Posted a new draft of a paper with @sgil1122: "Heterogeneous Real Estate Agents and the Housing Cycle"

In it, we document several interesting empirical facts about housing + RE agents, and use them to discuss aggregate liquidity of housing.

paulgp.github.io/papers/Heterog…

Thread👇🏼

In it, we document several interesting empirical facts about housing + RE agents, and use them to discuss aggregate liquidity of housing.

paulgp.github.io/papers/Heterog…

Thread👇🏼

The housing market is a great example of a search market -- rather than a central clearing price for good, there exist many bilateral negotiations and matches.

An under-appreciated feature of this (a key feature in labor search models): many houses listed for sale fail to sell!

An under-appreciated feature of this (a key feature in labor search models): many houses listed for sale fail to sell!

As we see above, even during boom periods, only 70 percent of listed homes sell within a year. During the housing bust, this rate plummeted to below fifty percent! We term this the "liquidity" of the market.

We focus on a central feature of this market:

real estate agents.

We focus on a central feature of this market:

real estate agents.

Becoming a real estate agent is easy: in some states, it's as simple as 30 hours of classes and a $50 exam fee.

Moreover, due to the structure of commissions in the U.S., brand-new, inexperienced agents end up charging the same commission (2.5-3%) as veterans of the industry.

Moreover, due to the structure of commissions in the U.S., brand-new, inexperienced agents end up charging the same commission (2.5-3%) as veterans of the industry.

Hsieh and Moretti (2003) showed that this structure caused welfare loss as due to over-entry (& money spent on business stealing).

We use data on 10.4 million listings across 60 different listing platforms in the U.S. to show that this has large implications for the *clients*.

We use data on 10.4 million listings across 60 different listing platforms in the U.S. to show that this has large implications for the *clients*.

Two reasons why:

First, inexperienced agents (where experience is measured as listing activity in the previous calendar year) have huge market share.

Brand-new agents make up 30% of agents!

25% of listings are handled by agents with experience of 4 or less.

First, inexperienced agents (where experience is measured as listing activity in the previous calendar year) have huge market share.

Brand-new agents make up 30% of agents!

25% of listings are handled by agents with experience of 4 or less.

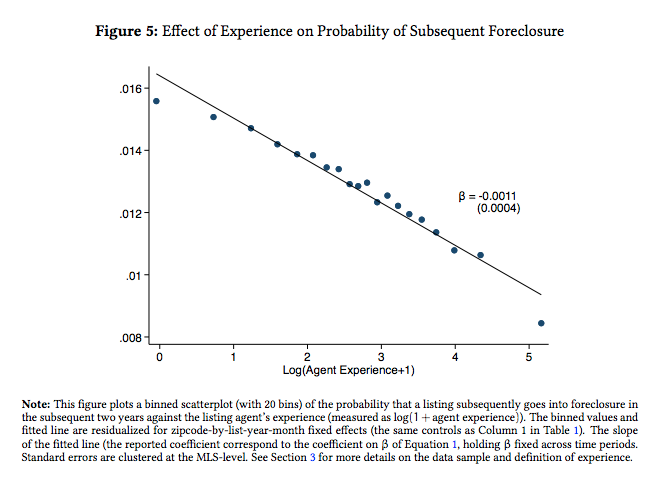

Second,

experience appears extremely important for housing liquidity. Moreover, it particularly matters when the housing market collapses.

experience appears extremely important for housing liquidity. Moreover, it particularly matters when the housing market collapses.

Two types of selection can confound our results: selection on property (or listing) characteristics and selection on listing client characteristics. For example, a more experienced agent might select to work with easy-to-sell properties or with more motivated clients.

The first is easier to deal with: we focus on within zipcode-listing-year-month variation, controlling for a many observables about the house, with the assumption that agents are "as-if" randomly matched within these covariates.

For the second, we do a lot of robustness tests: as an example, we control for the amount of home equity that a homeowner has accrued (to address those with more or less "urgency" to sell). We also focus on a sample of motivated sellers who need to sell their home.

Given our estimates, can we say how much real estate agent experience contributed to the drop in listing

liquidity in the recent housing bust? Can we talk about a counterfactual using just the regression analysis?

Our argument: no. Agent experience is highly endogeneous!

liquidity in the recent housing bust? Can we talk about a counterfactual using just the regression analysis?

Our argument: no. Agent experience is highly endogeneous!

We need a model that features:

1) agents who match houses

2) aggregate shocks

3) experience accumulation

Turns out solving for an equilibrium of a heterogeneous agent model with aggregatefluctuations is challenging. We adopt an oblivious equilibrium concept.

1) agents who match houses

2) aggregate shocks

3) experience accumulation

Turns out solving for an equilibrium of a heterogeneous agent model with aggregatefluctuations is challenging. We adopt an oblivious equilibrium concept.

Takeaway from the model is: shifting the economic incentives for entry and exit (increased entry costs, lower commission rates and decreasing the share of uninformed clients) all lead to higher aggregate liquidity, but they have different effects on seller welfare and employment!

Another key takeaway is that the level of these gains is much more modest than what we could construct with a simple back-of-the-envelope focus on regression coefficients. That's because free entry creates competition for experience!

The tension between experience for agents (an "investment") and free entry causes a world where a new entry into the housing market takes away the ability for someone else to gain experience.

There's a lot more in the paper (and we address questions regarding pricing as well!), please take a look!

paulgp.github.io/papers/Heterog…

paulgp.github.io/papers/Heterog…

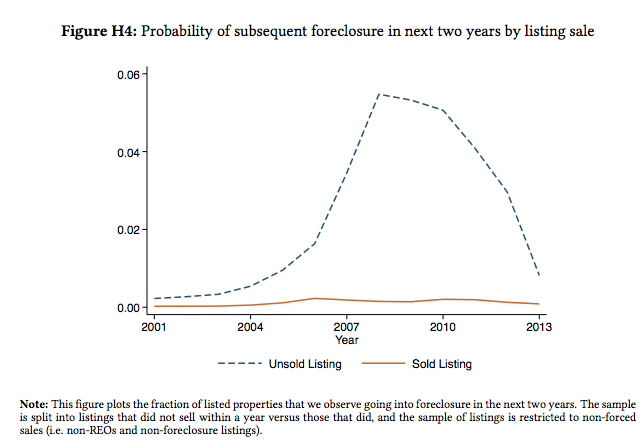

As a postscript: you might say, well, why do I care about liquidity? One neat empirical fact that we show is that for normal listings (non-REO, non-foreclosure), the probability of *subsequent* foreclosure (in the next two years) is highly correlated with agent experience.

Why? Well the homes that list and sell don't go into foreclosure. But those that do not sell are highly likely to go into foreclosure during the crisis. Since experience has large effects on the probability of listing sale, it's natural that this maps across!