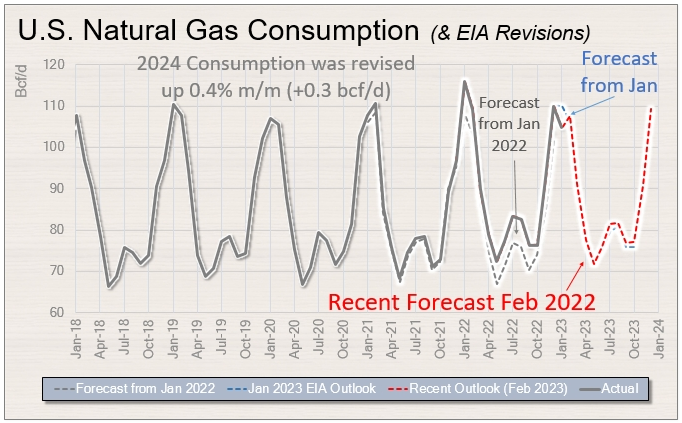

Could we see a NYMEX natural gas price spike this winter? The U.S. just might not be able to rely on 'cheap' Canada natgas imports w/ western CDN storage near record lows (at only 71% full).

A thread on CDN natural gas dynamics #AECO #oilandgas #LNG #alberta

A thread on CDN natural gas dynamics #AECO #oilandgas #LNG #alberta

A number of issues why CDN natgas storage is low, but we've already begun to see a reversal, with AECO difs improving dramatically over the last week (now at US$2.50/mcf). Last time storage was at current levels, the differential went on to reach $0.50/mcf a year later; 2/ #NYMEX

Despite CDN natural gas producing at record levels (17.2 bcf/d and ~1 bcf/d higher than last year), maintenance issues and other factors have yet to contribute to higher CDN natgas storage levels; /3

Canadian natgas consumption is ~0.5 bcf/d higher than last year, taking up some excess production; 4/

But CDN natgas net exports continue to be higher y/y as well. As we've seen in the past, if Canada continues to have infrastructure issues, combined with a cold winter (and low CDN natgas storage), the export market might fall to levels seen in back in 2019; /5 #nymex #AECO

• • •

Missing some Tweet in this thread? You can try to

force a refresh