EIA came out with their Short Term Energy Outlook

- These are the largest revisions in key data points impacting oil markets today. Although many of the adjustments are small, it shows the directional bias the EIA sees with its forecast models - a thread

#oott #oilandgas #WTI

- These are the largest revisions in key data points impacting oil markets today. Although many of the adjustments are small, it shows the directional bias the EIA sees with its forecast models - a thread

#oott #oilandgas #WTI

With China showing more signs of opening, oil demand was revised up 1% (160 mb/d). Is there more oil demand revisions to come? Possibly. Expected crude demand in 2023 is still only up 5% to 15.8 mln b/d (from 14.4 mln b/d in 2020) #oott

U.S. oil production in 2024 was lowered 1.4% (150 mb/d) - with much of this oil supply decline near the back-end of the year. As earning season progresses (and capex budgets are revised), we may see more estimate revisions to come #crude #permian #eagleford #midland #bakken

Outside of the U.S., non-OPEC oil supply was revised only slightly lower (-0.1% or 60 mb/d) #OPEC #oilandgas

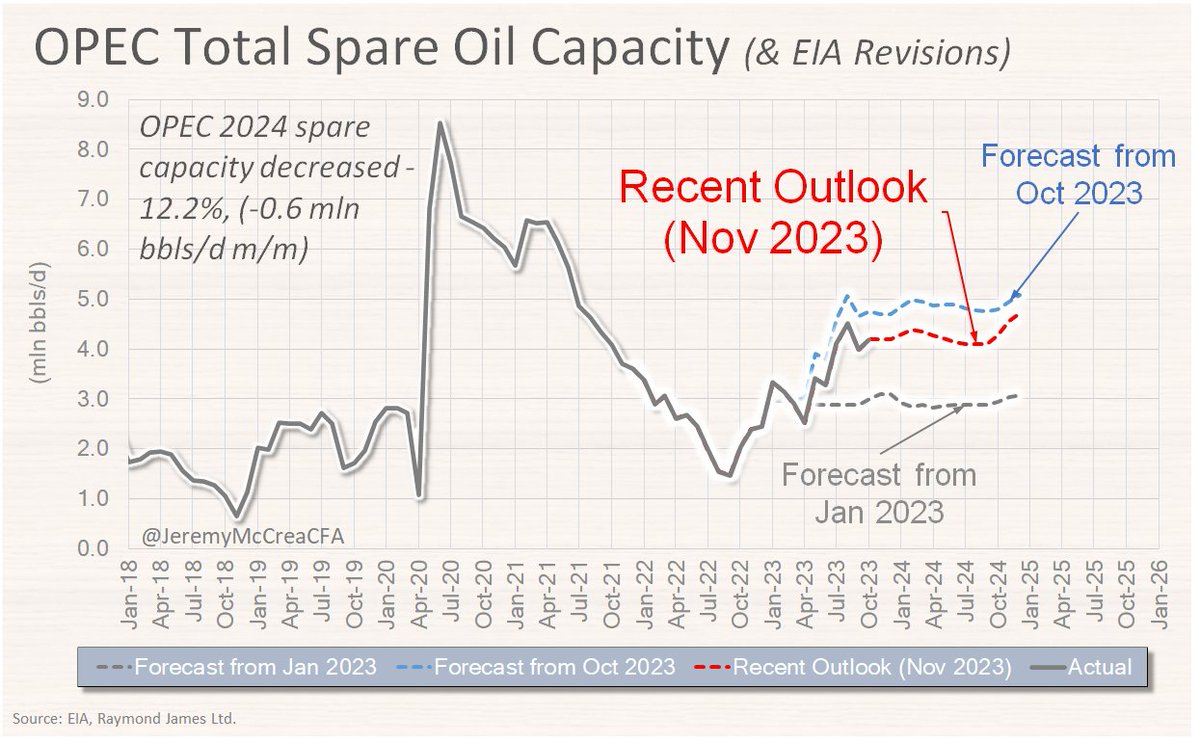

One of the larger global swing producers today is Russia. Despite sanction efforts, the EIA revised up Russian crude oil production by 4% (400 mb/d) for 2024 #oott #opec #opecplus

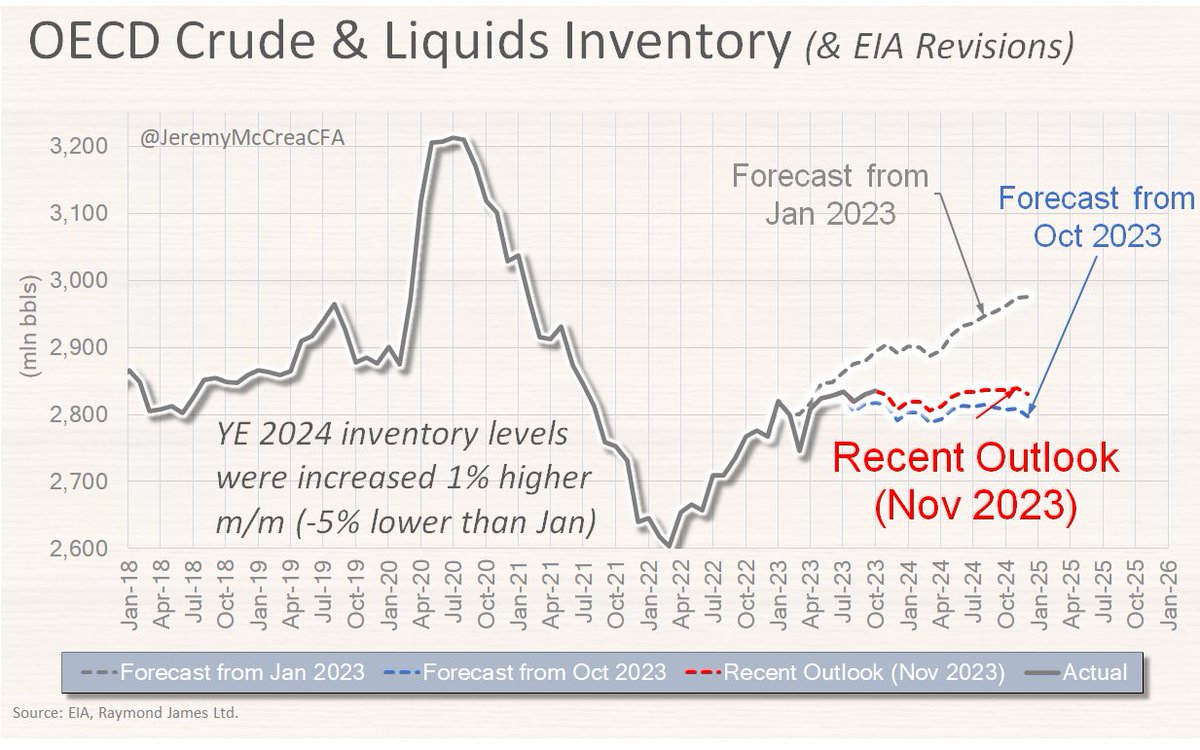

Ultimately, crude oil supply/demand factors coalesce into inventory levels and although the EIA lowered its YE 2024 levels by only 0.8%, it does show the directional bias in their forecast models today. #WTI #oilprice

• • •

Missing some Tweet in this thread? You can try to

force a refresh