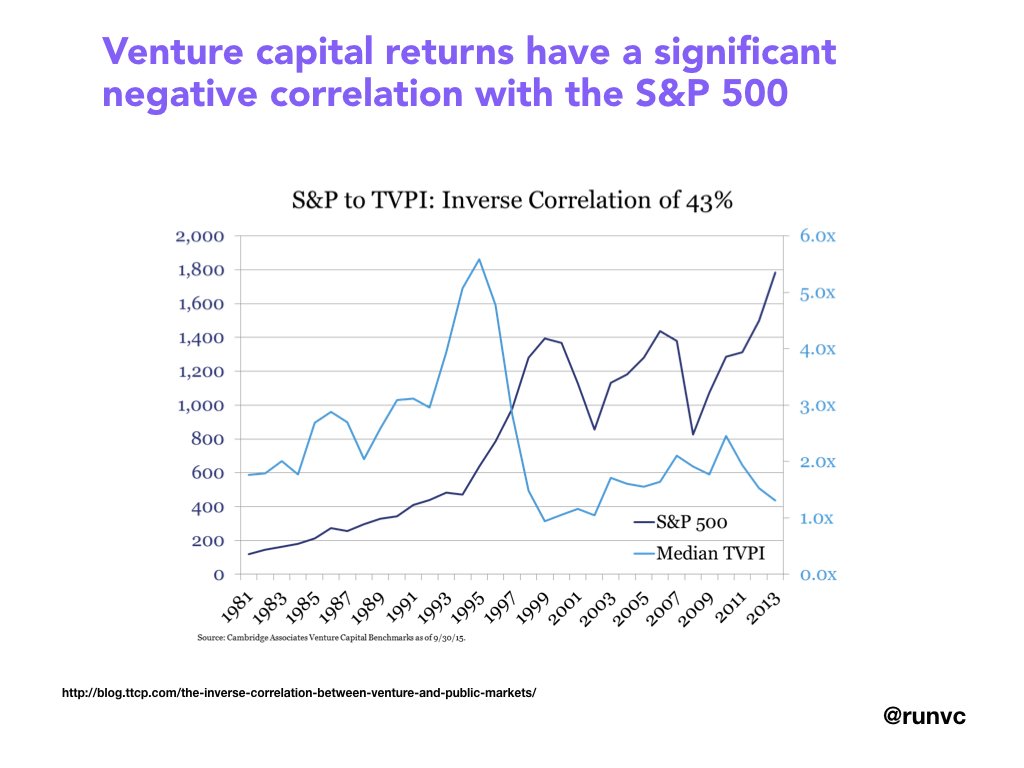

11/ Its also important to think about timing correlation or diversity in your portfolio, which is where the illiquidity of venture actually shines. Venture portfolios are partially shielded against short term market movements AND companies can sometimes time exits.

12/ Not to beat a dead horse (and there are multiple factors at work here) but it’s instructive to note that UBER, AirBnB, Slack, WhatsApp, WeWork, Twilio, Instagram and many of the other breakout venture successes of the last 15 years were founded in the dark depths of 2008-2010

13/ Once I walk through the above, I use this slide, from the brilliant folks @ttcp_sf to drive home the point that VC can help shield your portfolio from Beta (of course it only does that in a cash availability sense if you reliably invest over time and across vintage years)

14/ Another interesting feature of VC is that an investor in a venture fund will likely have their capital “called” over a 4-6 period instead of entirely up-front. This introduces both cash flow benefits and some challenges around cash planning.

15/ The benefit is that until the VC fund has identified an investment opportunity, you get to have that money put to work elsewhere. The drawback is that you need to manage your cash availability just in case the fund makes a capital call.

16/ I get this question phrased almost exactly this way more often than I ever expected.

18/ At the end of the day, unrealized returns don’t mean much, its all about cash on cash returns, or as @cdouvos might say, you need to put the moolah in the coolah and that is going to take some time. How much time….

19/This is another question that’s almost impossible to answer with precision so lets go with broad industry stats

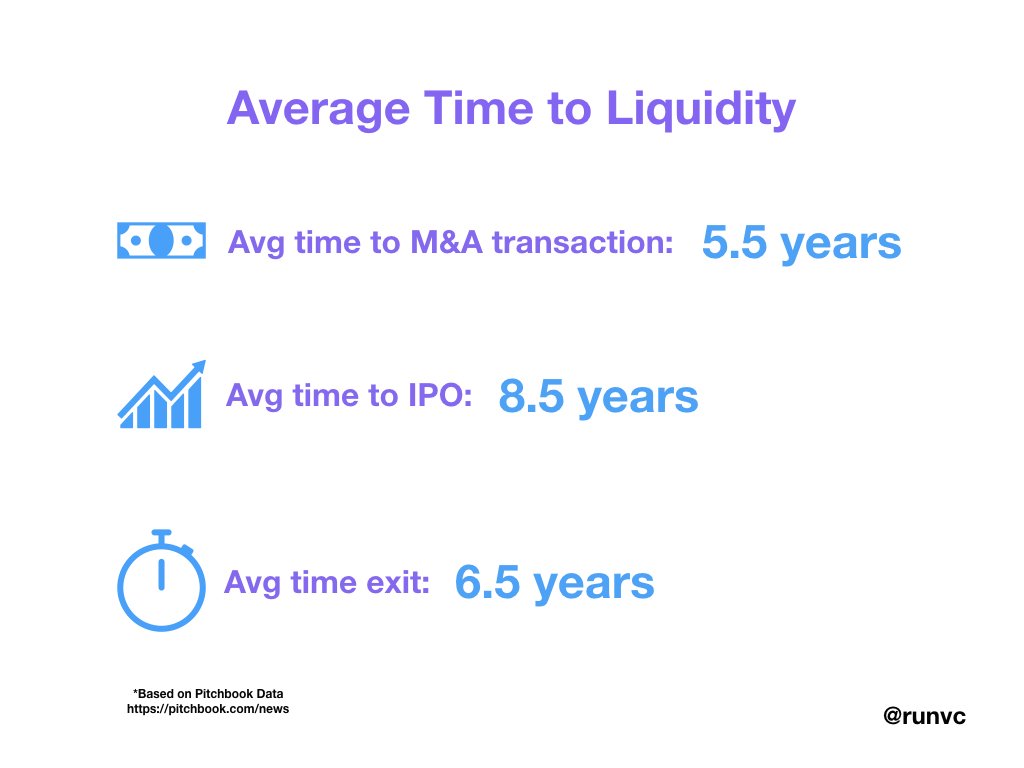

These numbers from @PitchBook start counting from the date of investment in a portfolio company. Funds deploy over 18-36 months so we need to add those months on.

These numbers from @PitchBook start counting from the date of investment in a portfolio company. Funds deploy over 18-36 months so we need to add those months on.

(Missed the slide) 🤦♂️

20/ While the average time to exit stands somewhere around 6.5 years, I believe venture fund investors can expect to start seeing early distributions 2-3 years in with distributions accelerating as a fund ages through its the liquidity sweet spot 7-8 years in.

21/ Anyone can make an investment but can you return an investment, the returning is the most important part…. Anyone can make an investment

22/ Taxes! Everyone’s favorite topic.

Seriously though, what investors really care about is their net cash on cash multiple at the end of the fund and that means net of expenses, fees AND taxes.

**Disclaimer: this is not tax advice, I can’t even do my own taxes**

Seriously though, what investors really care about is their net cash on cash multiple at the end of the fund and that means net of expenses, fees AND taxes.

**Disclaimer: this is not tax advice, I can’t even do my own taxes**

23/

24/ The J curve is a reference to how returns/expenses are realized over the life of a VC fund. When you graph them it tends to take the form of a J. Funds are pass through entities so expenses & write-offs are deductions for investors. Conversely successful exits are gains

25/ Funds tend to incur a large portion of their expenses up front & companies that fail, are more likely to do so early. Thus, investors may see big tax advantages or deductions early on in a fund which they can apply to gains they are seeing from elsewhere in their portfolio.

26/ I am perennially surprised by how few people know about Qualified Small Business Stock (even some early stage venture fund managers). The punchline is that many if not all of the proceeds from small early stage funds may be tax free to the LPs at the federal level. TAX FREE.

27/ Think about how that changes the equation. That hedge fund, timber fund, apartment complex you’re thinking about needs to crush early stage venture to win net of taxes. (I’m biased)

28/ The caveats, the equity needs to be purchased before the company has gross assets of $50M or more and the fund needs to hold the equity for > 5 years. If conditions are met though gains up to 10X cost basis or $10M FOR EACH LP are shielded from fed income tax.

29/ This is where I try to bring everything together for folks.

Who should consider investing in VC?

People who are (a) highly diversified so that they can gain the upside of VC while taking advantage of its ability to de-risk via low correlation AND

Who should consider investing in VC?

People who are (a) highly diversified so that they can gain the upside of VC while taking advantage of its ability to de-risk via low correlation AND

30/ (b) have predictable liquidity needs since much of the capital they invest in VC will be hard to access for 10+ years.

31/ Unfortunately, these two conditions are enough that most people shouldn’t be invested in the asset class but for those who do meet the conditions, they’re substantially undercutting their returns if they don’t have 5%-15% of their portfolio allocated to VC.

32/ I say 5%-15% because that is where many brilliant allocators shake out. These are people way smarter than I, many of whom have CFAs so I don’t argue. The larger your investment corpus & the further you are to the upper right in the above slide, the more you can allocate.

33/ Thats basically it folks.

Also, I'm a dad and I like dad jokes so this is how I usually end it. 🙃

Also, I'm a dad and I like dad jokes so this is how I usually end it. 🙃

Fin/ Again, if you’re pitching your asset class or market you’ve already lost the battle but I hope its interesting or amusing to see how I tell the bull case for VC to people who don't know much about it.

p.s./ I want to thank @ryan_caldbeck's masterful tweet storms for inspiring me to offer more than just my hot takes and @TurnerNovak for sanity checking my fever dream rantings.