,

18 tweets,

4 min read

Read on Twitter

It isn't fashionable to say things like this about smart guys like Dr. Mike Burry, but this is a steaming hot take.

bloomberg.com/news/articles/…

bloomberg.com/news/articles/…

The "recent flood of money into index funds" has not been so recent. It has been 20+yrs. And before that, futures were a thing. And before that, broad open-ended mutual funds were a thing, going back 95yrs now.

And broad-based stock bubbles and crashes are not new either.

And broad-based stock bubbles and crashes are not new either.

As to... 'The flows will reverse at some point, he said, and “it will be ugly” when they do', I assume he means some day stocks or ETFs will get sold at prices lower than the previous day.

Yes, markets go down. And every sale print needs a buyer.

So the argument is different.

Yes, markets go down. And every sale print needs a buyer.

So the argument is different.

On "price discovery", yes. He has a point. Buying an S&P500 or Russell 2000 ETF doesn't pick the stocks, but historically, most people didn't pick stocks. Stocks were picked for them. They bought what their broker, their uncle, Barrons, or the guy at the Sunday BBQ recommended.

The crux of his point about damage appears to be "liquidity."

“The dirty secret of passive index funds -whether open-end, closed-end, or ETF - is the distribution of daily dollar value traded among the securities within the indexes they mimic."

Not a dirty secret, nor abnormal.

“The dirty secret of passive index funds -whether open-end, closed-end, or ETF - is the distribution of daily dollar value traded among the securities within the indexes they mimic."

Not a dirty secret, nor abnormal.

Stocks have varying degrees of liquidity. This is not new. He talks about dollar liquidity, which is meaningless in and of itself. He should talk about liquidity against float.

Half the S&P trades less than US$150mm/day?

Sure. That half is worth 13% of S&P500 float mktcap.

Half the S&P trades less than US$150mm/day?

Sure. That half is worth 13% of S&P500 float mktcap.

That is the nature of long tails. There aren't 500 AAPLs or AMZNs to go around. If there were, they wouldn't be Apples or Amazons.

So the other half trades more. On average $490mm/day. Take out the top 20 and the average of the remaining 230 of the top 250 is $350mm/day.

So the other half trades more. On average $490mm/day. Take out the top 20 and the average of the remaining 230 of the top 250 is $350mm/day.

But liquidity is about float changing hands, not HFTs scalping retail on the top 20.

The "illiquid" bottom 250 names? They trade on average 30% more ADV/float than the 230 (Top 250 less Top 20), and 15% more than the top 250 (19% if you exclude AMD).

The bottom 250 are liquid.

The "illiquid" bottom 250 names? They trade on average 30% more ADV/float than the 230 (Top 250 less Top 20), and 15% more than the top 250 (19% if you exclude AMD).

The bottom 250 are liquid.

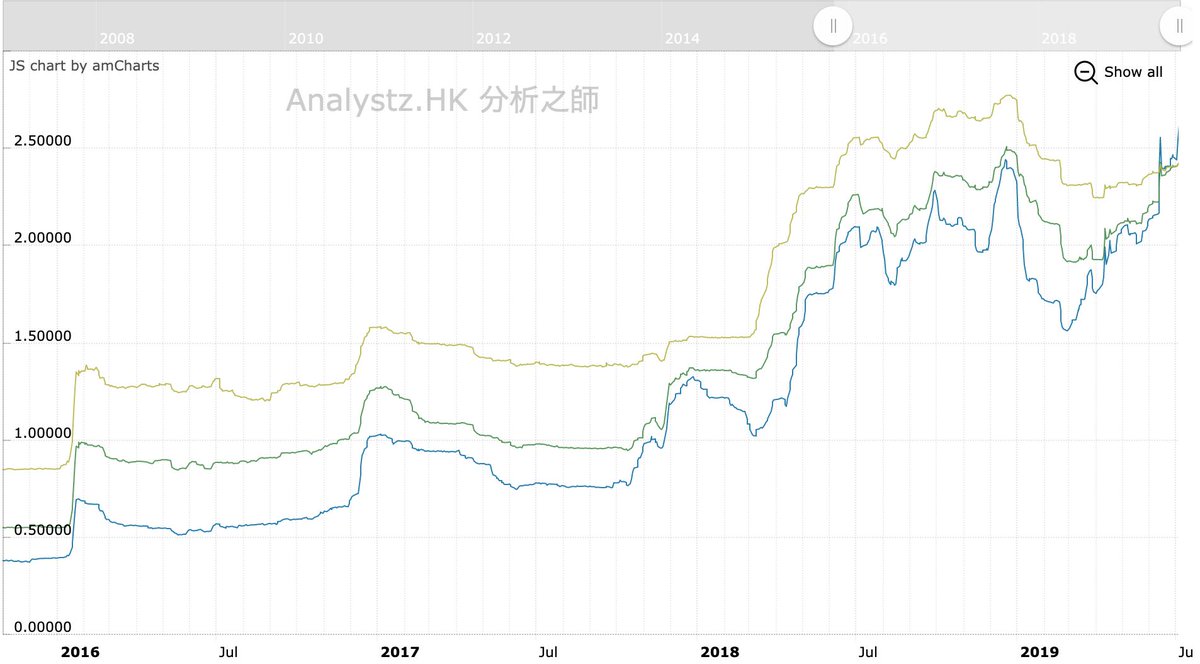

How about IWM?

Separating the 2000 names into 5 quintiles shows the averages are pretty evenly spread by size, but it is to note that the R2k is itself the market's long tail. S&P has its top20, its top 250 (87% of float), the next 250, then there is a gap and then the R2k.

Separating the 2000 names into 5 quintiles shows the averages are pretty evenly spread by size, but it is to note that the R2k is itself the market's long tail. S&P has its top20, its top 250 (87% of float), the next 250, then there is a gap and then the R2k.

The real crux is here: THE UNWIND.

The idea is that everything has to unwind. That is FALSE.

All the stocks in the market are owned by all the people in the market. Twas ever thus. Only the packaging is different.

The idea is that everything has to unwind. That is FALSE.

All the stocks in the market are owned by all the people in the market. Twas ever thus. Only the packaging is different.

The huge rise in passive investing has seen materially ALL of its inflow from the loss of AUM from other collective investment schemes (mutual funds). On average, pre-fees, I expect one would find that all the ETFs/passive perform roughly the same way the mutual funds did.

1929 peak to trough a few years later saw DJIA fall 89%. A lack of ETFs or much less prevalence did not keep Berkshire Hathaway from losing 50% a couple of times. The S&P500 fell by half in 1973-74. And again by half in 2000-2002. And 57% in 2007-2009.

The key is...

Only People Who Have To Unwind Have To Unwind.

Most of the large previous crashes were the result of excessive leverage forcing unwind. Of course, some is mechanical and some is behavioral. I could be "overinvested" in equities and that would make me 'levered'

Only People Who Have To Unwind Have To Unwind.

Most of the large previous crashes were the result of excessive leverage forcing unwind. Of course, some is mechanical and some is behavioral. I could be "overinvested" in equities and that would make me 'levered'

when vol goes up because the daily mark to market "hurts" mentally. I might 'force myself' to unwind - to 'sell until the sleeping point'.

The question therefore is...

Are passive investors "stretching" the market because they are saving too much because they have FOMO?

The question therefore is...

Are passive investors "stretching" the market because they are saving too much because they have FOMO?

Not clear.

Have they pushed things more than previous bubbles with huge FOMO/momentum of CISs? (1929, 1936, 1946, 1965, 1968, Dec72, Sep87?

Also not clear.

How far would the components of the ETFs have to fall? (we know the smallcaps have good value because Burry owns them).

Have they pushed things more than previous bubbles with huge FOMO/momentum of CISs? (1929, 1936, 1946, 1965, 1968, Dec72, Sep87?

Also not clear.

How far would the components of the ETFs have to fall? (we know the smallcaps have good value because Burry owns them).

Sounds suspiciously like a growth vs value reversion call.

His mention of small cap Japan value traps is a sign. I don't disagree. There's great value there with a governance tailwind. But "passive is a bubble" as an excuse for smallcap value being undervalued? Not a good look.

His mention of small cap Japan value traps is a sign. I don't disagree. There's great value there with a governance tailwind. But "passive is a bubble" as an excuse for smallcap value being undervalued? Not a good look.

Those smcap J-names have small floats/mktcap, and combined mkt cap is ~3-5% of Japan mktcap which is 10% of world.

A Small AUM High Active Share Go Anywhere Fund with a highly idiosyncratic mgr can do that.

A $20-30bn fund cannot. So $25trln of S&P mktcap can’t either.

A Small AUM High Active Share Go Anywhere Fund with a highly idiosyncratic mgr can do that.

A $20-30bn fund cannot. So $25trln of S&P mktcap can’t either.

Oops. Meant 19% if you include AMD. AMD has a ridiculously high ADV as a percentage of its float. I’d say totally unsustainable. It’s the outlier on the right.