As promised, a new blog post: "USS’s valuation rests on a large and demonstrable mistake: when corrected there is no deficit as at 31 March 2018 and no need for detrimental changes to benefits or contributions". 𝗣𝗹𝗲𝗮𝘀𝗲 𝗿𝗲-𝘁𝘄𝗲𝗲𝘁. 1/

medium.com/@mikeotsuka/us…

medium.com/@mikeotsuka/us…

It begins: "It is hard to overstate the importance of USS’s confirmation yesterday of the accuracy of union-appointed JNC member Sam Marsh’s modelling of some implications of their valuation." 2/

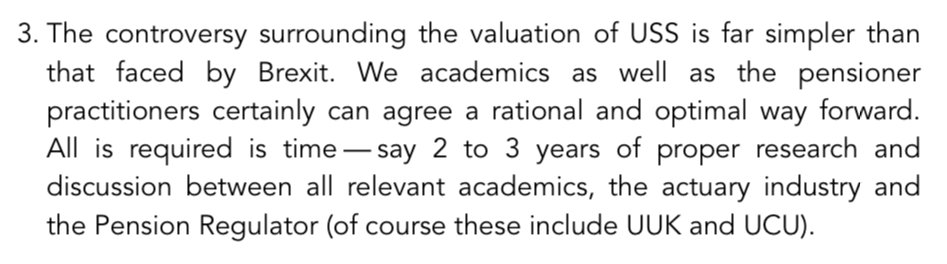

From the concluding section: 3/

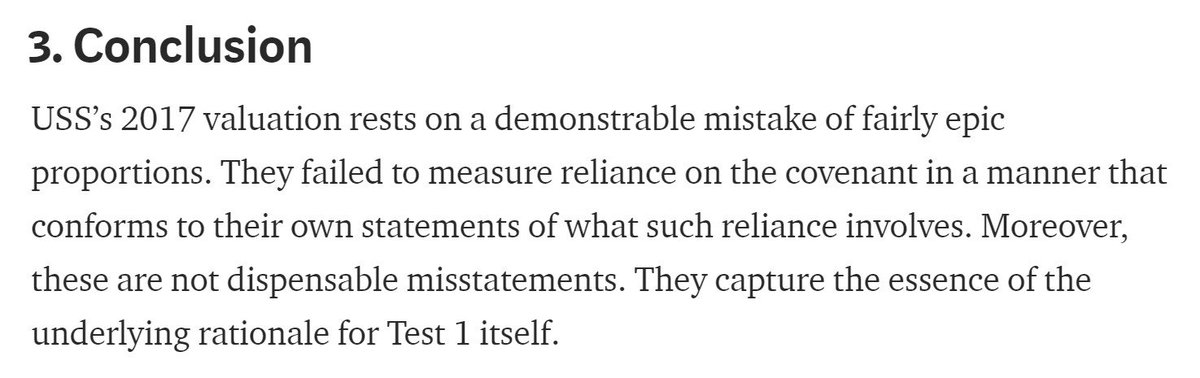

Another screenshot from the concluding section:

I think I correctly inferred here that @Sam_Marsh101's calculations were broadly correct:

Nikhil's incredulity is justified. Below I'll try to explain what I think happened. 1/

It wasn't a miscalculation on the part of #USS. Rather, it was a conceptual confusion, of a relatively subtle and excusable sort, which led them to think that they didn't need to make a calculation re column 1, since they had already established these values via... 2/

...their calculations that populated column 2. In this tweet, @Sam_Marsh101 explains why the values in column 2 needn't be the same as the values in column 1. But if you look at the many tweets above, you'll see that it took many tweets for him to explain to me how... 3/

...these values could actually come apart. Like me, many people in USS and perhaps also their actuarial advisers, assumed that, given what the two concepts involved, the two values had to converge. 4/

It didn't help that Test 1 is entirely an invention of USS, so there isn't a body of literature analysing the theory behind it. 5/

This wasn't a simple cock-up on #USS's part, of the sort involving a miscalculation. Rather, it was a failure to see that they needed to make calculations to establish the values in column 1, since they had not already been determined by the calculations in column 2. 6/

It required insight and an ability to 'think outside the box' on @Sam_Marsh101's part to see, and then prove, that these values could diverge. Like a lot of discerning insights, they seem obvious only in hindsight. 7/7

Missing link to tweet 👆: "...In this tweet, @Sam_Marsh101 explains why the values in column 2 needn't be the same as the values in column 1. But if you look at the many tweets above, you'll see that it took many tweets for him to explain to me how... 3/":

In response to @martin_oneill's embedded tweet: There is a lot for which employers should be held to accounts (e.g., their distorted representation of employer responses to the Sept 17 consultation). But not for this. 1/

Here responsibility lies almost entirely with #USS. Rather than picking a fight w/ UUK over this, the most effective response would be for @ucu & @UniversitiesUK to come together now & place maximal pressure on #USS to correct this error & value our pension scheme properly. 2/2

𝗧𝗿𝗮𝗻𝘀𝗽𝗮𝗿𝗲𝗻𝗰𝘆: @ucu, @UniversitiesUK (CEO @AlistairJarvis) & USS trustees (inc. @DaveGuppy & @UofGVC) should demand prompt answers from @GuyCoughlan & other USS executives to the following questions: 1/

1. Why did you fail to respond to the request on 29 Sept 2017 from Sheffield University USS working group for the value in col 1, row 1? 2/

2. Why did you fail to publicly release the cashflow projections that @Sam_Marsh101 requested, on grounds that you could not do so w/o trustee permission, while also failing to ask the trustee's permission? 3/

3. Why do you continue to refuse to publicly disclose the asset projections that JNC member @Sam_Marsh101 requested, as well as the underlying figures & calculations? 4/

4. What grounds, apart from embarrassment to #USS executives that would arise from such disclosure, do you have to deem this information "business sensitive" rather than public? 5/5

In this tweet and the one below it, @Sam_Marsh101 offers his account of where he thinks #USS went wrong. 1/

𝗜'𝘃𝗲 𝗷𝘂𝘀𝘁 𝗮𝗱𝗱𝗲𝗱 𝗮𝗻 𝗔𝗱𝗱𝗲𝗻𝗱𝘂𝗺 to the bottom of my blog post in which I diagnose a more general, fundamental error of #USS's in their design of Test 1. I'd be interested to learn whether @Sam_Marsh101 agrees w my take. Link to blog: 2/2

medium.com/@mikeotsuka/us…

medium.com/@mikeotsuka/us…

👆About 4,000 people viewed my blog post before 8 pm on Sunday, when I added my 𝗔𝗱𝗱𝗲𝗻𝗱𝘂𝗺 in which I think manage to provide a simple, clear & compelling diagnosis of USS's error. If you're one of them, please click the above link & scroll down to the bottom of the post.

👆🧐Tagging @AlistairJarvis @JoanneSegars @SallyBridgeland @RedActuary @Derek_Benstead @kevinwesbroom @USSbriefs @OpenUPP2018 @JosephineCumbo & @henryhtapper to draw their attention to the Addendum.

.@markmleach's @Wonkhe Monday Morning Briefing has just landed in the email inboxes of various VC's and university FDs. And it includes this!:

And here, hot off the press, is @Sam_Marsh101 nice, succinct commentary on his findings:

medium.com/ussbriefs/a-fl…

medium.com/ussbriefs/a-fl…

USS has responded to the above, and here is my reply:

medium.com/@mikeotsuka/a-…

medium.com/@mikeotsuka/a-…

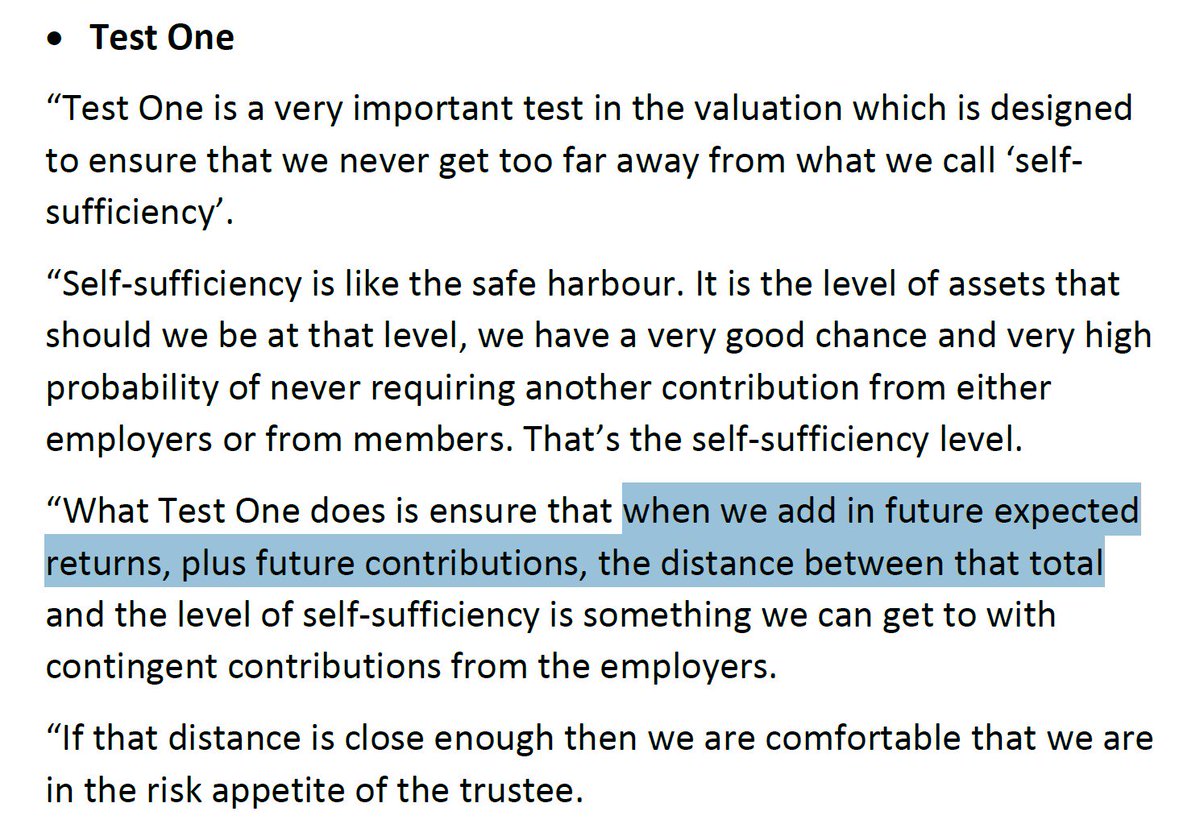

In this follow-up statement, #USS finally engages in the substance of the critique of Test 1 that arises from @Sam_Marsh101's findings: 1/

This is their argument for ignoring the asset projection in row 1, column 1: 2/

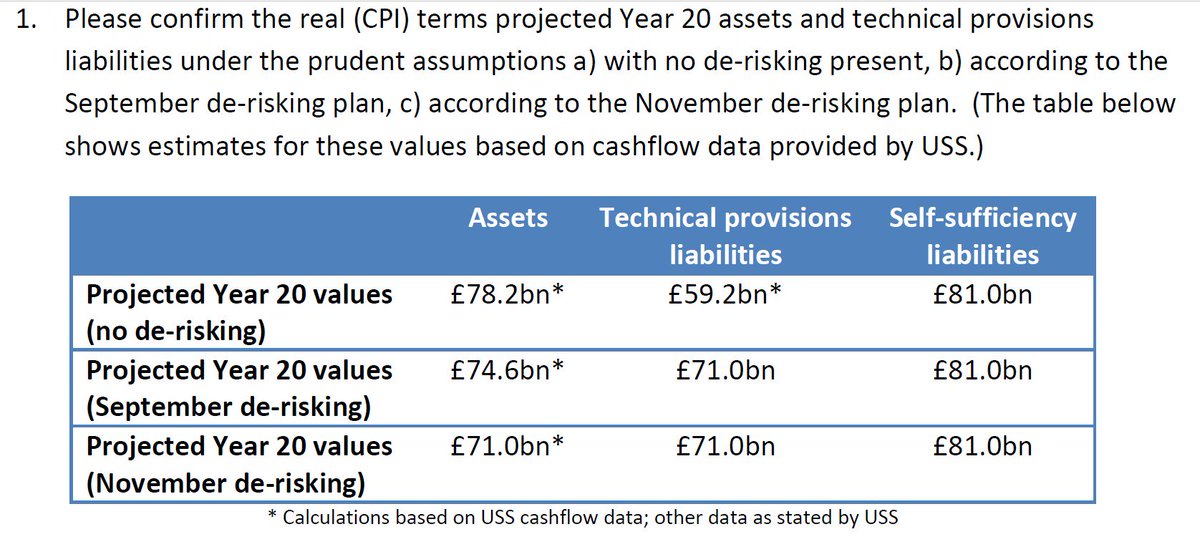

Their initial response, however, was quite different. When @Sam_Marsh101 pointed out that the values in row 1, column 1 & row 1, column 2 in the chart below differed... 3/

...the was the scheme actuary's initial response! 4/

In other words, they did not initially realise that these values diverged. This caught them by surprise. But they have now come up with a line of response. 5/

Recall that, a little over a year ago, @FirstActuarial pointed out this unusual feature, regarding the falling cost of future service, w #USS's valuation. During the Sept 2017 consultation, both they & Sheffield University USS working group asked #USS to confirm this feature. 7/

In their typical slow-responsive fashion, #USS refused to confirm this until well after the close of the valuation. In this blog I explain why the consultation was undermined by this refusal. 8/

medium.com/@mikeotsuka/us…

medium.com/@mikeotsuka/us…

What is emerging from all this #USS has built multiple unacknowledged layers of prudence into the valuation. Here is JEP's list of some of these layers: 9/

It is only a month or a year after the initial, disastrous Sept 2017 consultation that #USS discloses these facts. Lack of transparency remains a serious problem. 10/

For this reason, it is disappointing that, in their responses to @JosephineCumbo, #USS has not provided satisfactory answers to the four questions regarding transparency that I posed in tweets below this tweet: 11/

Scheme members, and, I would think, trustees such as @DaveGuppy & @UofGVC, will be very interested in any answers @JosephineCumbo is able to elicit, esp. to the following question: 12/12

I will eventually write a blog post on USS's claims regarding the smoothing of the cost of future service over 20 years. Here is a preview of one of the points I will make: 1/

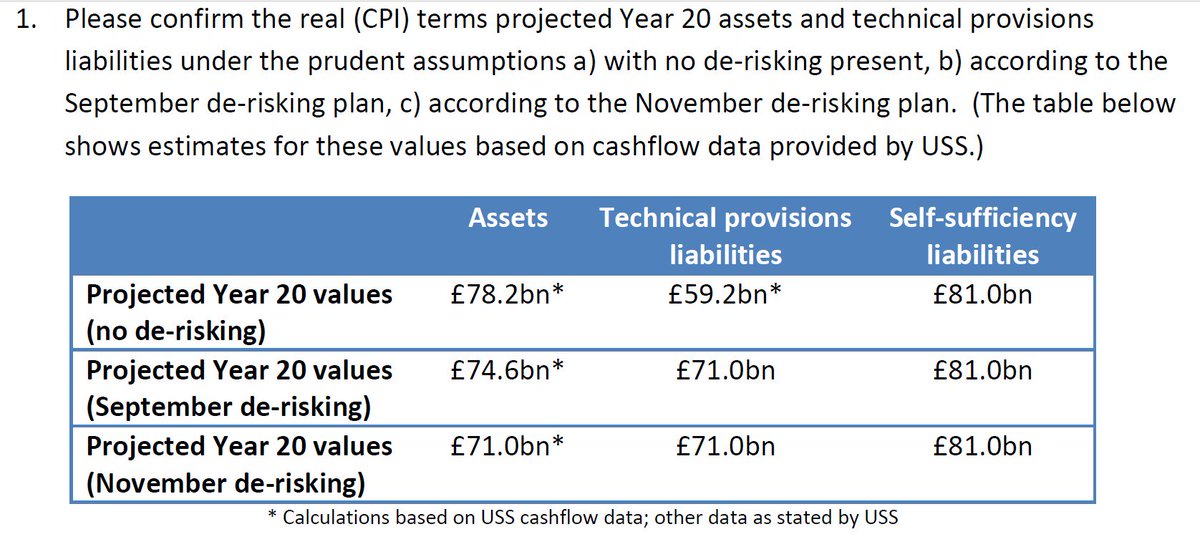

It's one thing to determine what the level of the scheme's assets will be in 20 years' time under current contribution rates, benefit & portfolio, in order to determine the size of the gap to self-sufficiency then. 2/

That calculation is made in order to determine whether the scheme would be within affordable distance of self-sufficiency by then if we carried on as at present. If it would be within affordable distance, then there is no Test 1 call for de-risking the portfolio. 3/

We then determine the costs per year of future service, given the current (non-de-risked) portfolio, and have a further discussion of what sort of smoothing of contributions would be warranted if these costs vary from year to year. 4/

In their linked statement, #USS fails to distinguish these two separate steps, the different considerations they involve, and the need to carry out the first step before the second one. (Tagging @Sam_Marsh101 for his thoughts.) 5/5

USS is rewriting history. This aspect of the valuation was REVEALED by @Derek_Benstead & @RedActuary of @FirstActuarial in their mid-September response to the September consultation document. See here: 2/

And here: 3/

As I note above, even though the Sheffield Uni USS working group requested confirmation from USS on 29 Sept 2017 of FA's finding, USS did not reply until AFTER the valuation. 4/

#USS's failure to confirm @FirstActuarial's finding until AFTER the close of the consultation rendered that consultation problematic, for reasons that are captured in the headline of this linked blog post: 6/

medium.com/@mikeotsuka/us…

medium.com/@mikeotsuka/us…

I hope @UniversitiesUK employers & @AlistairJarvis, plus UUK actuary @kevinwesbroom, review the details in my above linked blog post and then press #USS to explain why they did not disclose, until after close of the consultation... 7/

...that #USS was charging employers & members for future service ON THE ASSUMPTION THAT THE GILT YIELD DOES NOT REVERT. 8/

#USS therefore failed to reveal something which would have laid to rest employer fears expressed during the consultation about what would happen if the gilt yield didn’t revert as USS expected. 9/

#USS could have responded that they had already hedged against this by charging us at the rate as if the gilt yield doesn't revert. So we get a bonus if gilt yields revert as USS forecasts rather than incurring a penalty if it doesn't. 10/

#USS instead chose to speed up the onset of de-risking (aka November de-risking) rather than delaying its onset for 10 years as they had proposed in their Sept consultation document. 11/

In other words, #USS gratuitously chose to do something -- speed up the onset of de-risking -- which both UCU & many employers opposed and which JEP has recommended against. 12/

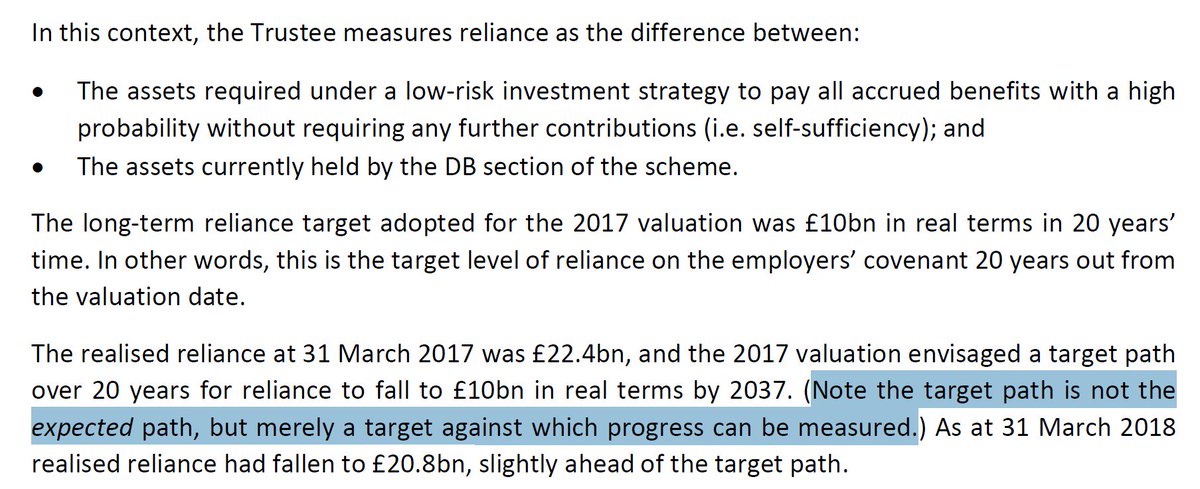

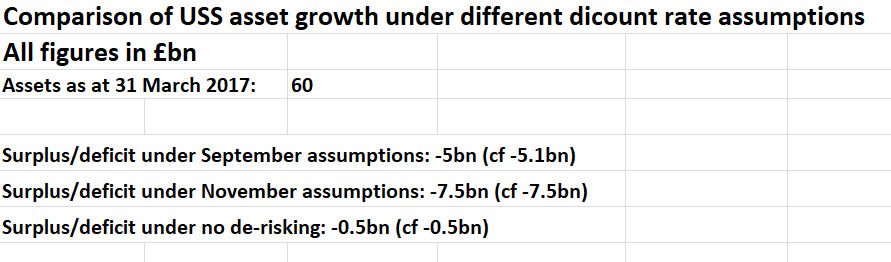

Yesterday, we learned that #USS built in a more massive hedge against a failure of gilt yield reversion by in effect setting the assumed asset level of the scheme in 2037, for the purpose of measuring the reliance gap to a self-sufficiency portfolio... 13/

....as the level that would obtain in the event of no gilt yield reversion. They did not explain to stakeholders that they had built this massive extra layer of prudence into their implementation of Test 1. 14/

I think they didn't explain this to us because they did this by accident, w/o awareness that this is what they had done, rather than intentionally. Cock-up, not conspiracy. See this tweet & the one below it, which indicate that it was inadvertent: 15/