A tremendous amount of ink has been spilled discussing the supposed quandary of the #equity market’s robust recovery since March, while at the same time #economic improvement has been more uneven and uncertain.

At the heart of this misunderstanding is an apples-to-oranges comparison: the fact is that the #stock #market and the #economy, while connected, are two meaningfully distinct entities.

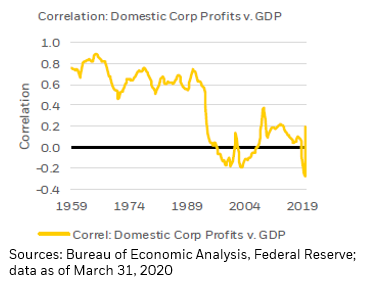

As a case in point, the correlation between domestic corporate #profits and #GDP #growth collapsed in the 1990s and has hovered near zero for the past three decades.

Furthermore, in today’s environment, the industries that have been most adversely affected by the #pandemic lockdowns (hotels, restaurants, leisure, airlines) hold an outsized impact on #labor markets, but a relatively minimal influence over #financial #markets.

And at the same time those firms that hold the greatest weights in major #market indices also tend to #employ relatively fewer people than did the top #firms several decades ago.

None of that is to ignore the genuine #economic pain being felt by many #SmallBusinesses, which are truly struggling through this period with massive #revenue and #employment losses, but those firms are not the same as those in the major #equity indices.

Finally, many commentators dramatically underestimate the impact of #monetary and #fiscal support, which is a theme we have long argued is of prime importance for #markets today.

• • •

Missing some Tweet in this thread? You can try to

force a refresh