1/ I’ve received a number of questions lately about replacing liquid alternatives with tactical strategies.

I wanted to write a quick tweetstorm contrasting the two.

(Full disclosure: I manage tactical portfolios.)

I wanted to write a quick tweetstorm contrasting the two.

(Full disclosure: I manage tactical portfolios.)

2/ Painting in broad strokes, tactical strategies believe that expected premiums earned from exposure to systematic risk factors are time-varying and, therefore, portfolio composition should be as well.

3/ It is important to point out that these are typically the same risk factors already held within most strategic portfolios.

4/ Tactical decisions are traditionally derived from economic, fundamental/valuation, technical, and sentiment-based signals.

I, personally, lean heavily towards signals derived from the pantheon of quantitative style premia: value, momentum, carry, defensive, and trend.

I, personally, lean heavily towards signals derived from the pantheon of quantitative style premia: value, momentum, carry, defensive, and trend.

5/ Where tactical asset allocation rotates and tilts exposure to systematic factors, alternatives engineer *entirely new ones*.

This is typically achieved by going long one set of investments and short another, often eliminating a significant proportion of systematic risk.

This is typically achieved by going long one set of investments and short another, often eliminating a significant proportion of systematic risk.

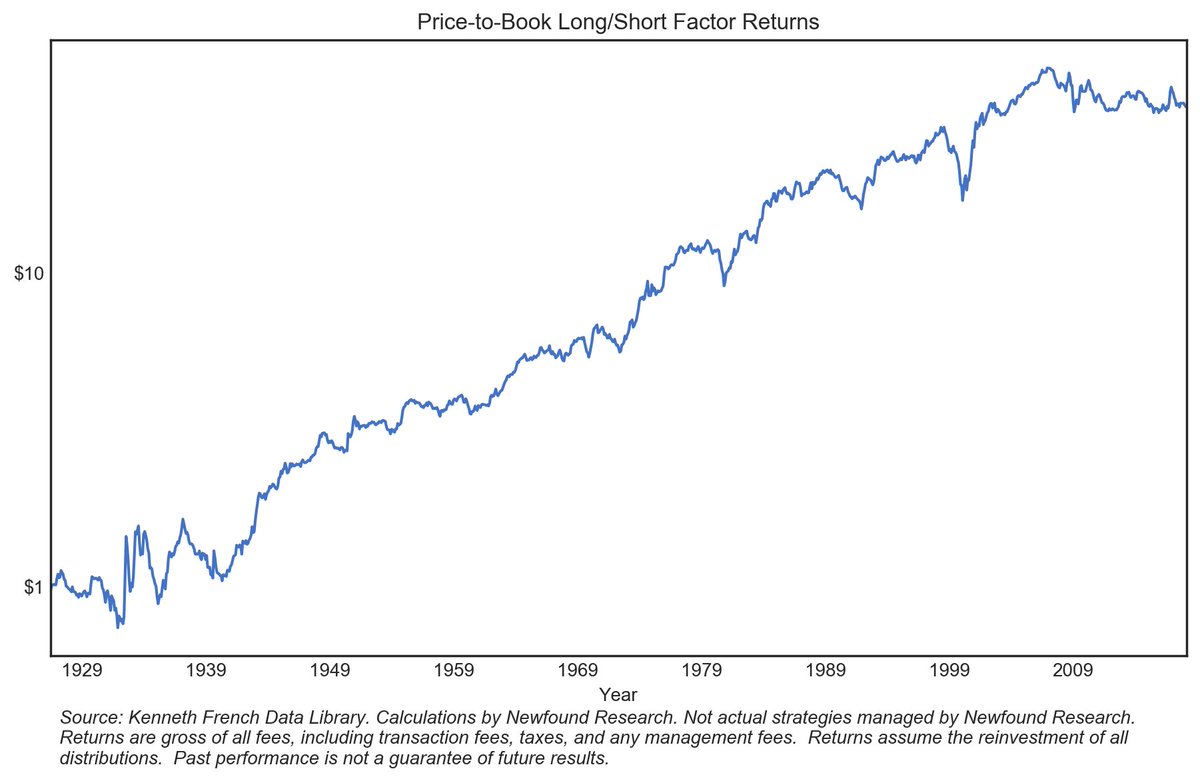

6/ The obvious example here is a portfolio that buys quantitatively cheap companies and short-sells expensive ones, attempting to capture the "value premium" independent of what the broad market is doing.

7/ Depending upon your perspective of the science behind the process, the identification and extraction of these alternative return sources is either akin to financial engineering, alchemy, or pure voodoo.

But then again, many people consider TAA to be market timing.

But then again, many people consider TAA to be market timing.

8/ By engineering new return sources, alternatives can potentially provide more consistent diversification.

In contrast, tactical strategies will likely have time-varying correlations to different systematic risk factors.

In contrast, tactical strategies will likely have time-varying correlations to different systematic risk factors.

9/ To use a really bad analogy, tactical strategies give you the ability to adjust the shades of the primary colors within your portfolio, while liquid alternatives give you entirely new colors to paint with.

10/ This gets a little confusing when we consider that many tactical strategies may be driven by the same quantitative styles that are captured by alternatives.

11/ For example, a long/flat tactical equity strategy using trend.

But we can really think of this as a 50/50 equity/cash portfolio plus 50% exposure to a long/short equity strategy.

From a diversification perspective, however, the structural equity exposure remains.

But we can really think of this as a 50/50 equity/cash portfolio plus 50% exposure to a long/short equity strategy.

From a diversification perspective, however, the structural equity exposure remains.

12/ And I think that's the real key. TAA has a structural element of systematic risk, while alternatives can potentially offer new sources of diversification.

13/ Even as a tactical manager, I have to admit that unique sources of diversification are almost always a superior way to manage risk (if they work).

The problem is that they are often opaque. Combined with negative realized tracking error and we have a behavioral nightmare.

The problem is that they are often opaque. Combined with negative realized tracking error and we have a behavioral nightmare.

14/ So here's my take:

If we believe in alternatives, we should use them up to our tracking error comfort level.

Beyond that point, if we have not diversified away sufficient systematic risk, we can consider tactical strategies.

If we believe in alternatives, we should use them up to our tracking error comfort level.

Beyond that point, if we have not diversified away sufficient systematic risk, we can consider tactical strategies.