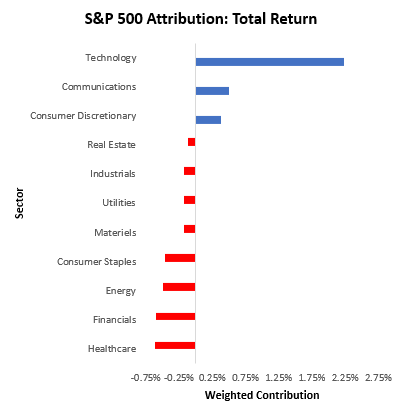

Market Regime Update

1. Over the last week, assets rallied in unison. Below, we show stocks, commodities, and bonds were up while the dollar sold off.

1. Over the last week, assets rallied in unison. Below, we show stocks, commodities, and bonds were up while the dollar sold off.

2. The strength of the moves in commodities has filtered through to the one-month pricing of rising growth outcomes. We show our market regime measures below.

3. While near-term pricing has been of rising growth, the distribution of regime probabilities remains flat, as highlighted above. Our non-linear trend process has worked well in navigating these conflicting market regime dynamics.

4. The weekly signal output from this process are shared below.

https://twitter.com/prometheusmacro/status/1668050543959322624

5. The shift in trend signal for Treasuries is particularly important, especially given that the market continues to price interest rate cuts. These look unlikely to materialize.

6. For further context, we recommend all our followers to read our latest edition of the Month in Macro ~ 45 pages of the best #macro content out there.

prometheus-research.net/p/month-in-mac…

prometheus-research.net/p/month-in-mac…

• • •

Missing some Tweet in this thread? You can try to

force a refresh