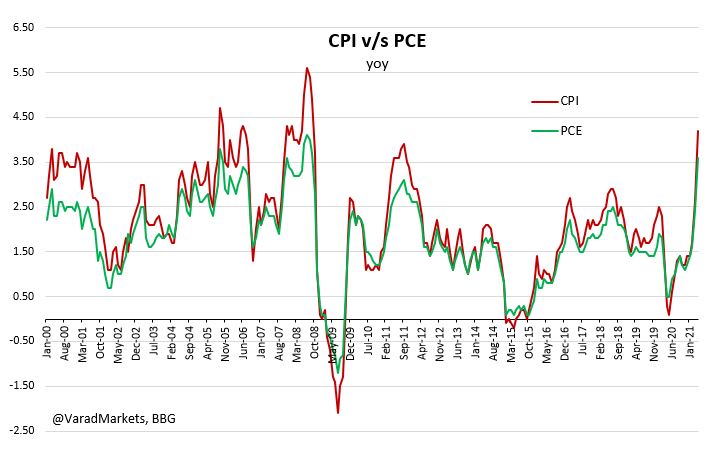

Role of #USD & #EUR in Global Monetary System:

[Charts from ECB Paper: 'International Role of Euro']

#Dollar continues to dominate FX Reserves, International Debt, Loans, Deposits, FX Turnover & Global payments

1/7

[Charts from ECB Paper: 'International Role of Euro']

#Dollar continues to dominate FX Reserves, International Debt, Loans, Deposits, FX Turnover & Global payments

1/7

FX Transactions settled in CLS System (Continuous Linked Settlement)

▪️ USD led FX market => involved in ~90% of all settlements in Dec'20

▪️ EUR second most actively settled ccy

2/7

▪️ USD led FX market => involved in ~90% of all settlements in Dec'20

▪️ EUR second most actively settled ccy

2/7

FX Share in Global FX RESERVES:

Sub-thread below

3/7

Sub-thread below

3/7

https://twitter.com/VaradMarkets/status/1377336275653459972?s=20

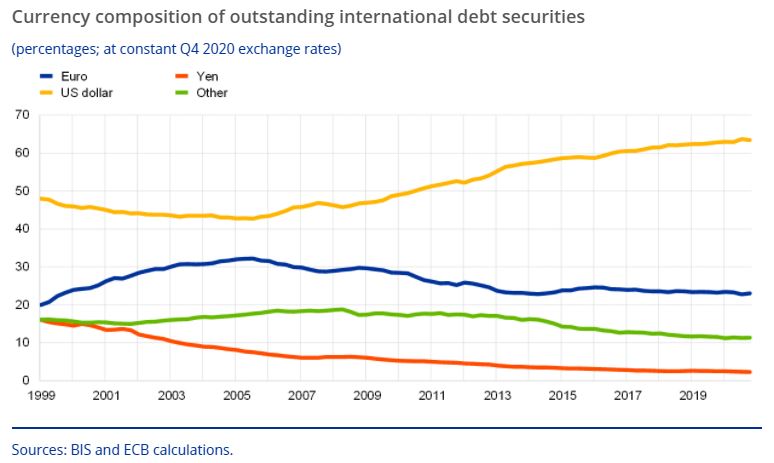

FX Share in International DEBT:

▪️ USD accounts for ~66% of all International Debt issuance

▪️ EUR share has declined to 23%

4/7

▪️ USD accounts for ~66% of all International Debt issuance

▪️ EUR share has declined to 23%

4/7

Borrowers of International Debt:

▪️ USD-denominated debt issuance by EM borrowers surged - favourable financing conditions in US

▪️ EUR-denominated debt issuance declined - less interest from US borrowers

▪️ Also rapid growth in USD-denominated green bond issuance in 2020

5/7

▪️ USD-denominated debt issuance by EM borrowers surged - favourable financing conditions in US

▪️ EUR-denominated debt issuance declined - less interest from US borrowers

▪️ Also rapid growth in USD-denominated green bond issuance in 2020

5/7

FX Share in International LOANS:

▪️ USD share declined but still dominant ccy => 54% of international loans

▪️ EUR 16%, Others 27%

6/7

▪️ USD share declined but still dominant ccy => 54% of international loans

▪️ EUR 16%, Others 27%

6/7

FX Share in International DEPOSITS:

▪️ USD share of outstanding stock of international deposits ~54% => pandemic driven safe-haven Dollar demand + Fed's QE driven excess USD liquidity

▪️ EUR share 17%

@rodneyatwigram @chigrl

Reference:

ecb.europa.eu/pub/ire/html/e…

7/7

▪️ USD share of outstanding stock of international deposits ~54% => pandemic driven safe-haven Dollar demand + Fed's QE driven excess USD liquidity

▪️ EUR share 17%

@rodneyatwigram @chigrl

Reference:

ecb.europa.eu/pub/ire/html/e…

7/7

• • •

Missing some Tweet in this thread? You can try to

force a refresh