These are the EIA's key forecast revisions impacting natural gas markets. Although many of the adjustments are small, it shows the directional bias within their models. Overall, negative revisions for production; upward revisions in consumption for 2024, as NYMEX prices come down

LNG volumes are taking longer to pick-up in early 2023 but ultimately are still expected to grow to 13.5 bcf/d by YE 2024 #LNG #Natgas

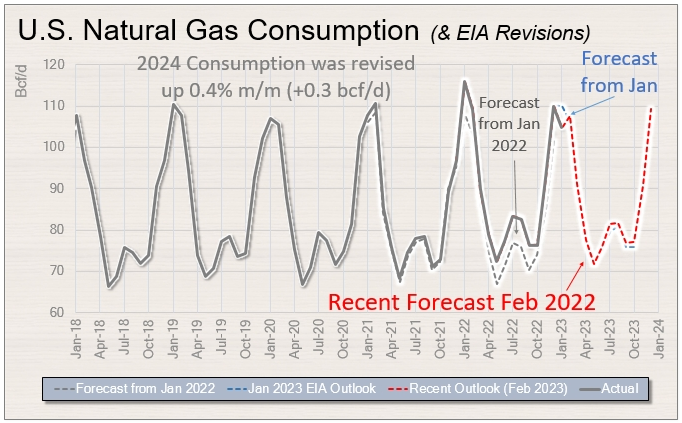

Natural gas consumption doesn't quite reach levels seen last year (in both winter and summer months). This is typically the result of weather; with current demand being revised down slightly from last month

Expectations for trough 2023 storage levels have been revised up by 5% on the back of warmer weather. Despite constructive supply/demand forces for 2024, storage level expectations in this year have also still moved higher #naturalgas

One of the larger revisions the EIA made was to its NYMEX natural gas price forecast - dropping its forecast from ~$5/mcf to ~$3.50/mcf in 2023. It's price outlook slowly builds throughout 2024 as supply/demand forces come into balance

• • •

Missing some Tweet in this thread? You can try to

force a refresh