Your weekly dose of "I need to buy a bunker" Market Reflexivity:

Pensions account for their future liabilities by discounting them at an est. return.

Most are projecting +7%/yr, but if you drop to 4%, CA's liability, for instance, goes up by $200bn

Pensions account for their future liabilities by discounting them at an est. return.

Most are projecting +7%/yr, but if you drop to 4%, CA's liability, for instance, goes up by $200bn

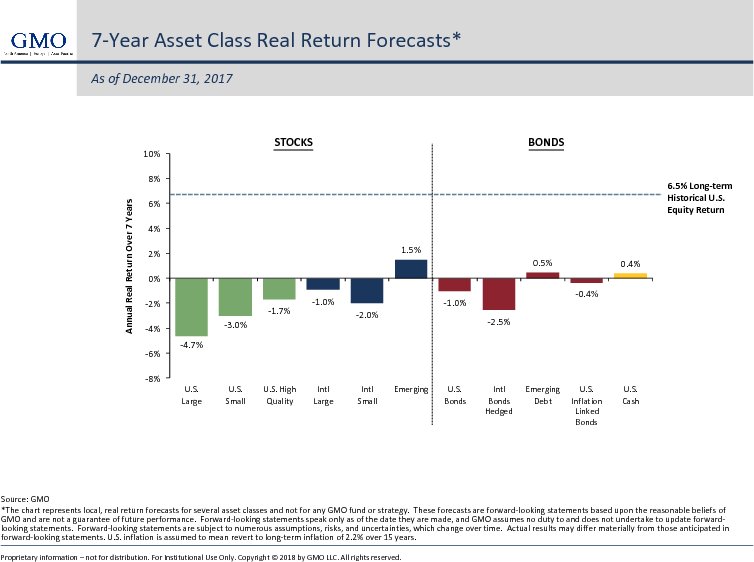

They sure as hell can't get that from treasuries with rock bottom rates.

And GMO is predicting *negative* 7 year returns for most stocks

So what do they do?

And GMO is predicting *negative* 7 year returns for most stocks

So what do they do?

You move out on the risk curve and allocate to "alternatives" -- the alt coins of the real market.

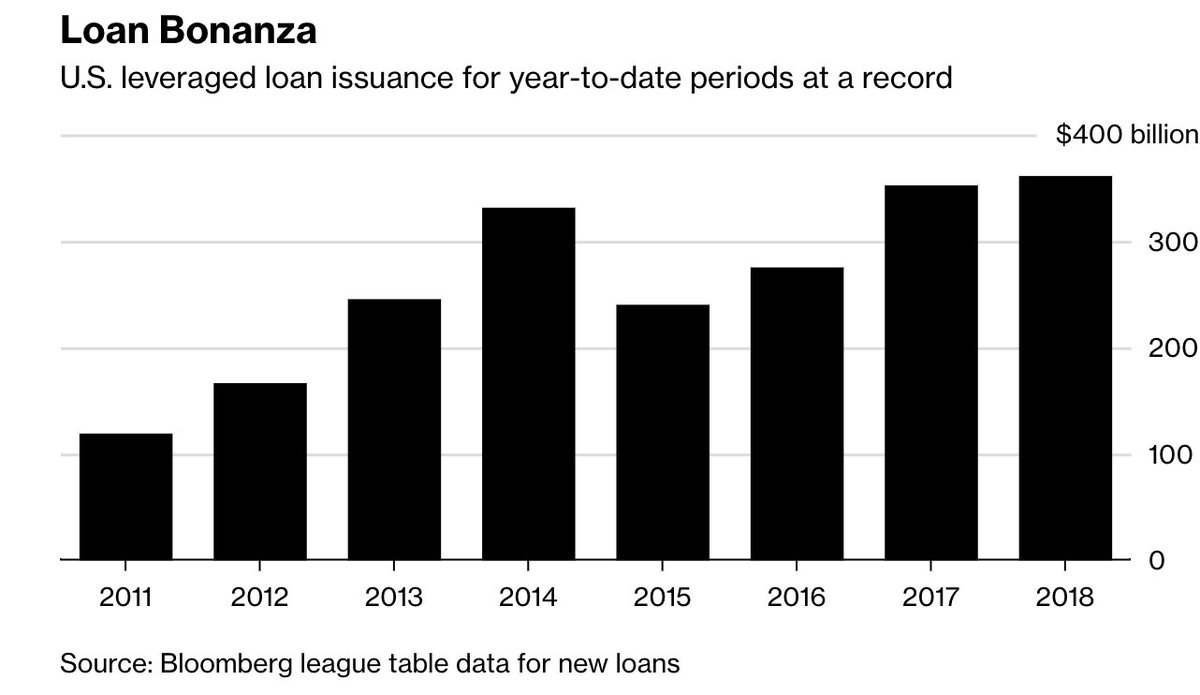

Levered loan funds -- funds that invest in riskier loans -- are hitting all time record raises. I'm sure you've also noticed the massive vc raises too.

Levered loan funds -- funds that invest in riskier loans -- are hitting all time record raises. I'm sure you've also noticed the massive vc raises too.

Covenant lite loans -- those with less restrictions -- just hit 80% of total levered loan issuance.

The excess loan demand allows issuers to relax restrictive requirements (like cash flow return, leverage ratios, etc).

The excess loan demand allows issuers to relax restrictive requirements (like cash flow return, leverage ratios, etc).

This pushes down rates. Junk bond spreads -- the difference between the rates junk bonds and us treasuries pay -- hit their lowest level since July 2007

As the risk premia falls, pension funds need to take on *even more* risk to get paid

As the risk premia falls, pension funds need to take on *even more* risk to get paid

Companies, with their artificially low rates are able to take on debt they otherwise wouldnt

And with debt from the unreasonably low rates, they buy back stock, because it's almost always accretive at rock bottom rates and their execs are compensated based on EPS

And with debt from the unreasonably low rates, they buy back stock, because it's almost always accretive at rock bottom rates and their execs are compensated based on EPS

According to @ArtemisVol, 40% of earnings growth and 30% of stock gains since 2009 have been from buybacks

So all in all, pensions reaching for yield has driven down corp. rates, fueled buybacks and the stock market, which increases company's access to capital allowing them to refi / pay off levered loans and generates outsized returns for the pension funds --fueling the cycle further

But what happens as yields rise and liquidity dries up?

(1) It's no longer accretive to buy back stock at higher rates. Company's are forced to actually invest for growth. Wages increase. Zombie co's exposed.

(2) Debt service increases, reducing profitability and EPS growth

(1) It's no longer accretive to buy back stock at higher rates. Company's are forced to actually invest for growth. Wages increase. Zombie co's exposed.

(2) Debt service increases, reducing profitability and EPS growth

(3) Company's have trouble paying off debt. More junk bonds default. Levered loan funds actually fall in value

(4) Yields increase further as demand for levered loans fall. Company's can no longer refi debt. Bankruptcies. Bad news bears.

(4) Yields increase further as demand for levered loans fall. Company's can no longer refi debt. Bankruptcies. Bad news bears.

(5) Pension funds liabilities soar as returns fall

As @EricRWeinstein frequently says, there are ponzi / pyramid schemes embedded in many of our revered institutions

Pension fund viability was predicated on the largest bull market of all time...which could be coming to an end

As @EricRWeinstein frequently says, there are ponzi / pyramid schemes embedded in many of our revered institutions

Pension fund viability was predicated on the largest bull market of all time...which could be coming to an end

Demographically and politically this is concerning. Millenials are extremely indebted and the elderly are wealthier than ever. But will they be forced to bail them out"?

A stock market that isn't increasing 6%/yr will expose the vulnerabilities and tail risk we've created

A stock market that isn't increasing 6%/yr will expose the vulnerabilities and tail risk we've created

@gabebassin for the inspo