,

65 tweets,

452 min read

Read on Twitter

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @National_Bank: ANALYSIS OF COOKED FINANCIALS FOR THE PERIOD ENDING 30-SEPTEMBER-2017

---+++---+++---+++---+++

THREAD::::THREAD::::

---+++---+++---+++---+++

@JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @RobertSyundu

---+++---+++---+++---+++

THREAD::::THREAD::::

---+++---+++---+++---+++

@JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @RobertSyundu

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy 1) In November 2015, Blogger Cyprian Nyakundi (Corporate Fraud Assassin) reported that National Bank of Kenya had developed the habit of cooking books of accounts.

cnyakundi.com/rot-at-nationa…

cnyakundi.com/rot-at-nationa…

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy 2) The habit has refused to go away and instead they now do it with utmost arrogance not caring what the public would say and of course with the backing from Opus Dei....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy 3) ...As we said before, we can only compare Wilfred Musau and Hassan Mohamed to a CAT WHICH AFTER STEALING MILK, LEAKS THE WHISPERS WITH IMPUNITY NOT BOTHERED ABOUT THE OPINION OF THE MILK OWNER...

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy 4) ....We promised to procure the services of our BONOKO (street) accountant just to understand (in a nutshell) to what extent Wilfred Musau is misleading investors through CREATIVE ACCOUNTING......

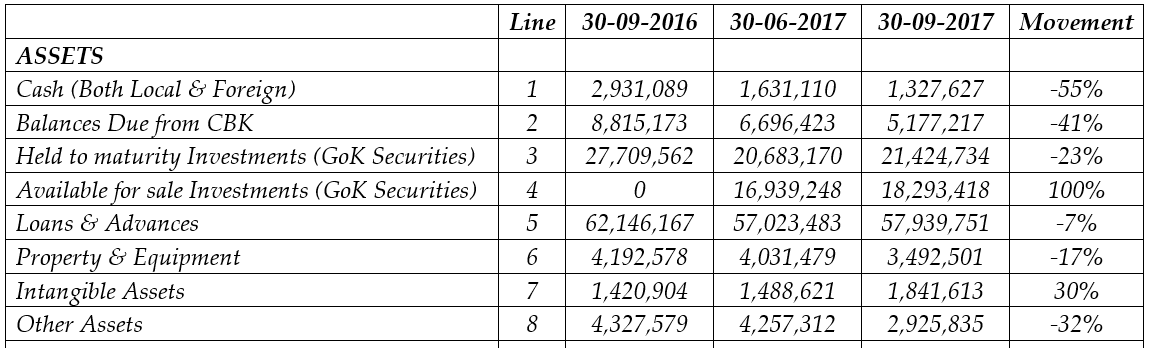

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy 5) ...We have the draft verdict and the Bonoko Accountant is making sense. Below is an excerpt of NBK Published accounts for the period ending 30th September 2017. What follows is a blow-by-blow analysis...

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare 6) ..(A). Referring directly to the @CBKKenya Guidelines, Loans are classified from Grade 1 to Grade 5. PROVISIONING is an Accounting treatment which applies to BAD DEBTS beyond recovery....

centralbank.go.ke/policy-procedu…

centralbank.go.ke/policy-procedu…

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare 7) ...

....The term “STATUTORY RESERVES” as captured on line 16 of the image above is only applicable to Grades 1 and 2. Grade 1 accounts are deemed to be operating normally and attracts Loan Loss provision of 1% while Grade 2 are classified as Watch accounts and attracts...

....The term “STATUTORY RESERVES” as captured on line 16 of the image above is only applicable to Grades 1 and 2. Grade 1 accounts are deemed to be operating normally and attracts Loan Loss provision of 1% while Grade 2 are classified as Watch accounts and attracts...

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare 8) ....

....additional 2% on provisions. In total, Statutory Loan Loss Reserves is a one-off 3% of the loan portfolio. It is one-off because it’s only levied once in the life of a loan....

....additional 2% on provisions. In total, Statutory Loan Loss Reserves is a one-off 3% of the loan portfolio. It is one-off because it’s only levied once in the life of a loan....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare 9) ....

...Now here is the KITCHEN-WORK. For such reserves to increase by KSH 1 Billion as seen in line 16, Loan Portfolio ought to have grown by at least KSH 33 Billion.

According to Line 5 of the above image, Loans and advances ought to have been at least KSH 95 Billion...

...Now here is the KITCHEN-WORK. For such reserves to increase by KSH 1 Billion as seen in line 16, Loan Portfolio ought to have grown by at least KSH 33 Billion.

According to Line 5 of the above image, Loans and advances ought to have been at least KSH 95 Billion...

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare 10) ...

....However what we are seeing is a reduction of the loan portfolio from KSH 62 Billion to KSH 57 Billion. A reduction in the portfolio by KSH 5 Billion should invoke a write-back of about KSH 150 Million back to the P&L.....

....However what we are seeing is a reduction of the loan portfolio from KSH 62 Billion to KSH 57 Billion. A reduction in the portfolio by KSH 5 Billion should invoke a write-back of about KSH 150 Million back to the P&L.....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare 11) ....

.....Because there was no growth of portfolio, The KSH 1 Billion hidden under Statutory reserves is an actual loan loss which ought to have been captured on the Profit and loss account. If you adjust this hidden loss amount to NBK.....

.....Because there was no growth of portfolio, The KSH 1 Billion hidden under Statutory reserves is an actual loan loss which ought to have been captured on the Profit and loss account. If you adjust this hidden loss amount to NBK.....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare 12) ...

......September accounts, you will increase the comprehensive loss position from KSH 6.164 Million to a staggering loss of KSH 935 Million......

......September accounts, you will increase the comprehensive loss position from KSH 6.164 Million to a staggering loss of KSH 935 Million......

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare 13) ...

...Now tell me, why is Wilfred Musau misleading Investors? Why is CBK Gov. allowing this to happen? Patrick Njoroge boasts of having worked with @IMFNews, .....

...Now tell me, why is Wilfred Musau misleading Investors? Why is CBK Gov. allowing this to happen? Patrick Njoroge boasts of having worked with @IMFNews, .....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 14) ...

....what was he doing there if he cannot even comprehend simple accounting treatments? Was he a sweeper or a Chaplain at the IMF Offices?

....what was he doing there if he cannot even comprehend simple accounting treatments? Was he a sweeper or a Chaplain at the IMF Offices?

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 15) ..(B). In June 2017, NSSF injected KSH 3 Billion to National bank as a loan which should have been captured as a liability even if it was a non-interest earning instrument.....

businessdailyafrica.com/corporate/NSSF…

businessdailyafrica.com/corporate/NSSF…

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 16) ...

....However, out of their own wisdom or lack of it, Wilfred Musau & Hassan Mohamed decided not to capture this anywhere. Shockingly, there is an entry for borrowed funds captured as NIL on line 12 of the image.....

....However, out of their own wisdom or lack of it, Wilfred Musau & Hassan Mohamed decided not to capture this anywhere. Shockingly, there is an entry for borrowed funds captured as NIL on line 12 of the image.....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 17) ...

..The Impact of these funds on the loan portfolio is also not evident as the portfolio shrunk. Therefore any argument suggesting that the funds were offloaded to customers must be resisted.....

..The Impact of these funds on the loan portfolio is also not evident as the portfolio shrunk. Therefore any argument suggesting that the funds were offloaded to customers must be resisted.....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 18) .....

.....In short, Wilfred Musau & Hassan Mohammed (the protected criminals) may have once again spirited away with NHIF contributions.....

.....In short, Wilfred Musau & Hassan Mohammed (the protected criminals) may have once again spirited away with NHIF contributions.....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 19) ..

....This time around, they have a new Chief-chef in town called Peter Kioko as the Chief Risk Officer.

Peter Kioko, a longtime friend of Wilfred Musau was frog-matched from the Fast Moving Consumer Goods (FMCG) Industry to come and implement creative accounting in NBK....

....This time around, they have a new Chief-chef in town called Peter Kioko as the Chief Risk Officer.

Peter Kioko, a longtime friend of Wilfred Musau was frog-matched from the Fast Moving Consumer Goods (FMCG) Industry to come and implement creative accounting in NBK....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 20) ...

....He has over 20 years of experience in creative accounting in the FMCG. He goes around Nairobi CBD boasting how no company can make a loss as long as he is the CFO. .....

....He has over 20 years of experience in creative accounting in the FMCG. He goes around Nairobi CBD boasting how no company can make a loss as long as he is the CFO. .....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 21)...(C) Retained Earnings is simply profit retained and for a company that has been around for more than a year, it’s a cumulative figure of profits unpaid as dividends. As a result, if a company makes profit, the figure goes up in the following accounting period....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 22) ...

...On the other hand when losses as are encountered, the figure goes down and eats up on the core capital (Tier 1 capital) of the institution....

From Line 15 of the above image, you will notice that as of 30th September 2016, Retained Earnings were KSH. 3.2 Billion...

...On the other hand when losses as are encountered, the figure goes down and eats up on the core capital (Tier 1 capital) of the institution....

From Line 15 of the above image, you will notice that as of 30th September 2016, Retained Earnings were KSH. 3.2 Billion...

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 23) ...

...followed by a KSH 3.06 Billion in June 2017.

We are all aware National Bank has not declared a loss which leaves all intelligent people wondering how the figure suddenly shrank to KSH 1.8 Billion. Could there be a hidden loss somewhere? ....

...followed by a KSH 3.06 Billion in June 2017.

We are all aware National Bank has not declared a loss which leaves all intelligent people wondering how the figure suddenly shrank to KSH 1.8 Billion. Could there be a hidden loss somewhere? ....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 24) ...

..Why are these two criminals (Wilfred Musau & Hassan Mohamed) testing the investor intelligence? Where is @CBKKenya and @CMAKenya who must give a go-ahead before accounts are published? .....

..Why are these two criminals (Wilfred Musau & Hassan Mohamed) testing the investor intelligence? Where is @CBKKenya and @CMAKenya who must give a go-ahead before accounts are published? .....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 25) ...

...At least we know Audit firms sends inexperienced associates to deal with hardcore criminals like Hassan Mohamed & Wilfred Musau who in turn outmaneuvers them in Banking matters......

...At least we know Audit firms sends inexperienced associates to deal with hardcore criminals like Hassan Mohamed & Wilfred Musau who in turn outmaneuvers them in Banking matters......

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 26) ...

....But a regulator like CBK must have qualified IDEOTS to do the job rather than having Opus Dei like Patrick Njoroge who continuously apply make-up and rushes to his one bedroom apartment every evening.

....But a regulator like CBK must have qualified IDEOTS to do the job rather than having Opus Dei like Patrick Njoroge who continuously apply make-up and rushes to his one bedroom apartment every evening.

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 27) ...(D) Paid up share capital is known as Tier 1 capital in the financial sector. It’s against this figure that many relevant banking ratios are derived to determine the FINANCIAL SOUNDNESS of a banking institution....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 28) ...

...Some of the Ratios are: Capital Adequacy Ratios, Earnings Ratios, Bad Loan ratios, employee productivity ratios best captured on overheads and liquidity ratios among others. ...

...Some of the Ratios are: Capital Adequacy Ratios, Earnings Ratios, Bad Loan ratios, employee productivity ratios best captured on overheads and liquidity ratios among others. ...

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 29) ...

...Rogue Banks like National Bank Will MASSAGE the SOURCE NUMBERS that affect these ratios because according to them, FINANCIAL SOUNDNESS MUST BE FORCED ON INVESTORS....

...Rogue Banks like National Bank Will MASSAGE the SOURCE NUMBERS that affect these ratios because according to them, FINANCIAL SOUNDNESS MUST BE FORCED ON INVESTORS....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 30) .....

... If Wilfred Musau together with his CREATIVE ACCOUNTANT (Peter Kioko) correctly declared the 1 Billion loss, they would have been RED on all the Financial Soundness Ratios......

... If Wilfred Musau together with his CREATIVE ACCOUNTANT (Peter Kioko) correctly declared the 1 Billion loss, they would have been RED on all the Financial Soundness Ratios......

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 31) ...

..Looking at Line 13 of the above image, you will realize core capital increased from KSH 7.21 Billion to KSH 7.37 Billion without disclosure on activities that led to this. We already know how the RIGHTS ISSUE was squandered by MUSAU & HASSAN....

..Looking at Line 13 of the above image, you will realize core capital increased from KSH 7.21 Billion to KSH 7.37 Billion without disclosure on activities that led to this. We already know how the RIGHTS ISSUE was squandered by MUSAU & HASSAN....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 32) ...

...and as a result never took place.

So where is the additional paid up capital coming from? Could it be a BALANCING FIGURE for accounts that have refused to balance? Or was it meant to reduce the SEVERITY OF NON-COMPLIANCE with some CBK ratios? .....

...and as a result never took place.

So where is the additional paid up capital coming from? Could it be a BALANCING FIGURE for accounts that have refused to balance? Or was it meant to reduce the SEVERITY OF NON-COMPLIANCE with some CBK ratios? .....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 33) ...

...Already we can see Core Capital as a ratio of Risk Weighted Assets is UNDER WATER by 0.7% while the Total Capital (Tier 2 capital) ratio is SUBMERGED by 3.2%.....

...Already we can see Core Capital as a ratio of Risk Weighted Assets is UNDER WATER by 0.7% while the Total Capital (Tier 2 capital) ratio is SUBMERGED by 3.2%.....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 34) ....

...The misreporting of this figure was engineered by the Chief crooks (Wilfred Musau & Hassan Mohammed) with direct supervision from CELIBACY EXPERT PATRICK NJOROGE, THE GITHERI MEDIA SENSATION.

...The misreporting of this figure was engineered by the Chief crooks (Wilfred Musau & Hassan Mohammed) with direct supervision from CELIBACY EXPERT PATRICK NJOROGE, THE GITHERI MEDIA SENSATION.

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 35) When a company employs incompetent crooks like Hassan Mohamed and the entire group of MUNIR REMNANTS, they survive on excuses and deception meant to satisfy their greed and deepen their pockets. A few pointers are captured next:

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 36) ..(A) Line 17 (Other Reserves) and Line 24 (Fair Value Changes in Financial Assets) in the above image seems to be affected by similar events owing to their trend. We accept correction from fellow Bonoko Accountants.

National bank has a website & ...

nationalbank.co.ke/investor-relat…

National bank has a website & ...

nationalbank.co.ke/investor-relat…

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 37) ...

...being a publicly listed company, they are obliged to make public there accounts whether cooked or not. There only hope is that the consumers of such information is not sophisticated enough to digest the fine-print.

From the financial accounts in there website, .....

...being a publicly listed company, they are obliged to make public there accounts whether cooked or not. There only hope is that the consumers of such information is not sophisticated enough to digest the fine-print.

From the financial accounts in there website, .....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 38) ...

..you will notice that the events leading to losses on these financial instruments have been consistent for a few years. This begs the question: “Why continue holding financial instruments whose value depreciates every year?”......

..you will notice that the events leading to losses on these financial instruments have been consistent for a few years. This begs the question: “Why continue holding financial instruments whose value depreciates every year?”......

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 39) ....

...It is almost guaranteed the same instruments will depreciate next year. Now if you did not know, this is the DEFINITION OF INCOMPETENCE......

...It is almost guaranteed the same instruments will depreciate next year. Now if you did not know, this is the DEFINITION OF INCOMPETENCE......

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 40) ...(B) In the face of Rate capping, Government securities stood out as sources of high-yielding investment. On Line 2 & 3, you will notice National Bank Assets continued to shrink (on CBK and Government securities), reminiscent of........

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 41) ...

...a company approaching foreclosure and certainly an investment cheat-sheet.

Then a surprise figure (Line 4) designed to balance runaway unexplained liabilities shows up as Government instruments available for sale at KSH 18 Billion from ZERO in 2016......

...a company approaching foreclosure and certainly an investment cheat-sheet.

Then a surprise figure (Line 4) designed to balance runaway unexplained liabilities shows up as Government instruments available for sale at KSH 18 Billion from ZERO in 2016......

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 42) ....

.....It must be a PLEASANT COINCIDENCE that INVESTMENT INSTRUMENTS WERE DESIGNED TO SUDDENLY MATURE WITHOUT NOTICE.

Could it be that NBK does not have a TREASURY DEPARTMENT TO MONITOR MATURITY OF INVESTMENT INSTRUMENTS WITH PLANS OF QUICK REINVESTMENTS?........

.....It must be a PLEASANT COINCIDENCE that INVESTMENT INSTRUMENTS WERE DESIGNED TO SUDDENLY MATURE WITHOUT NOTICE.

Could it be that NBK does not have a TREASURY DEPARTMENT TO MONITOR MATURITY OF INVESTMENT INSTRUMENTS WITH PLANS OF QUICK REINVESTMENTS?........

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 43) ...

....We Refuse to believe this argument. The Creative CFO (Peter Kioko) found it easy to introduce a balancing figure against treasury instruments because Audit Firms lack the experience to understand treasury instruments and rightfully so because they lay emphasis.......

....We Refuse to believe this argument. The Creative CFO (Peter Kioko) found it easy to introduce a balancing figure against treasury instruments because Audit Firms lack the experience to understand treasury instruments and rightfully so because they lay emphasis.......

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 44) ....

...on theories while banking criminals concentrate on understanding Operationalization.

...on theories while banking criminals concentrate on understanding Operationalization.

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 45) ...(C) NATIONAL BANK is on record having sold most of its assets where Wilfred Musau (Current MD), Sheikh Munir (Former MD) and Hassan Mohamed (DUALE’S MONEY LAUNDERING AGENT) single-handedly assumed ownership of those properties through proxies...

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 46) ..

..We are informed the Trio pushed the sale of these assets to there proxies at the book values rather than the fair values. For instance, a branch which was valued at KSH 50M 10 years ago was sold at that price with total disregard to the actual market value for KSH 180M..

..We are informed the Trio pushed the sale of these assets to there proxies at the book values rather than the fair values. For instance, a branch which was valued at KSH 50M 10 years ago was sold at that price with total disregard to the actual market value for KSH 180M..

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 47) ...

....The Ignorant shareholders then continue wondering why the much hyped sale of assets failed to achieve its purpose of shoring up core capital. Off course the Githeri Media sensation (CBK’s Beauty Pageant Patrick Njoroge) as a partner in shoddy transactions with.....

....The Ignorant shareholders then continue wondering why the much hyped sale of assets failed to achieve its purpose of shoring up core capital. Off course the Githeri Media sensation (CBK’s Beauty Pageant Patrick Njoroge) as a partner in shoddy transactions with.....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 48) ...

....most banks (including KCB’s Oigara) is not a dependable watch-dog for shareholders. Shareholders must however be informed that Foolishness can never be forgiven even by God....

....most banks (including KCB’s Oigara) is not a dependable watch-dog for shareholders. Shareholders must however be informed that Foolishness can never be forgiven even by God....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 49) ....

...Having sold most of its assets, NBK was left with more permanent assets whose Expected life (Leases) are longer with minimal depreciation.

It is therefore shocking that National bank properties experiences accelerated depreciation within 1 year.....

...Having sold most of its assets, NBK was left with more permanent assets whose Expected life (Leases) are longer with minimal depreciation.

It is therefore shocking that National bank properties experiences accelerated depreciation within 1 year.....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 50) ...

....You will notice on Line 6 of the image that properties’ book value condensed by KSH 700 Million which is weird for assets having long life (Leases).....

....You will notice on Line 6 of the image that properties’ book value condensed by KSH 700 Million which is weird for assets having long life (Leases).....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 51) ...

...On the other hand on line 21, the cumulative depreciation for the year quoted as KSH 369 Million did not match the movement in book values.

MUSAU must have noted that correct entry of the depreciation figure could plunge his books of accounts to a further loss......

...On the other hand on line 21, the cumulative depreciation for the year quoted as KSH 369 Million did not match the movement in book values.

MUSAU must have noted that correct entry of the depreciation figure could plunge his books of accounts to a further loss......

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 52) ..

....You know he must demonstrate Financial soundness to unsuspecting shareholders. By the way, all Pension contributors (NSSF) are shareholders of NBK. One of these fine days there will be violent demonstrations across the country against NBK Looters....

....You know he must demonstrate Financial soundness to unsuspecting shareholders. By the way, all Pension contributors (NSSF) are shareholders of NBK. One of these fine days there will be violent demonstrations across the country against NBK Looters....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 53) ...(D) Intangible assets in a bank is mainly the Software. Core Banking System forms the biggest part of this. Remember we talked about how National Bank criminals looted the bank in the pretext of system upgrade? .......

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 54) ..

....We stated with certainty how an upgrade from the same platform did not require Accelerated amortization. Yet as you can see on Line 7 of the above image, A KSH 400 Million amortization has been recorded.....

....We stated with certainty how an upgrade from the same platform did not require Accelerated amortization. Yet as you can see on Line 7 of the above image, A KSH 400 Million amortization has been recorded.....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 55) ....

...While Wilfred Musau decided to hide Actual Loan Loss provisions disguising them as statutory reserves, he found it necessary to pass a systems amortization of KSH 400 Million because according to him, Looting comes first before the Pensioners (shareholders)......

...While Wilfred Musau decided to hide Actual Loan Loss provisions disguising them as statutory reserves, he found it necessary to pass a systems amortization of KSH 400 Million because according to him, Looting comes first before the Pensioners (shareholders)......

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 56) ..(E) According to Line 18 of the above image, Interest income from Loans reduced by 51% from KSH 7.6 Million to KSH 3.7 Million. While it is easier to blame the Interest rate capping for incompetence, you will notice that the average rate banks were charging before.....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 57) ..

...capping was 18% per annum which reduced to 14% after rate capping.

This means that if you had a performing loan portfolio of KSH 42 Billion you would earn KSH 7.56 Billion per annum of interest income as compared to KSH 5.88 Billion after rate capping......

...capping was 18% per annum which reduced to 14% after rate capping.

This means that if you had a performing loan portfolio of KSH 42 Billion you would earn KSH 7.56 Billion per annum of interest income as compared to KSH 5.88 Billion after rate capping......

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 58) ..

....The reduction as a result of rate capping would be 22% and anything else like 51% is pure incompetence. Blaming rate capping is simply a convenient way for looters with no institutional growth strategy.....

....The reduction as a result of rate capping would be 22% and anything else like 51% is pure incompetence. Blaming rate capping is simply a convenient way for looters with no institutional growth strategy.....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 59) ...

....You will notice that reduction of rates was meant to be good for the banks who were complaining about high default rates. Lower rates means lesser repayment amount by borrowers and hence lesser default rates......

....You will notice that reduction of rates was meant to be good for the banks who were complaining about high default rates. Lower rates means lesser repayment amount by borrowers and hence lesser default rates......

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 60) ...

....As a result, Efficient banks would use that as an opportunity to plough back suspended interest (in the suspense account) back to profit and loss account.

....As a result, Efficient banks would use that as an opportunity to plough back suspended interest (in the suspense account) back to profit and loss account.

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 61) ...(F) Last but not least, looking at Line 23 we see an item named Other Operating costs. We are told this item is mainly for marketing. BERNADETTE NGARA, a woman with a CUTTING EDGE APPETITE for Ben 10s (and we say so because she only employs her boyfriends.....

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 62) ...

...In exchange for a good salary, the boys MUST PERSEVERE a harsh environment of cartilages) has over KSH 1.5 B of marketing budget annually.

She has a target from HASSAN & MUSAU to come up with all sorts of marketing tricks just to make sure the KSH 1.5B is exhausted.

...In exchange for a good salary, the boys MUST PERSEVERE a harsh environment of cartilages) has over KSH 1.5 B of marketing budget annually.

She has a target from HASSAN & MUSAU to come up with all sorts of marketing tricks just to make sure the KSH 1.5B is exhausted.

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 63) Remember we made some promises in our previous articles? It is not in our nature to forget and rest assured, we will keep our promise. For instance, Insider loans as captured on Line 26 of the above image is given as KSH 26 Million......

@Disembe @National_Bank @CreditSuisse @Asamoh @KPMGEastAfrica @njorogep @DeutscheBank @RobertSyundu @commerzbank @NseKenya @CMAKenya @C_NyaKundiH @CBKKenya @JoshuaOigara @Saagite @hawklead1 @MigunaMiguna @citizentvkenya @TheStarKenya @Ihrm_Kenya @IFCAfrica @KCBGroup @DCI_Kenya @EACCKenya @WorldBankKenya @ODPP_KE @BelAkinyii @KinyanBoy @KTNKenya @OleItumbi @KBonimtetezi @ItsMutai @HFGroupCare @IMFNews 64) ....More than Half of the Islamic Banking Portfolio are loans belonging to the Criminal Chairman (Hassan Mohamed) through proxies. A very loud example is AINUSHAMSI LIMITED. However, this is news for another day.

BOOM!!!!!!!!

BOOM!!!!!!!!