,

10 tweets,

4 min read

Read on Twitter

I've heard people say they can't be a victim of internet fraud because they don't subscribe to internet banking or do any epayment. What if I tell you that two recent cases of e-fraud I know of, involve people who are not into ebanking or other fancy payment modules like USSD?

That you've not gone "e" is no longer a protection. In fact, scammers are on the look out for these kind of people. The methodology is simple. They steal your phone, they enroll it for USSD and they steal your money.

I don't know if this is a banking industry problem or just a one bank problem. But the bank that keeps popping up anytime this kind of fraud occurs is @gtbank. Against regulatory prescriptions that limits daily withdraws & 2FA, GTB seems to make it easy for fraudsters to steal.

It's important we say these things because as at today, if you own a GTB a/c, you're at risk of being defrauded whether or not you use USSD, own an ATM Card or use internet banking. GTB has to do better to protect its customers from fraudsters. Convenience must not trump security

So how do you protect yourself?

1. Don't lose your phone

2. Don't lose your phone

3. Don't lose your phone

There are other things u can do but they're linked to protection from phone loss. This's why we ask the @cenbank to be tougher on banks who are in default of its guidelines

1. Don't lose your phone

2. Don't lose your phone

3. Don't lose your phone

There are other things u can do but they're linked to protection from phone loss. This's why we ask the @cenbank to be tougher on banks who are in default of its guidelines

If you've been a victim of this kind of fraud, speak out. The law is on your side. The bank will say it was your fault. But you must maintain that it is rather the fault of the bank that they allowed money in their legal custody to be stolen. They must therefore refund every dime

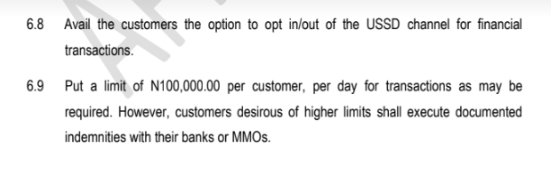

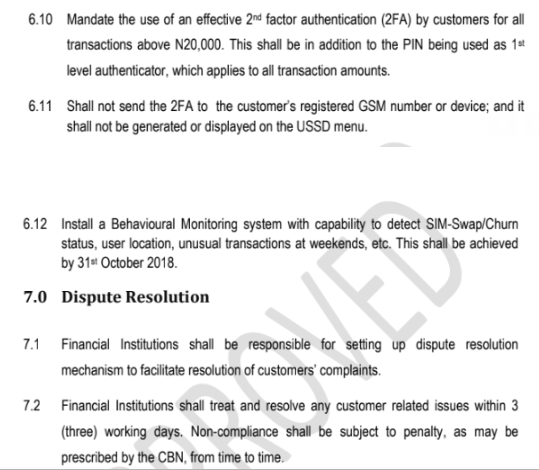

First, the banks are mandated to ensure a daily limit of N100k is maintained on USSD. If anything over that amt is withdrawn from your account, without a signed indemnity, the bank is in default. 2ndly, If any payment above N20k is effected without a 2FA, the bank is in default.

Thirdly, Section 7.2 of the USSD Guideline clearly states that “Customer related issues should be resolved within three (3) working days". If you make a formal complaint to the bank and if it is yet to be resolved after 3 working days, the bank is in default and they must refund.

Who do you write?

1. The bank MD. Corporate clients understand this. All letters are addressed to the MD. Once it's acknowledged at a branch, the MD can't claim he didn't see it

2. Send email copies of acknowledge letter to d compliant dept, CBN, CPC

*Wait 3 days & send reminder

1. The bank MD. Corporate clients understand this. All letters are addressed to the MD. Once it's acknowledged at a branch, the MD can't claim he didn't see it

2. Send email copies of acknowledge letter to d compliant dept, CBN, CPC

*Wait 3 days & send reminder

If you've never been a victim of fraud you'll not understand how it feels to watch your savings fly away one debit alert at a time. So please share this thread and this one by @WaleMicaiah as well. While we wait for CBN to do the needful, let's stay Woke.