OK let's talk $UBNT

Discussion on the company has been dominated by the fraud/shenanigans crowd since the @CitronResearch hit piece

I want do change that so let's do a deep dive on the fundamentals of the company with the wild assumption that the company is completely legit

Discussion on the company has been dominated by the fraud/shenanigans crowd since the @CitronResearch hit piece

I want do change that so let's do a deep dive on the fundamentals of the company with the wild assumption that the company is completely legit

short history:

@RobertPera has founded the company as a side project while working at Apple. he officially left and started Ubiquiti in 2005.

Pera had an idea for an outdoor wireless WiFi product and successfully launched it later that year for a great success

@RobertPera has founded the company as a side project while working at Apple. he officially left and started Ubiquiti in 2005.

Pera had an idea for an outdoor wireless WiFi product and successfully launched it later that year for a great success

The company was completely bootstrapped, Pera didn't use any VC (That's why he holds +70% to this day).

Pera identified early that the commodity hardware business model wasn't sustainable and understood that he needed a more defensible business model

Pera identified early that the commodity hardware business model wasn't sustainable and understood that he needed a more defensible business model

in 2008 Ubiquiti launched the AirMax platform. AirMax is a proprietary protocol which solves a bunch of technical problems of the common 802.11 WiFi standard for long-distance outdoor environment.

AirMax was special because it created a moat - the customers(WISPs) were locked-in

AirMax was special because it created a moat - the customers(WISPs) were locked-in

AirMax let Ubiquity become an integrated hardware software company in the mold of Apple (We'll get to the financial implications later).

I'll let Pera himself explain the importance of AirMax:

I'll let Pera himself explain the importance of AirMax:

BTW the excerpt was taken from @RobertPera's blog. I can't recommend it enough. It shows the thinking behind one of Tech's best contemporary minds. Even if Ubiquiti doesn't interest you per se, reading the blog will still give you incredible value.

rjpblog.com/page/2/

rjpblog.com/page/2/

anyway, AirMax was launched to a great success($50M sales in 2008) and effectively created a new industry: The WISP industry(WISP = Wireless Internet Service provider)

What are WISPs and how did Ubiquiti enable them?

What are WISPs and how did Ubiquiti enable them?

1. WISPs are usually operated by regional entrepreneurs and provide BB Internet to under-served markets.

2. Ubiquiti priced its products so cheap that it immediately made the WISPs economically feasible.

By 2011 Ubiquiti totally dominated the market and showed explosive growth

2. Ubiquiti priced its products so cheap that it immediately made the WISPs economically feasible.

By 2011 Ubiquiti totally dominated the market and showed explosive growth

By then, the business model was defined and relied on several principles:

1. Minimal spend on sales & support

2. Support is given in an Internet forum(the community) by the users themselves (and the actual engineers

3. Pricing the products insanely cheap

1. Minimal spend on sales & support

2. Support is given in an Internet forum(the community) by the users themselves (and the actual engineers

3. Pricing the products insanely cheap

the prices were so cheap that @RobertPera was accused of "leaving money on the table.

In reality though, Pera wasn't leaving any money. The value offering of the products was so incredibly high, that customers have become evangelists of the company.

In reality though, Pera wasn't leaving any money. The value offering of the products was so incredibly high, that customers have become evangelists of the company.

The customers were so in love with the product that they voluntarily became the marketing and support functions of the company.

so at that point, the company was basically an R&D operation with a defensible platform and minimal residual OPEX.

I mean just look at the financials:

so at that point, the company was basically an R&D operation with a defensible platform and minimal residual OPEX.

I mean just look at the financials:

Don't know about you, but I have never seen anything like it. an explosively growing tech platform (60% revenue CAGR from 2008 to 2012) with ~zero spend on SG&A(seriously, 2.5%), 35% EBIT margin and 100% conversion of Net Income to FCF

Can't stress it enough - That's one of the best financial performances I've ever seen from a nascent growing tech company. the only comparable I can think of is early iPhone/late Jobs era Apple(which kind of makes sense if you really think about it). Here, look at $APPL numbers:

By that point the company IPOed and Pera realized he can apply the same business model to new industries. he sought industries with specific characteristics:

1. Slow inflexible incumbents

2. Overpriced products

3. Sophisticated end consumers

1. Slow inflexible incumbents

2. Overpriced products

3. Sophisticated end consumers

the combination of all 3 enables the Ubiquiti business model because it can then:

1. introduce products with disruptive prices

2. be confident that the consumers will find the products without marketing and manage with no support

3. operate under the radar of the incumbents

1. introduce products with disruptive prices

2. be confident that the consumers will find the products without marketing and manage with no support

3. operate under the radar of the incumbents

In addition it was important that the product will be part of a defensible platform (like iOS and AirMax) and will be in an adjacent market(R&D wise).

The chosen industry was Enterprise networking and the platform was UniFi.

The chosen industry was Enterprise networking and the platform was UniFi.

Why Enterprise networking?

1. Inflexible incumbent (Cisco)

2. Overpriced products (hold that thought)

3. Sophisticated consumers (nerd IT types)

1. Inflexible incumbent (Cisco)

2. Overpriced products (hold that thought)

3. Sophisticated consumers (nerd IT types)

The prevalent business model in the industry consists of selling overpowered products at high initial prices with additional recurring subscription costs.

Ubiquiti launched competing products really disruptive pricing points. we're talking 80%-90% cheaper than the alternatives

Ubiquiti launched competing products really disruptive pricing points. we're talking 80%-90% cheaper than the alternatives

How did Ubiquiti managed to price so cheap?

1. selling more basic hardware with less features

2. spending ~0 on marketing and support.

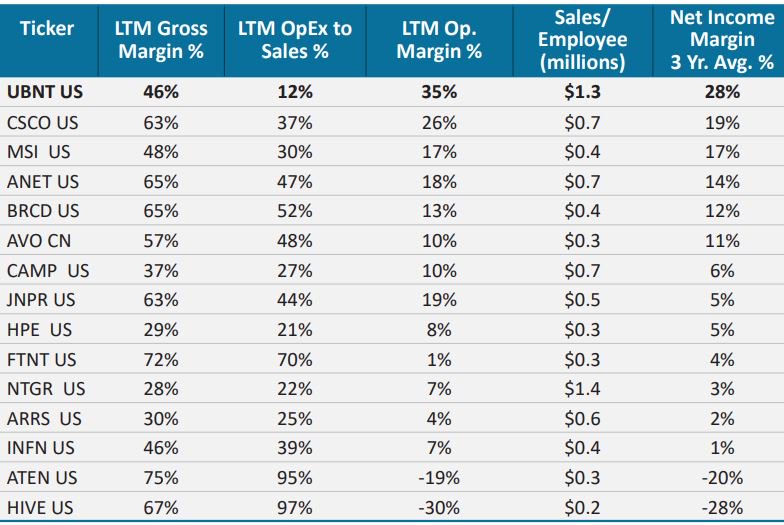

the business model is reflected in the numbers.

While gross margin is among the lowest of the industry, it possesses best of breed EBIT margins

1. selling more basic hardware with less features

2. spending ~0 on marketing and support.

the business model is reflected in the numbers.

While gross margin is among the lowest of the industry, it possesses best of breed EBIT margins

In the years since UniFi exploded and became the undisputed leader of another formerly under-served niche - SMBs networking.

Those are businesses who can't afford the stuff from the incumbents and had to use inferior consumer grade hardware prior to the appearance of UniFi

Those are businesses who can't afford the stuff from the incumbents and had to use inferior consumer grade hardware prior to the appearance of UniFi

We're talking about Hospitality, education, local governemnt, emerging markets, moms and pops retail, festivals, etc.

I recommend taking a look at the stories section on the website if you want to understand the customers better:

community.ubnt.com/t5/UniFi-Stori…

I recommend taking a look at the stories section on the website if you want to understand the customers better:

community.ubnt.com/t5/UniFi-Stori…

UniFi started mainly with access points, but spread quickly and now offers a full range of networking products (from cameras to switches).

The products are steadily improving and the company is in a direct collision course with Cisco

The products are steadily improving and the company is in a direct collision course with Cisco

competition can't react:

1. Price is so disruptive that incumbents can't compete. competing on price will decimate their business. There were attempts to offer inferior limited products but they're DOA

2. Challengers can't compete because they lack scale, brand & active community

1. Price is so disruptive that incumbents can't compete. competing on price will decimate their business. There were attempts to offer inferior limited products but they're DOA

2. Challengers can't compete because they lack scale, brand & active community

In addition, UniFi is a single management platform which means switching costs and a platform for add-on products.

for a more through introduction to UniFi I recommend the following:

arstechnica.com/information-te…

for a more through introduction to UniFi I recommend the following:

arstechnica.com/information-te…

It all adds up to UniFi dominating and presenting an even crazier growth rates than AirMax. UniFi revenue has gone from $35M in 2013 to $570M in 2018, a 75% CAGR and still growing at a 40% rate in 2018.

In the meantime Ubiquiti has become the incumbent in the WISP industry, and started to loss focus because of UniFi represents a much larger opportunity. Growth in the WISP segment has plateaued since 2014

Last points before I get to valuation:

1. The unique business model enables Ubiquiti to grow with minuscule growth capex. in Ubiquiti's case, growth capex is hidden inside the R&D line. ROIC is mind-boggling

1. The unique business model enables Ubiquiti to grow with minuscule growth capex. in Ubiquiti's case, growth capex is hidden inside the R&D line. ROIC is mind-boggling

2. That enables the business to spit cash while growing. couple that with a GOAT level capital allocator founder/operator and you get the following data which is one of the most extraordinary things I've witnessed in my investing career:

3. Ubiquiti has tried to enter new business lines but didn't found meaningful success besides UniFi. the beauty is that the the cost of failure is negligible so the investor gets optionality for new product lines with minimal risk

Valuation:

I'm assuming 21% normalized tax rate which leads to 27% net margin on 2018.

best way to value is sum of parts because of the different outlook of the two segments and their relative independence from each other.

we'll assume the two segments operate at the same margin.

I'm assuming 21% normalized tax rate which leads to 27% net margin on 2018.

best way to value is sum of parts because of the different outlook of the two segments and their relative independence from each other.

we'll assume the two segments operate at the same margin.

Sum of parts:

1. WISP: $121M 2018 earnings. 0 growth, probably worth 10x-12x which equals $1.3B

2. net cash: $180M

3. UniFi: $154M 2018 earnings. 40% growth and converting 100% of NI to FCF and buying back stock. market values at 38x - $7.4B

4. option value - market values at 0

1. WISP: $121M 2018 earnings. 0 growth, probably worth 10x-12x which equals $1.3B

2. net cash: $180M

3. UniFi: $154M 2018 earnings. 40% growth and converting 100% of NI to FCF and buying back stock. market values at 38x - $7.4B

4. option value - market values at 0

if you assume 20% growth for UniFi it trades at about 30x 2019 earnings.

So, is 30x appropriate for UniFi?

It's arguable but comparison to parallel rapid growing tech platforms(we'll use $NTNX as example) reveals an interesting situation

So, is 30x appropriate for UniFi?

It's arguable but comparison to parallel rapid growing tech platforms(we'll use $NTNX as example) reveals an interesting situation

Ubiquiti is unique in that it actively returns cash to shareholders while growing so fast. if we apply an arbitrary 20% net margin to NTNX, we'll get that it trades at about 30x which on the surface is on par with UBNT

the key difference though is that NTNX is currently not really generating 20% margins and actually is investing a lot of money in order to grow and rapidly diluting shareholders in the meantime.

so while NTNX might be a great business, a $ in earnings for NTNX is worth much less than a comparable $ for UBNT(all else equal). the same holds for UBNT when comparing with the vast majority of rapid tech growers

What is FV? I'm not sure. For now I'm just happy holding a great company at a reasonable price.

Barring a serious SEC outcome I'm pretty confident the stock will yield satisfactory returns for the long term shareholder even at current share price.

Barring a serious SEC outcome I'm pretty confident the stock will yield satisfactory returns for the long term shareholder even at current share price.