1/ Anatomy of Commodity Futures Risk Premia (Szymanowska, Roon, Nijman, van den Goorbergh)

"A single factor, high-minus-low from basis sorts, explains the cross-section of spot premia. Two additional basis factors are needed to explain the term premia."

papers.ssrn.com/sol3/papers.cf…

"A single factor, high-minus-low from basis sorts, explains the cross-section of spot premia. Two additional basis factors are needed to explain the term premia."

papers.ssrn.com/sol3/papers.cf…

2/ "Holding" = hold to maturity (spot+term premia)

"Short Roll" = roll every period (2 months)

"Excess Holding" = long Holding and short Short Roll (isolates term premia → maturity)

"Spreading" = roll calendar spreads (isolates term premium at one point on the term structure)

"Short Roll" = roll every period (2 months)

"Excess Holding" = long Holding and short Short Roll (isolates term premia → maturity)

"Spreading" = roll calendar spreads (isolates term premium at one point on the term structure)

3/ For futures returns, "differences between maturities are larger for Holding than Short Roll returns.

"As Holding returns are the sum of Short Roll and Excess Holding returns, these differences are due to the term premia, which are more distinct in longer maturity contracts."

"As Holding returns are the sum of Short Roll and Excess Holding returns, these differences are due to the term premia, which are more distinct in longer maturity contracts."

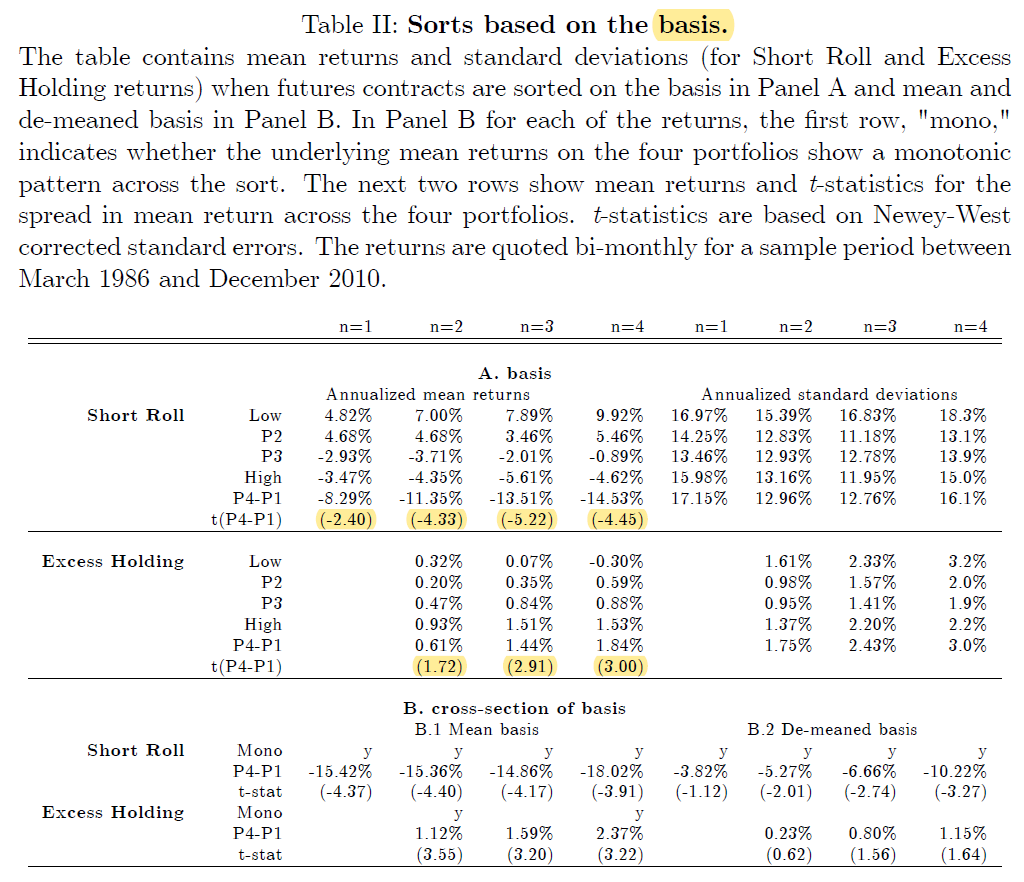

4/ "Commodities with the lowest basis have the highest mean returns."

The term premia (from Excess Holding returns) are smaller and have the opposite sign: holding carry portfolios to maturity underperforms rolling early. (Carry seems to be stronger for longer-dated contracts.)

The term premia (from Excess Holding returns) are smaller and have the opposite sign: holding carry portfolios to maturity underperforms rolling early. (Carry seems to be stronger for longer-dated contracts.)

5/ Results are robust to using different samples, controlling for seasonality, and removing the effect of interest rates from the basis.

"70% of the spot and term premia is due to sorting on the (in-sample) mean. The remaining 30% is due to sorting on deviations from the mean."

"70% of the spot and term premia is due to sorting on the (in-sample) mean. The remaining 30% is due to sorting on deviations from the mean."

6/

7/ The authors also test

* cross-sectional momentum (12-month trailing returns)

* variance scaled by mean return (volatility corrected for momentum)

* inflation beta

* dollar beta

* hedging pressure

* open interest

* liquidity

* cross-sectional momentum (12-month trailing returns)

* variance scaled by mean return (volatility corrected for momentum)

* inflation beta

* dollar beta

* hedging pressure

* open interest

* liquidity

8/ "Except for the US dollar and open interest, sorting on other forecasting variables yields similar patterns in spot and term premia as sorting on the basis: the order of magnitude is often similar, with term premia being of the opposite sign and much smaller than spot premia."

9/ "The basis factor explains almost all of the spot [Short Roll] premia but cannot explain the term [Excess Holding] premia in our sample."

10/ "These graphs show that the mean returns line up with their beta with respect to the beta factor. The (absolute) correlations between the mean returns and the betas are all about 0.80."

11/ "Two basis factors from Spreading returns capture most of the cross-sectional variation in the term premia. These factors are different from the basis factor that explains the spot premia, implying that we need three factors (total) to explain both the spot and term premia."

12/ "Overall, none of the factor portfolios comes close to the performance of the basis factor.... Spot premia are better characterized by the basis factor than by any one of the other factors."

13/ "None of the factors based on the other forecasting variables comes close to the explanatory power of the two basis factors."