,

20 tweets,

4 min read

Read on Twitter

Clearbanc, Shopify, and Stripe have all launched their own version of the same type of loan.

The loans seem sexy and cheap, but they're definitely not. They're borderline predatory.

Let's take a look at why 👇

(1/16)

The loans seem sexy and cheap, but they're definitely not. They're borderline predatory.

Let's take a look at why 👇

(1/16)

Each program works the exact same way. You take out a loan - and return the loan as a percentage of your sales each day.

So, in this example from Shopify, if I make $10K a day in sales, I'll send $1700 daily (17%) to Shopify until I pay off the loan.

(2/16)

So, in this example from Shopify, if I make $10K a day in sales, I'll send $1700 daily (17%) to Shopify until I pay off the loan.

(2/16)

The benefits for the merchant:

"No interest!"

"No paperwork!"

"Easy funding!"

Unfortunately, that's where the fun ends.

(3/16)

"No interest!"

"No paperwork!"

"Easy funding!"

Unfortunately, that's where the fun ends.

(3/16)

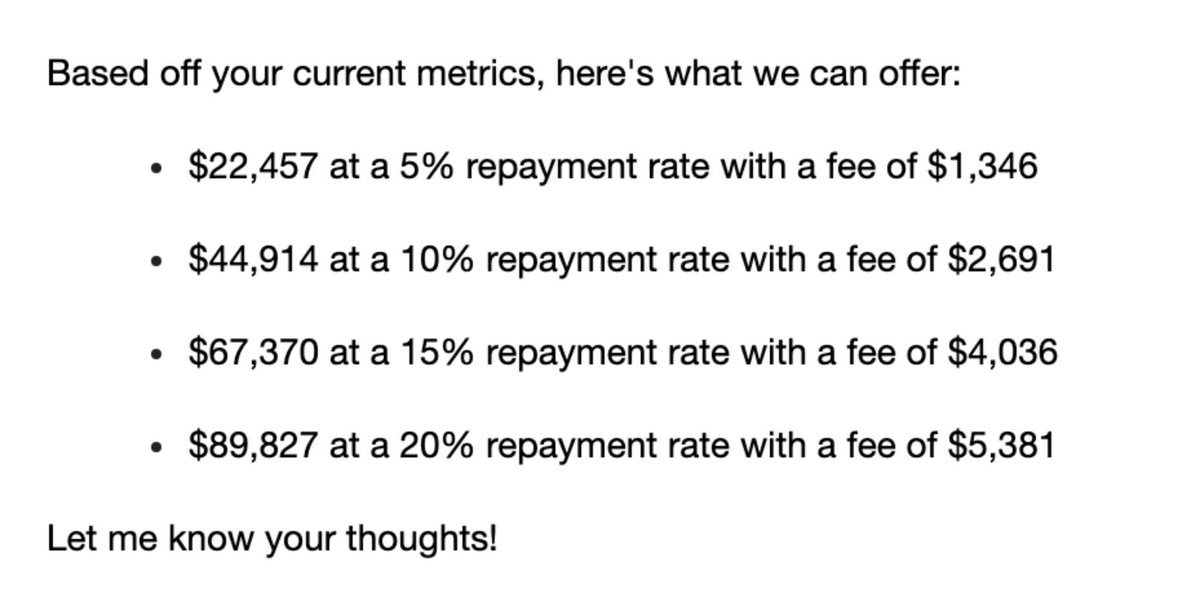

Here is an offer I received from Clearbanc back in January.

Sounds amazing, right? Only a 5-20% fee!

(4/16)

Sounds amazing, right? Only a 5-20% fee!

(4/16)

Oh hey, here's a Business Insider article, telling me that Clearbanc only charges 6% interest! Wow!

(5/16)

(5/16)

That's bull$h!t. And honestly, Business Insider should be ashamed.

These offers actually carry anywhere from a 30%-50% APR, depending on your assumptions for revenue over the coming months.

Read that again.

FIFTY percent APR.

(6/16)

These offers actually carry anywhere from a 30%-50% APR, depending on your assumptions for revenue over the coming months.

Read that again.

FIFTY percent APR.

(6/16)

I'm DEFINITELY no expert at business financing, but I do know that most states have outlawed personal loans at 36% APR or higher. Something to keep in mind.

(7/16)

(7/16)

Back to the math.

When we received that offer from Clearbanc, we were doing roughly $3500 in daily sales, and growing roughly 15% monthly.

They knew this because they used my sales history to calculate the offer they made me.

(8/16)

When we received that offer from Clearbanc, we were doing roughly $3500 in daily sales, and growing roughly 15% monthly.

They knew this because they used my sales history to calculate the offer they made me.

(8/16)

When you model out those assumptions and the loan payback, here's what comes out. A 45% APR.

That's outrageous.

Even if you assume ZERO growth, the APR STILL comes out to 36%.

(9/16)

That's outrageous.

Even if you assume ZERO growth, the APR STILL comes out to 36%.

(9/16)

Let's compare these offers to some other offers I had from more "traditional" lending sources:

American Express offered me 170K at 14% APR

Wells Fargo offered me a 90K line of credit at 8% APR

(Guess which loans I took?)

(10/16)

American Express offered me 170K at 14% APR

Wells Fargo offered me a 90K line of credit at 8% APR

(Guess which loans I took?)

(10/16)

Here's the point. Don't be fooled by the smoke and mirrors of the newer, sexier lending options out there.

There's a reason Clearbanc has raised ONE BILLION dollars. They're getting very rich on very high interest loans.

(11/16)

There's a reason Clearbanc has raised ONE BILLION dollars. They're getting very rich on very high interest loans.

(11/16)

At their best, you can view these lenders as altruistic organizations that are fueling the ecommerce and DTC revolution, making it easy for organizations to get access to capital.

(12/16)

(12/16)

At their worst, you can view them as predatory lenders taking advantage of founders who don't have a financial background and can't see through the marketing.

Come to your own conclusions.

(13/16)

Come to your own conclusions.

(13/16)

But the bottom line is this: Do the math yourself.

I made a spreadsheet you can find at the link below. Make a copy and plug your Clearbanc, Shopify, or Stripe loan offers into the orange cells to calculate your APR.

(14/16)

docs.google.com/spreadsheets/d…

I made a spreadsheet you can find at the link below. Make a copy and plug your Clearbanc, Shopify, or Stripe loan offers into the orange cells to calculate your APR.

(14/16)

docs.google.com/spreadsheets/d…

For a bit more of a balanced take on the subject, read the latest article by @ahhensel (with a small cameo by yours truly).

(15/16)

modernretail.co/startups/a-ban…

(15/16)

modernretail.co/startups/a-ban…

And for the love of God, somebody who is better at this than me - please check my math and let me know if I'm wrong so that I can delete this thread and walk away in shame.

(16/16)

(16/16)

ADDENDUM: a few very smart people have pushed back on this. The essential narrative goes like this:

“Having an option like Clearbanc is better than no option at all.”

(1/4)

“Having an option like Clearbanc is better than no option at all.”

(1/4)

My beef is not with the existence of Clearbanc. I may actually use them in the future, assuming I’m not on a do-not-lend list.

Paying 40% APR is better than giving away another 30% of your company.

(2/4)

Paying 40% APR is better than giving away another 30% of your company.

(2/4)

My issue is with the fact that they shroud the actual cost of their loans in smoke and mirrors.

There’s a reason that federal law requires APR and nominal interest rate to be listed for all consumer loans.

All I want is some Truth in Lending.

(3/4)

There’s a reason that federal law requires APR and nominal interest rate to be listed for all consumer loans.

All I want is some Truth in Lending.

(3/4)

It would take very little effort for Clearbanc to make these estimates available to you.

There’s a reason they don’t.

(4/4)

There’s a reason they don’t.

(4/4)