,

21 tweets,

7 min read

Read on Twitter

Dear Emma,

There are issues with your tweets here. A bunch of them in fact.

About HIBOR, the press, mortgages, defaults, the peg, and how it works.

There are issues with your tweets here. A bunch of them in fact.

About HIBOR, the press, mortgages, defaults, the peg, and how it works.

1) To those saying the local press in Hong Kong is not talking about the spike in HIBOR...

I urge you to google "HIBOR" news over the last 24hrs.

I assure you they are.

I urge you to google "HIBOR" news over the last 24hrs.

I assure you they are.

I'd ask... if the local press is not talking about it... how did you see it?

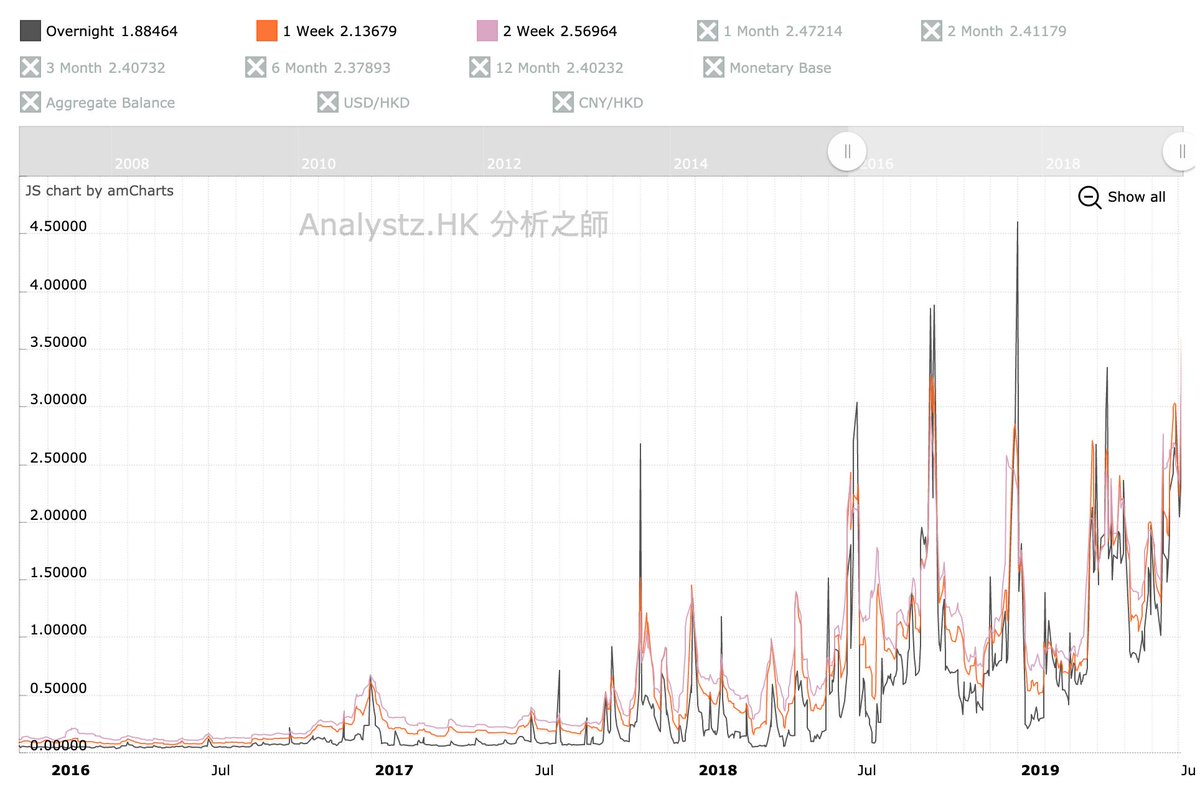

2) HIBOR, "which blew through 3%."

Which HIBOR?

12m and 6m HIBOR are not overly jumpy. 3m is a little jumpier.

2) HIBOR, "which blew through 3%."

Which HIBOR?

12m and 6m HIBOR are not overly jumpy. 3m is a little jumpier.

And O/N, 1wk, 2wk, 1mo, are a LOT jumpier.

But... if you look at the history, they have a record of being a lot jumpier. This is not the first time we have seen a very short-end HIBOR squeeze.

But... if you look at the history, they have a record of being a lot jumpier. This is not the first time we have seen a very short-end HIBOR squeeze.

Mortgages. There are two basic mortgage rates in HK.

1) 1MO HIBOR-PLUS-spread (90-95%)

2) BankPrimeRate-MINUS-spread (5-10%)

KEY DETAIL: almost all HK mortgages have a clause which says that if the rate you'd pay this month on #1 goes above the rate you'd pay on #2, you pay #2.

1) 1MO HIBOR-PLUS-spread (90-95%)

2) BankPrimeRate-MINUS-spread (5-10%)

KEY DETAIL: almost all HK mortgages have a clause which says that if the rate you'd pay this month on #1 goes above the rate you'd pay on #2, you pay #2.

So, only when the longer-term HIBOR rates rise and Bank Prime Rates rise do mortgages start to get a lot more expensive.

You use the word "Default": Do you have ANY data, articles, etc which suggest that default on mortgages in HK are, or will be "problematic"? Any at all?

You use the word "Default": Do you have ANY data, articles, etc which suggest that default on mortgages in HK are, or will be "problematic"? Any at all?

Why did short-term HIBOR (HK Interbank Offer Rate) jump? Because HK Banks are not OFFERING short-term money cheaply. They need it now. If you want money for 1mo, they can give it to you a lot cheaper. 1yr? Even cheaper. But it you want it only for 1-2 weeks, it will cost more.

In the table above 2W minus 1M = 48bp. That means the other 2.2 weeks after the first 2W are offered at 2.56% or so. Banks will offer you 2wk money at almost 90bp less if you wait 2wks.

And if 1mo is 2.98 and 2mo is 2.67, 1mo in 1mo is ~2.36. You can book that now.

And if 1mo is 2.98 and 2mo is 2.67, 1mo in 1mo is ~2.36. You can book that now.

So why is 1wk and 2wk HIBOR high?

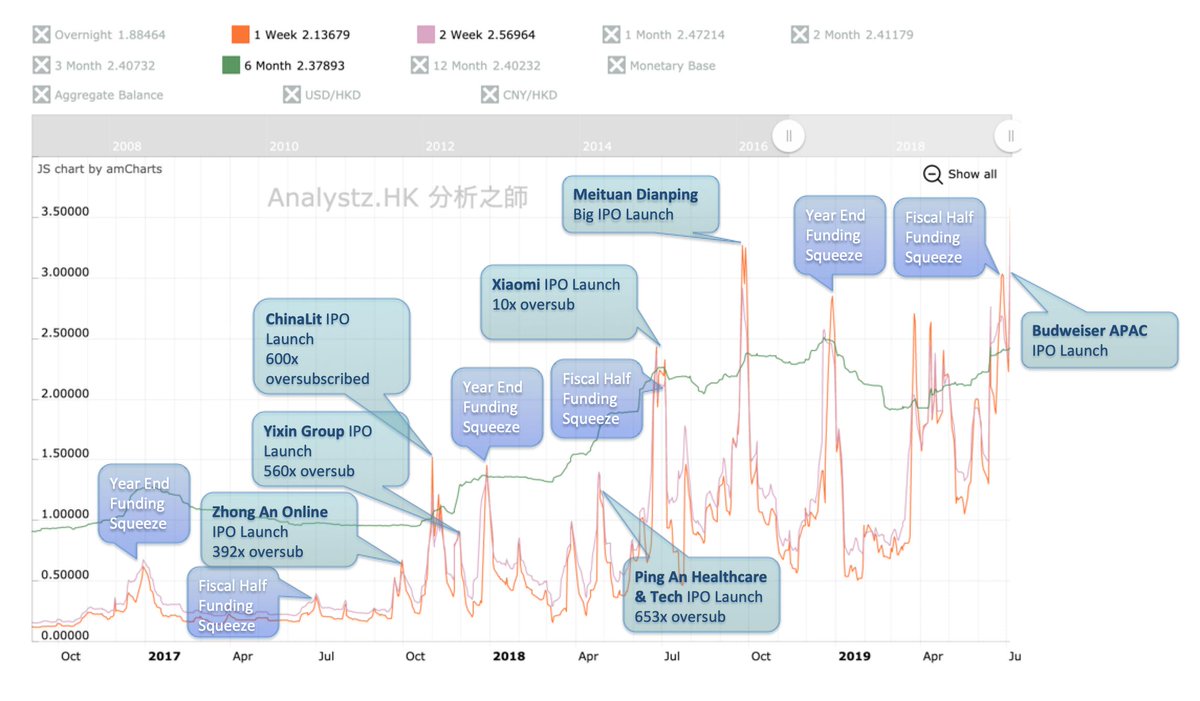

Because of the Budweiser APAC IPO. It's big at almost US$10bn.

I wrote about it yesterday in response to @Jkylebass' tweet.

It is NOT ABNORMAL AT ALL.

Because of the Budweiser APAC IPO. It's big at almost US$10bn.

I wrote about it yesterday in response to @Jkylebass' tweet.

It is NOT ABNORMAL AT ALL.

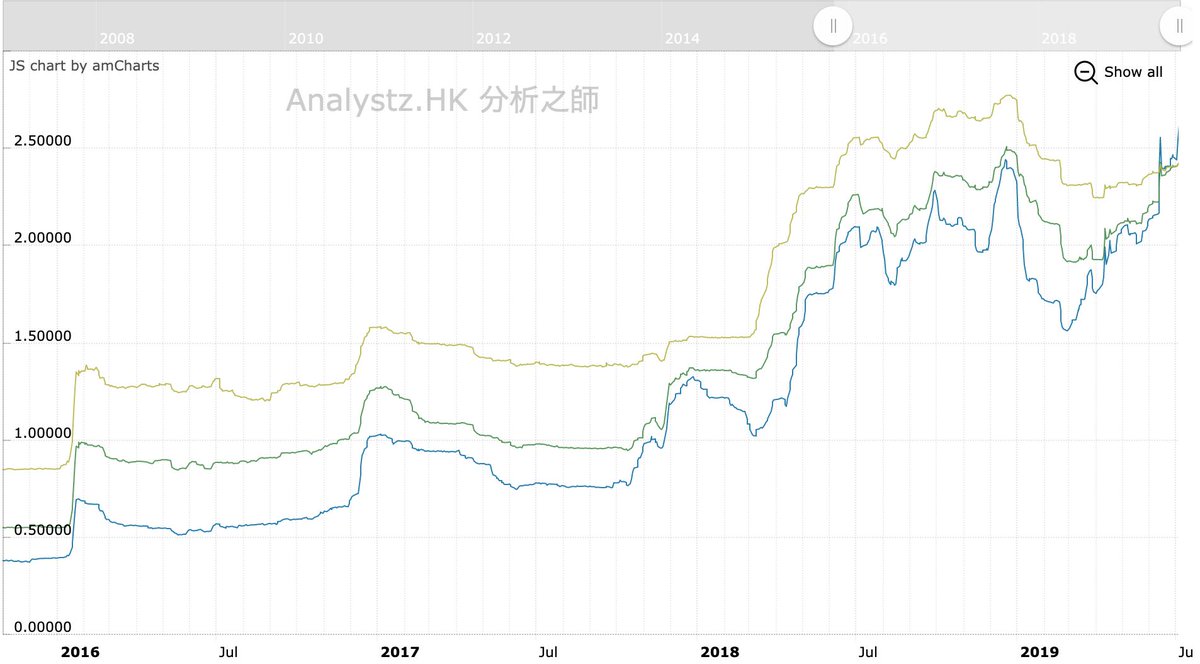

Hong Kong has a history of this.

The chart below will show you that spikes in 1W and 2W HIBOR happen with some regularity.

It happens every 6mos for funding over the photo, and it happens on IPOs with big retail subscriptions.

The chart below will show you that spikes in 1W and 2W HIBOR happen with some regularity.

It happens every 6mos for funding over the photo, and it happens on IPOs with big retail subscriptions.

The HKMA link above, gives a detailed explanation of the phenomenon. Otherwise, table below of IPOs

around late Oct-2017. Highlighted is ChinaLit - 1-2W HIBOR spiked from 0.2% to 1.6% then.

Highlighted line is key.

Deal anncd 10/24-ish

Orders in by 10/31

"Refund Date" 11/7

around late Oct-2017. Highlighted is ChinaLit - 1-2W HIBOR spiked from 0.2% to 1.6% then.

Highlighted line is key.

Deal anncd 10/24-ish

Orders in by 10/31

"Refund Date" 11/7

When retail investors put in, they have to put their money down. And it stays there for 6-9 days until "Refund Date". If a deal launches, you prep your money, and it disappears for 1-2wks.

China Lit saw HK$ 520 BILLION come out of the short-term funding market for a week.

China Lit saw HK$ 520 BILLION come out of the short-term funding market for a week.

Why so much? Retail gets 10% of an IPO. Unless it is oversubbed, in which case it can get to 50% through the "clawback mechanism."

Brokers want IPOs to be hot, so they will lend you money so you can buy more. Sometimes 90% margin. You put up $10k. Broker puts up $90k.

Brokers want IPOs to be hot, so they will lend you money so you can buy more. Sometimes 90% margin. You put up $10k. Broker puts up $90k.

You want to guarantee access to margin funding? Go in early. Borrow $90k for 2wks.

If you get 1/100 of your order, you buy $1k. You paid 3% on $90k for 2wks which is $104.

If you only get $1k, your breakeven is +11.8% (comms, fees, interest). So it's a bet.

If you get 1/100 of your order, you buy $1k. You paid 3% on $90k for 2wks which is $104.

If you only get $1k, your breakeven is +11.8% (comms, fees, interest). So it's a bet.

This one is also an issue.

No clue about the 90%. I'll ignore for now. Unrelated to peg discussion.

HIBOR 1M occasionally diverges from LIBOR 1M. Flush liquidity in retail accounts does not auto-switch immediately.

Also...

No clue about the 90%. I'll ignore for now. Unrelated to peg discussion.

HIBOR 1M occasionally diverges from LIBOR 1M. Flush liquidity in retail accounts does not auto-switch immediately.

Also...

Peg mechanics have a delay function. The system functions because HKMA intervenes at the peg boundaries, not between. The system takes care of itself between. Volatile very short-term rates and stable short-term rates and stronger HKD are N-O-T a symptom of capital flight.

They are a symptom of a funding squeeze.

And it has happened MANY times before and will happen MANY times again and local press and local market professionals are utterly aware and utterly prepared.

Want to try to arb that 110bp rate spread btwn 1wk HIBOR and 1wk US$LIBOR?

And it has happened MANY times before and will happen MANY times again and local press and local market professionals are utterly aware and utterly prepared.

Want to try to arb that 110bp rate spread btwn 1wk HIBOR and 1wk US$LIBOR?

There's 0.021154% in it for you IF you assume the pros are blind on the 1wk USDHKD forward AND assuming you can hedge your FX at less than 1.1bp friction each way.

The thing about the peg is that the HKMA contracts the monetary base denominated in HKD at 7.85. That does not necessarily contract the HK-based monetary base, just the HKD portion.

And when it comes off 7.85, they are out of the market, so HIBOR can do what it wants.

And when it comes off 7.85, they are out of the market, so HIBOR can do what it wants.

And if banks - who literally are the money printers in Hong Kong - can't convince their depositors to switch to USD, they end up overly long HIBOR at the very front of the curve, which is why the shape of the front end of the curve of HKD is different than USD.