,

24 tweets,

8 min read

Read on Twitter

Lyft S-1 is interesting for sure. Some good stuff, some things that raise some questions. A few things that jump out.

The most surprising thing to me was the relentless rise in take rate. I did not expect to see revs as a percent bookings at 28.7%. This is important, because I am skeptical this can go too much higher, and as we'll see, has driven a significant improvement in economics.

If you look at the change in bookings per ride versus revenues per ride, you can see how significant the increase in take rate has been on a per ride basis

If you look at the Y/Y change in the metrics they disclose, you can see that rider growth is meaningfully slowing. Rides/per rider has slowed too, such that rides are growing slightly above rider growth. So rev growth is being turbocharged by the increase in revs per ride.

here's sequential growth, can see riders growth hit mid single digits in Q4

Now to the cohorts. These show total rides in a given year per cohort. Two impressive things here, each year's new cohort is meaningfully bigger than the prior years, and solid increase in rides per cohort over time.

However, unless I'm thinking about this wrong, if you look at the change in cohorts over time, there is degradation. This shows change in riders by cohort by year. It appears that retention is falling each year, e.g. 2015 cohort grew rides 23.6% in Year 3, but 2016 only by 2.8%.

So the good news is they are able to bring in successively larger cohorts, but it appears those cohorts are growing far slower.

Another piece of good news has been the rapid rise in what they call contribution, but which appears to be gross margin.

Here's the full P/L. Q is what expense items can they leverage. Operations doesn't appear to be scaling, but assume it gets to 10-12%. R&D also at 10-12%. Say 50% GMs over time, that leaves 25-30% for S&M/G&A, currently running 50%. G&A should get to < 10. Can S&M get under 20?

If I were to summarize, I am concerned that take rates can't be pushed much higher, meaning revenue growth converges with growth in rides * change in bookings per ride. Might be some upside left in GM's, but to get to profitability requires meaningful leverage in S&M and G&A.

I think this means that the right way to compare ride sharing take rates to other marketplaces isn't revenue as percent of bookings, but rather Gross Margin (or Contribution for Lyft) as percent of bookings.

Here's Gross Profit as a percentage of bookings for Lyft. Would have the take rate in the low teens and rising.

Comparing Lyft's 13% to other marketplaces (and Gurley took issue with some of these take rates but just using it as a proxy) seems more reasonable. But again I wonder how much more room to push they have here.

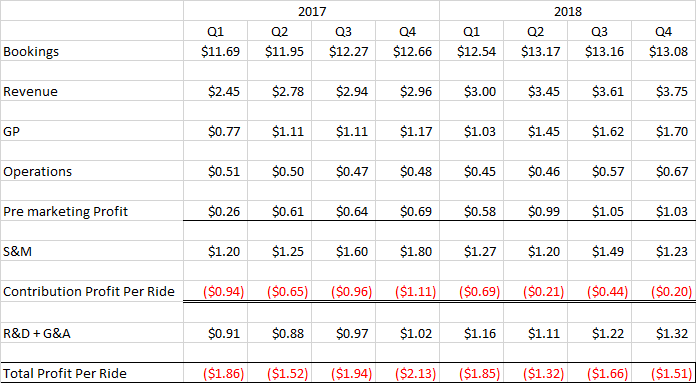

This is the P/L broken down per ride. Pre marketing profit (PMP) per ride, which is revs - COGS - Ops, has materially increased due to higher GMs, tho is flattish last 3 Q's. Contribution per ride (PMP - S&M) is improved but negative, and S&M per ride hasn't leveraged in 2 years.

WSJ had Uber financials through Q2 2018. Uber had lower take rate, 1300 bps higher gross margins, and significantly lower Ops/S&M/R&D as % of sales.

Uber "marketplace equivalent take rate" was 180bps higher in Q2 18 vs Lyft, despite 290bps lower take rate, b/c of higher GMs.

Uber "marketplace equivalent take rate" was 180bps higher in Q2 18 vs Lyft, despite 290bps lower take rate, b/c of higher GMs.

No idea if these are like for like, but if so, with a lower Rev take rate, much higher GM's, and more efficiency on expense line items, it seems far easier to model Uber getting to meaningful profitability, which tbh makes sense.

So Lyft gave long term aspirational guidance of 70% gross margins and 20% ebitda margins. I am... skeptical. Uber is multiples larger and has 55% gross margins. Lyft currently has 45%.

Using 20% margins, for a given level of EBITDA $, you can calc Billings, Rides, Riders, etc. Say you think $30B EV requires $2B in EBITDA. Assume 30% take rate (vs 28% today), $17.50/ride (vs $13) and 12.5 rides/rider (vs 9.6). They need 38.1M riders per quarter, vs 18.6M today.

10% EBITDA margin seems more likely (if at all), because GM's of 60% vs Uber at 55% today seems more reasonable. Here's a sensitivity table of Margin vs Rides per Rider, to generate $2B in EBITDA. At a 10% margin, you'd need 50M riders per quarter even if rides/rider doubles.

this also assumes billings/ride increase from $13 to $17.50. But implicit in the idea ridesharing displaces car usage to the extent required by the number of riders and rides/rider in the calc above, you would assume pressure on billings/ride. Billings/ride has fallen last 2 Qs.

Also, 30% take rate strikes me as aggressive. If you combine that with a 70% gross margin, you get a 21% "marketplace take rate" vs today's 12-13%, which would then get us back to the pt where even using Gurley's formulation of GP/Billings, ridesharing take rates seem aggressive.

With 10% margins and $15/ride, it's 74M riders a quarter taking 15 rides per quarter to get $2B in Ebitda. I'm not saying that's impossible. The single biggest mistake in assessing the TAM for ridesharing has been dramatically underestimating it.

abovethecrowd.com/2014/07/11/how…

abovethecrowd.com/2014/07/11/how…

If Lyft is doing ~1B+ rides per quarter, as implied by the numbers above and it has 40% share, that means there are 2.5B rides per 90 days in the US, or 28M rides per day. I have no idea what the average driver is doing in rides/day, but we're gonna need a lot of drivers.