,

9 tweets,

4 min read

Read on Twitter

ECB: Breakeven Bad.

A thread on inflation expectations, or lack thereof. (1/n)

A thread on inflation expectations, or lack thereof. (1/n)

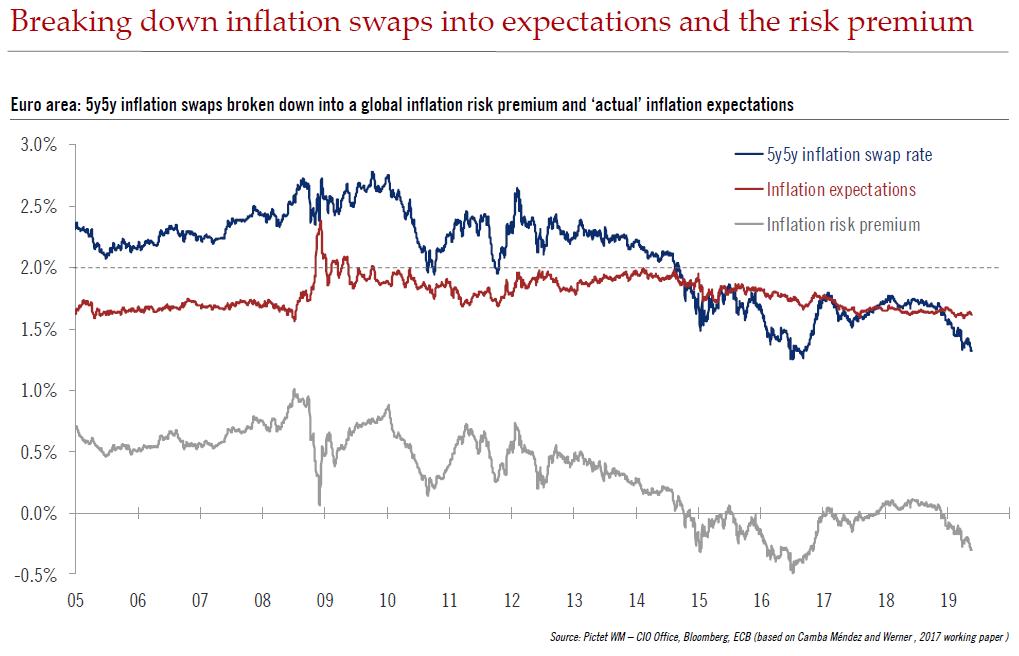

Inflation expectations are more important than ever to the ECB outlook. Ever since Mario Draghi mentioned the 5y5y inflation swap in Jackson Hole in 2014, it has become a symbol of the ECB's successes and failures. Today it's less than 10bp away from its all-time low. (2/n)

The problem is, inflation swaps are far from a reliable measure of inflation expectations, being driven by global factors and risk sentiment. Empirical evidence suggests that the inflation risk premium is negative, i.e. inflation breakeven should be higher all else equal. (3/n)

In order to extract the inflation risk premium and inflation expectation components from inflation-linked swaps (ILS), we have reproduced the model from Camba Méndez & Werner (2017) mentioned by Benoît Coeuré (there’s always a speech: ecb.europa.eu/press/key/date…). (4/n)

We find that the bulk of the decline in 5y5y inflation swaps since their peak in 2018 has been driven by developments in the global risk premium, with a limited, albeit rising, contribution from ‘actual’ inflation expectations this year. (5/n)

Specifically, no more than 15% of the drop in 5y5y inflation swaps over the past year can be attributed to lower inflation expectations, but this contribution has risen to over 30% this year, which requires careful monitoring. (6/n)

Survey-based metrics, while more resilient, also point to some shift in the distribution of inflation expectations. We find that the sensitivity of SPF expectations to actual inflation releases has started to increase again recently, in line with Coeuré's remarks. (7/n)

A couple of caveats: 1) oil prices should have helped but they haven't, which may explain part of the US-EA gap; 2) it's a global phenomenon, with inflation expectations falling in the US, too. (8/n)

Any sign of further dis-anchoring of inflation expectations would force an ECB response. We're not there yet, but we know what it would mean in terms of the ECB’s reaction function. QE, whatever the political, legal and technical costs.

My old bubble chart updated! (9/9)

My old bubble chart updated! (9/9)