At the end of last year, we highlighted our theme that 2020 would likely hew to around a 1.8%ish year (on real #GDP, Core #PCE, the 10-Year UST and the #Fed Funds Rate), but there are some other areas in which variations on this numeric guidepost also seem relevant too.

For instance, we’ve been impressed that the 3-month moving average on #payrolls resides now at 184,000, although it may well decelerate somewhat from that pace as the year goes on.

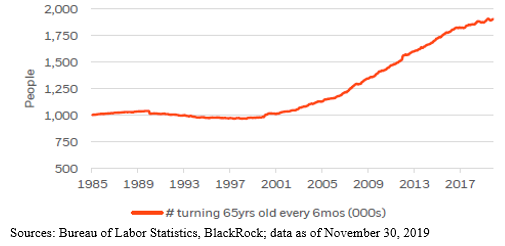

Further, roughly 1.8 million people will be hitting their formal #retirement age (65 years) every six months in 2020, which is nearly double the pace from just 20 years ago!

These new retiree households are bringing with them nearly $1.8 trillion in #financial asset demand growth per year (given 2019’s strong risk asset performance), and they will have a very real need for income-producing #assets as they transition #portfolios to retirement phase.

To us, this suggests that #equity #market returns are likely to concentrate around the corporations that are driving the almost $1.8 trillion-ish level of share buybacks, #dividends and research and development spend in the S&P 500, a good mix of high yielders and high growers.

With the potential for greater demand for the #equity asset class from those using it as an #income proxy, we wouldn’t be surprised to see financial #capital flows reverse somewhat from last year’s trend, and indeed, it appears that move may already have begun.

• • •

Missing some Tweet in this thread? You can try to

force a refresh