,

31 tweets,

19 min read

Read on Twitter

A thread on the latest CPA construction forecasts & 'No Deal' scenario (I'll summarise the results initially and then provide background/context)...

#ukconstruction #ukhousing #Brexit #NoDeal

#ukconstruction #ukhousing #Brexit #NoDeal

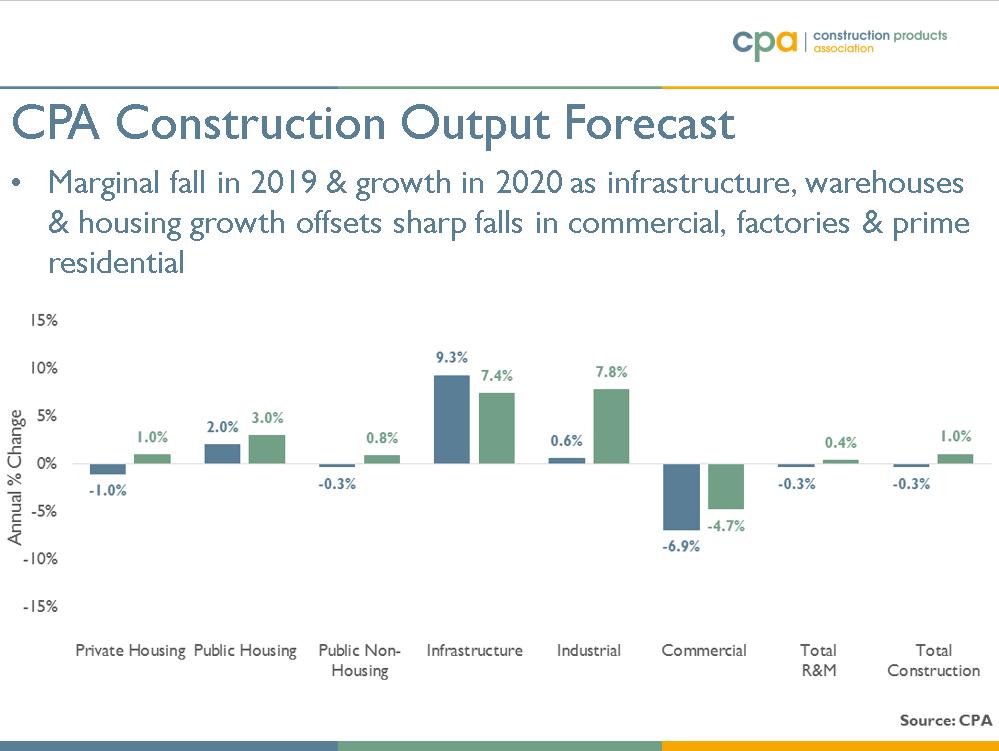

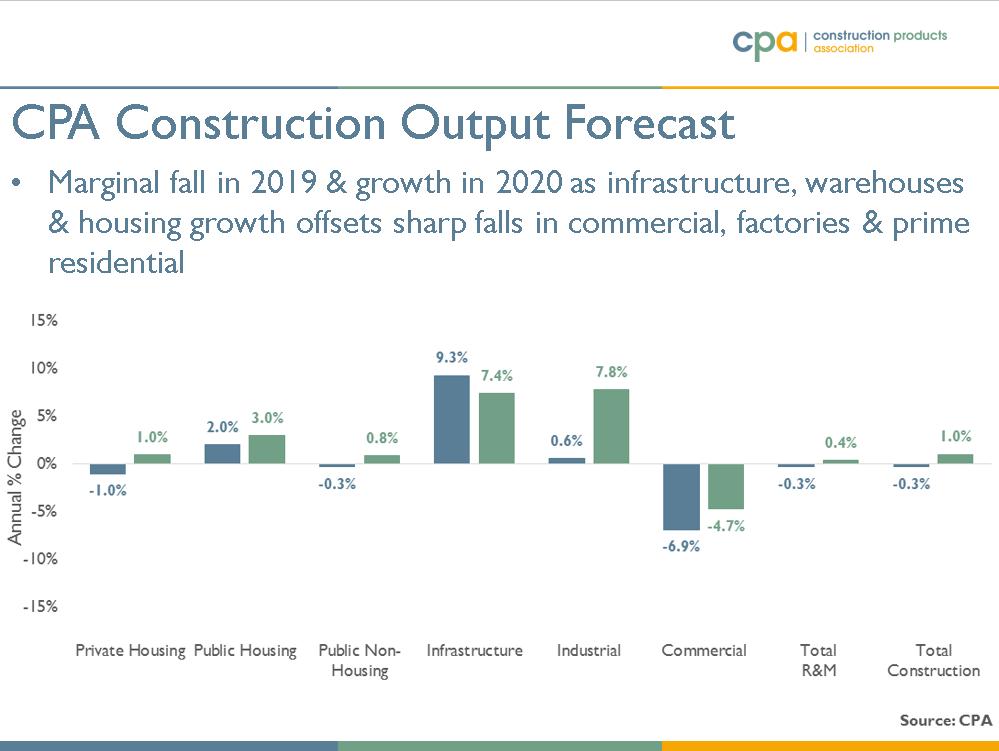

The CPA is forecasting that construction output will fall marginally (-0.3%) in 2019 & grow by 1.0% in 2020 assuming a smooth Brexit (either the Withdrawal Agreement with a fudge on the backstop or another delay to Article 50)...

#ukconstruction

#ukconstruction

... but construction activity is mixed by region & sector. Infrastructure, housing (North West, Yorkshire & Midlands) & industrial warehouses growth offsets falls in commercial, industrial factories & housing (London, South East & parts of the East)...

#ukconstruction #ukhousing

#ukconstruction #ukhousing

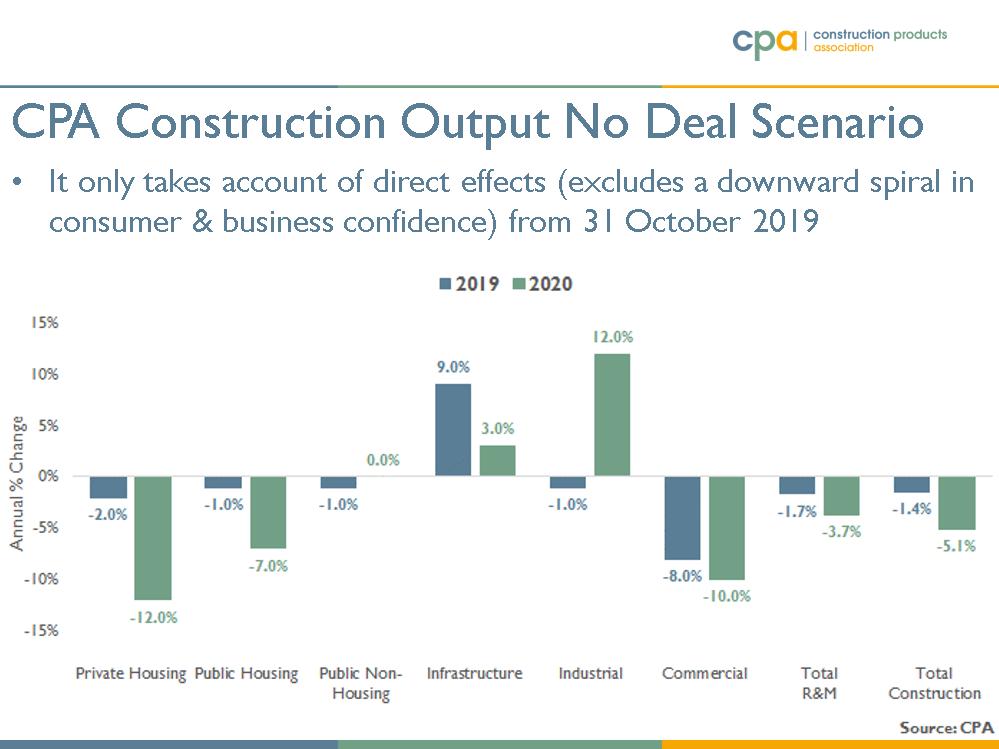

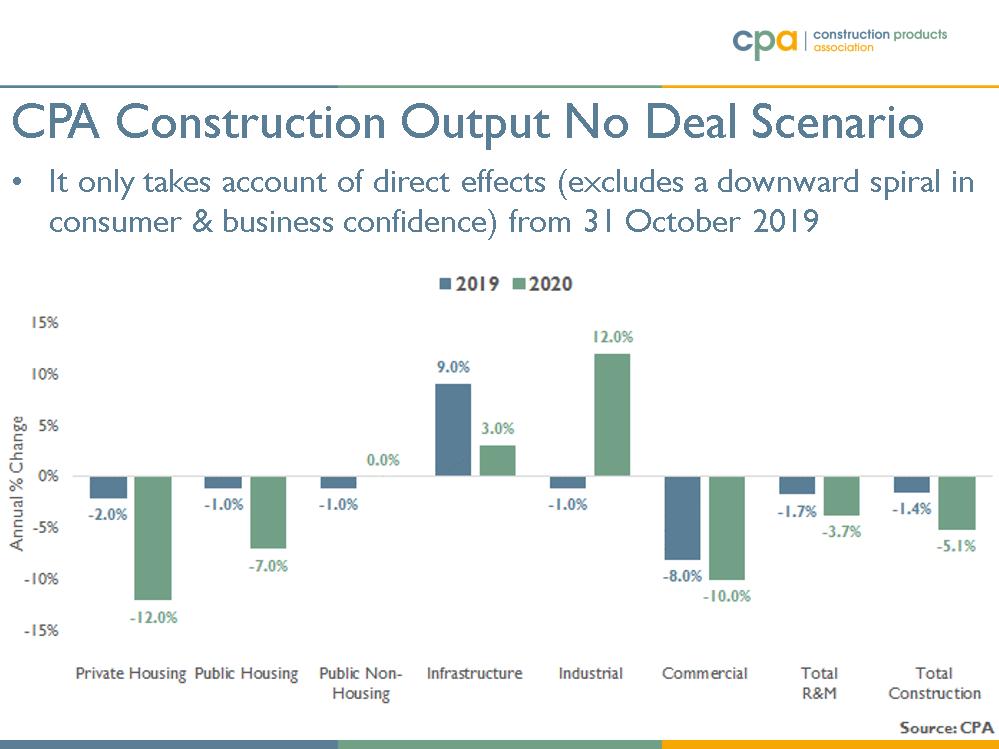

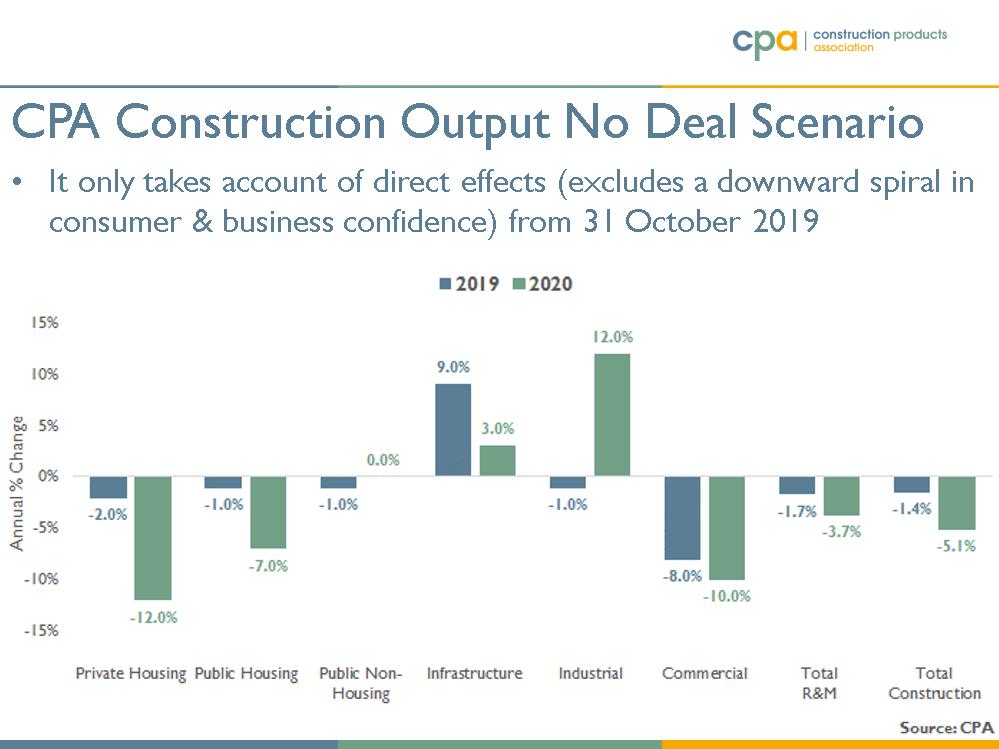

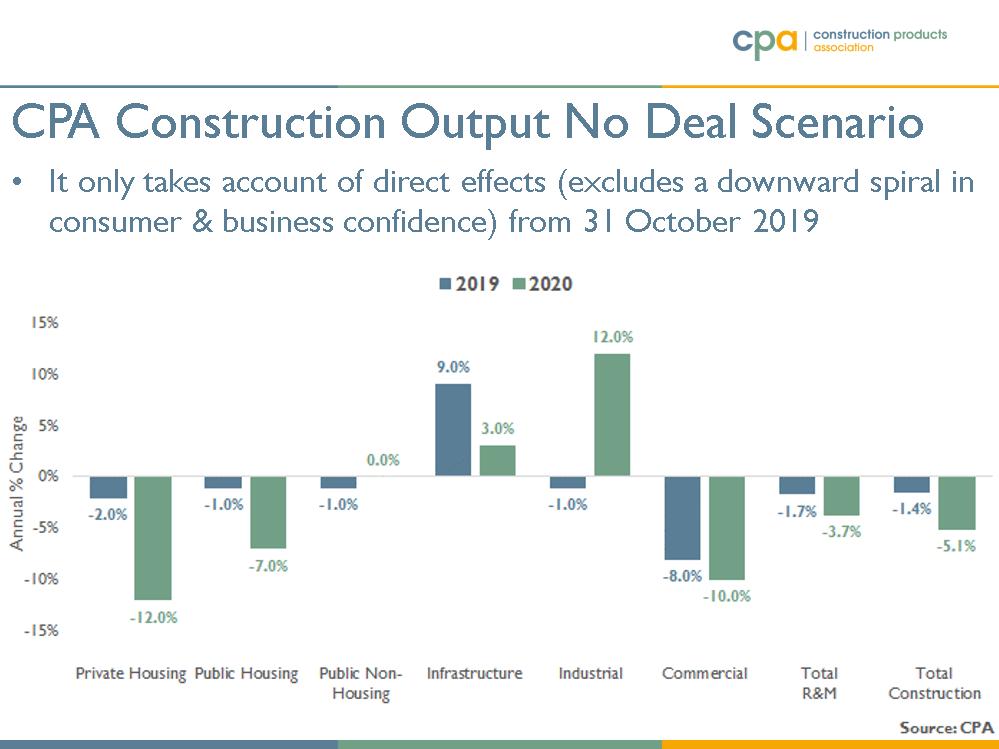

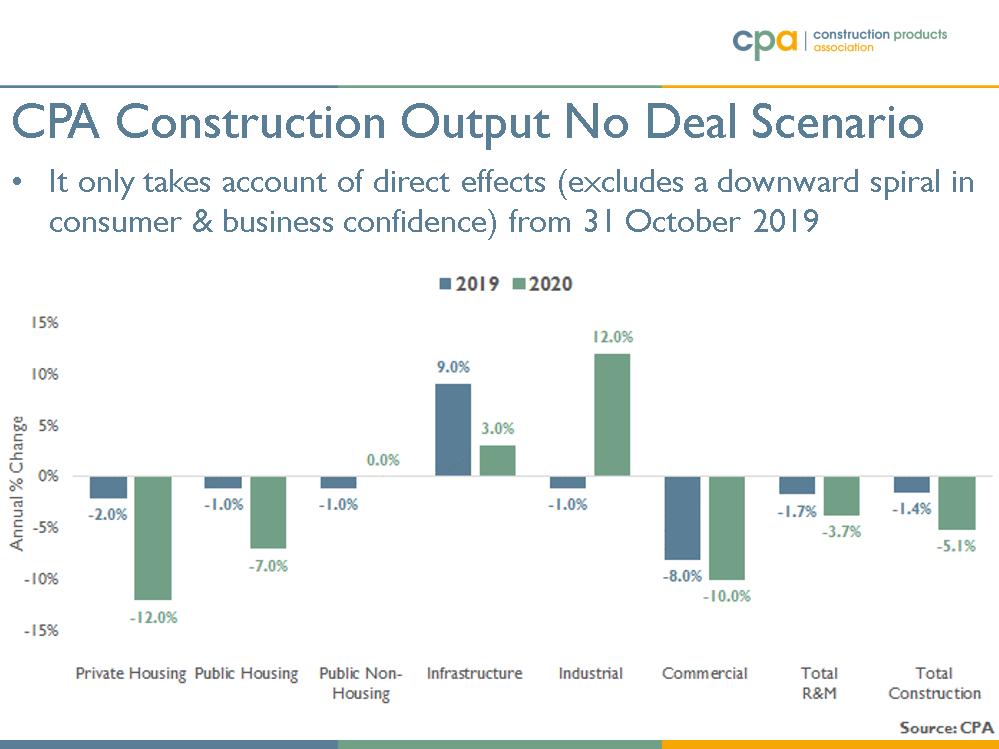

... whilst a 'No Deal' scenario would lead to falls in construction output of 1.4% in 2019 & 5.1% in 2020 although clearly it would adversely impact on some sectors more than others...

#ukconstruction #ukhousing #brexit #nodeal

#ukconstruction #ukhousing #brexit #nodeal

... as private housing output falls 2% in 2019 & 12% in 2020, Commercial output falls 8% in 2019 & 10% in 2020. Infrastructure output rises 9% in 2019 & 3% in 2020. Industrial falls 1% in 2019 & rises 12% in 2020.

#ukconstruction #ukhousing #brexit #nodeal

#ukconstruction #ukhousing #brexit #nodeal

Some background/context. In the UK economy, GDP has carried on rising since the EU Referendum but business investment slowed (& then fell throughout 2018) in spite of high capacity constraints as firms cannot commit to high upfront investment for a long-term rate of return...

... & firms focused on cost reduction & risk aversion. Many firms stockpiled in 2018 Q4 & 2019 Q1 but that may not be possible for those using external warehousing in 2019 Q3 given retailers reserving space well in advance for Black Friday & Christmas...

Consumers report poor sentiment but employment is high & there is real wage growth so households are largely ignoring Brexit uncertainty & continue to spend, which appears to be keeping economic growth going given consumption drives the UK economy.

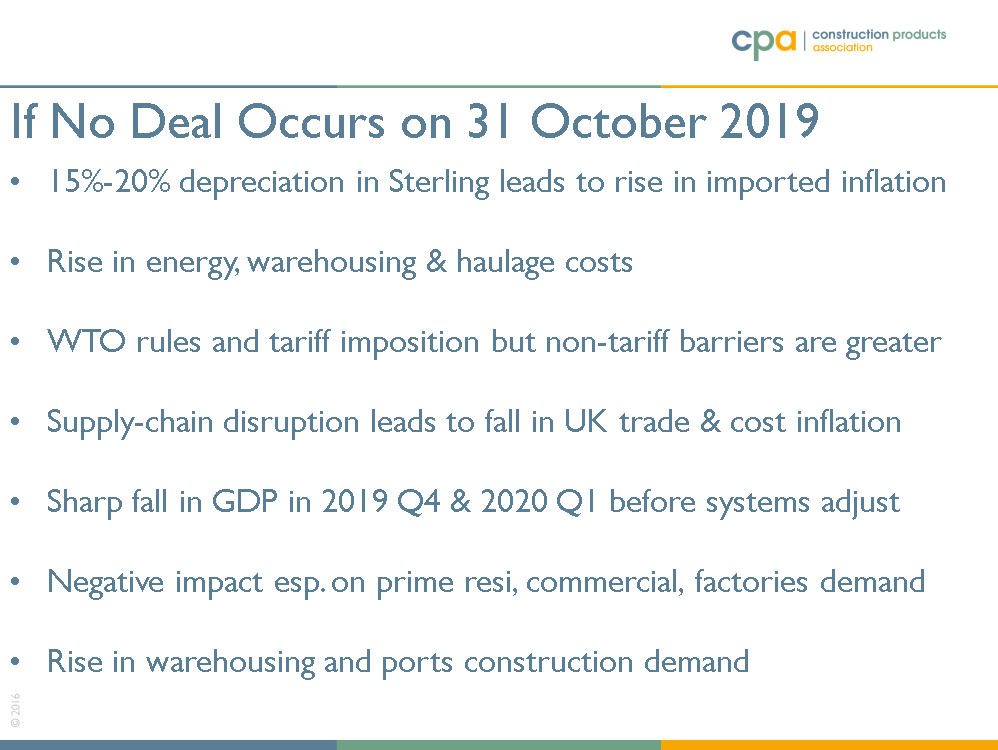

However, consumer spending continues to rise whilst inflation is low. If Sterling continues to depreciate & so imported materials, products & energy/fuel prices rise, that could impact badly on firms & consumers. Our 'No Deal' scenario has a 15%-20% fall in Sterling.

The problems are greatest for firms in the UK that are globally headquartered as they report turnover/profit in local currency. How do you plan for next year when, assuming constant revenue, a deal means an appreciation (say 5%-8%) in Sterling & so a 5%-8% rise in turnover...

... whilst a 'No Deal' may mean a 15%-20% depreciation in Sterling & consequently a 15%-20% fall in turnover in local currency. That's a very wide range of turnovers to try to plan for... & that assumes no change in UK turnover (which is unlikely given the impacts on demand).

For all the noise/speculation/political chaos over the past few months, the issues & essential options remain largely the same although the probabilities (approximate!) have & the likelihood of 'No Deal' has clearly risen considerably...

... forget whatever politicians are saying openly (as it often inconsistent & contradicts what they have said previously) but 'No Deal' has increased in likelihood due to the lack of time available, 31 October is not that far away given recess & party conferences...

... but, theoretically, there could still be an election in Autumn in an attempt to get a strong majority to enact policy (although that was tried in 2017 & didn't work well).

All of which means it is very difficult to forecast construction output by sector so it is important to understand the underlying assumptions made in the construction forecasts & in the 'No Deal' scenario.

We assume either a deal with the EU (effectively the Withdrawal Agreement without, or a limit on, the backstop (to get into the implementation period) or another delay to Article 50, which means trading conditions remain the same but medium-term uncertainty remains...

... which means that consumers continue to spend whilst unemployment remains low & whilst there is still real wage growth but larger firms & business investment continues to fall so UK economic activity continues to grow at subdued rates (below 0.5% per quarter)...

... & construction output falling only marginally (0.3%) in 2019 & rising (1.0%) in 2020 is heavily dependent on:

1) House building in the North West, Yorkshire & Midlands offsetting falls in London, South East & parts of the East...

2) Government delivery of infrastructure

1) House building in the North West, Yorkshire & Midlands offsetting falls in London, South East & parts of the East...

2) Government delivery of infrastructure

The CPA 'No Deal' scenario assumes a 15%-20% depreciation in Sterling & so rises in energy/fuel, warehousing & haulage costs, a sharp fall in GDP in 2019 Q4 & 2020 Q1 whilst systems adjust & lagged impacts on construction investment & output.

#ukconstruction #brexit #NoDeal

#ukconstruction #brexit #NoDeal

The 'No Deal' scenario has a 1.4% fall in construction output in 2019 & 5.1% fall in 2020. The greatest impacts are in residential, commercial offices & industrial factories (high upfront investment for a long-term rate of return)...

#ukconstruction #brexit #nodeal

#ukconstruction #brexit #nodeal

... but the 'No Deal' scenario anticipates increases in investment in sub-sectors that help deal with risk aversion/contingency such as industrial warehouses & infrastructure ports...

#ukconstruction #brexit #nodeal

#ukconstruction #brexit #nodeal

The 'No Deal' scenario sees a 6.4% fall in construction output by the end of next year, this is less than half the fall in construction output due to the financial crisis but note that this only takes account of direct effects.

#ukconstruction #brexit #nodeal

#ukconstruction #brexit #nodeal

A few slides of points to keep in mind when looking at the impacts of Brexit on the construction industry...

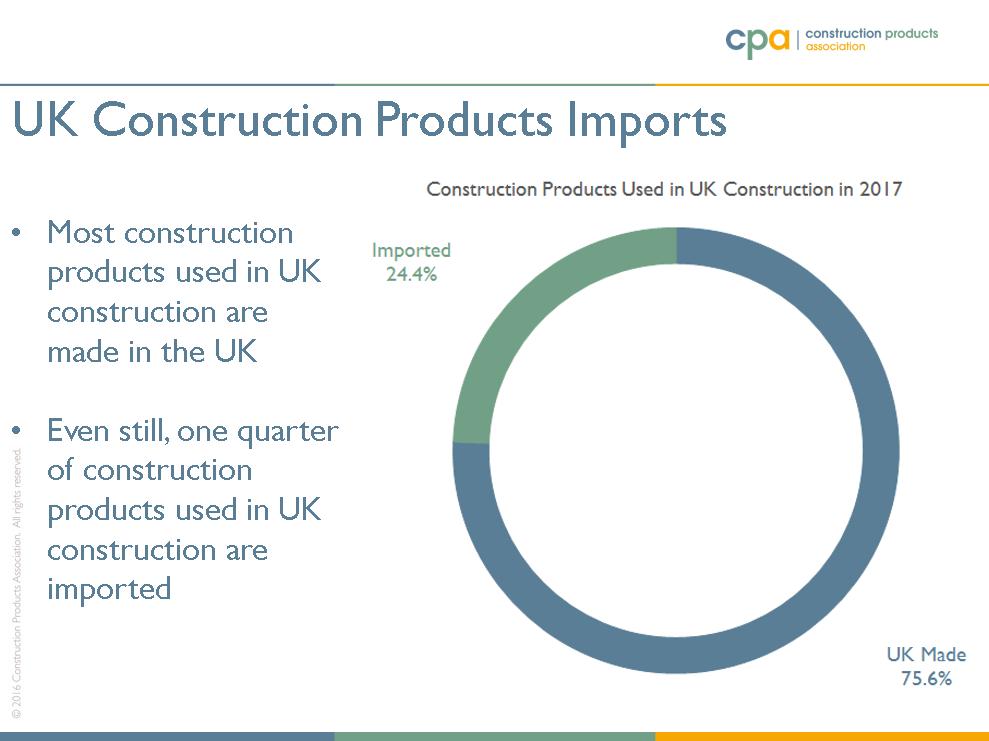

76% of products used in UK construction are made in the UK so Sterling depreciations directly raise costs on 24% of construction products but indirectly raise costs on the other 76% due to effects on imported materials, components, fuel & energy costs.

#ukconstruction #brexit

#ukconstruction #brexit

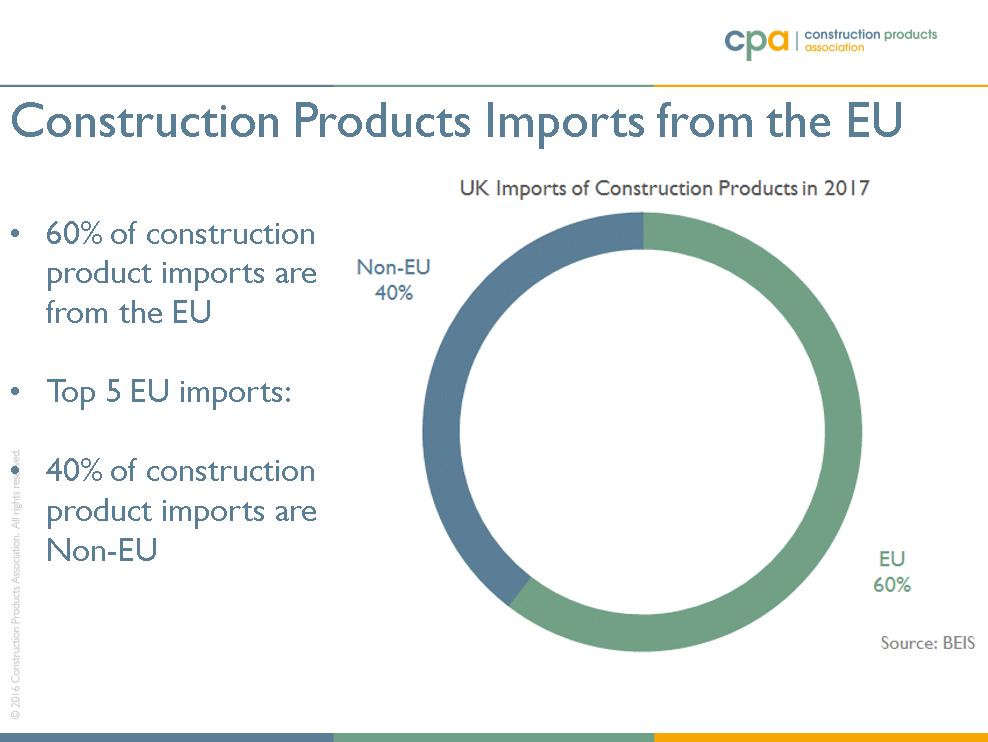

Of the 24% of construction products used in UK construction that are imported, 60% come from the EU (proximity being a key issue) so if there are EU & UK trade issues then it could impact significantly on construction product import supply & cost...

#ukconstruction #brexit

#ukconstruction #brexit

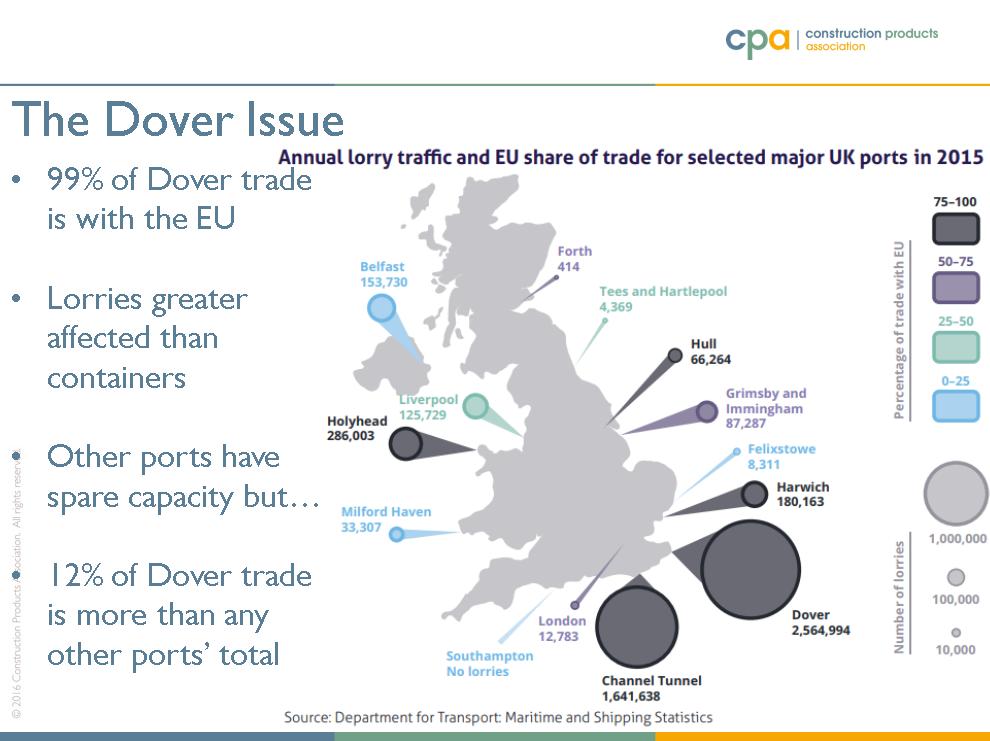

... but if there are EU & UK trade issues, it is likely to impact directly on Dover but construction products come to ports on the East coast (which do have additional capacity) although if some of Dover's trade shifts to other ports there may be issues.

#ukconstruction #brexit

#ukconstruction #brexit

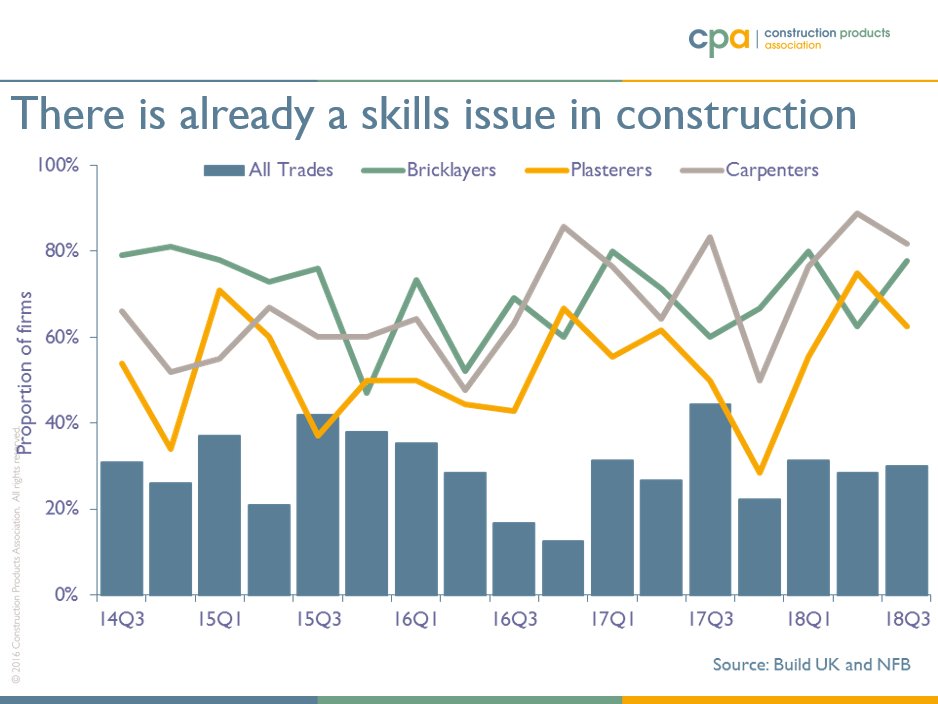

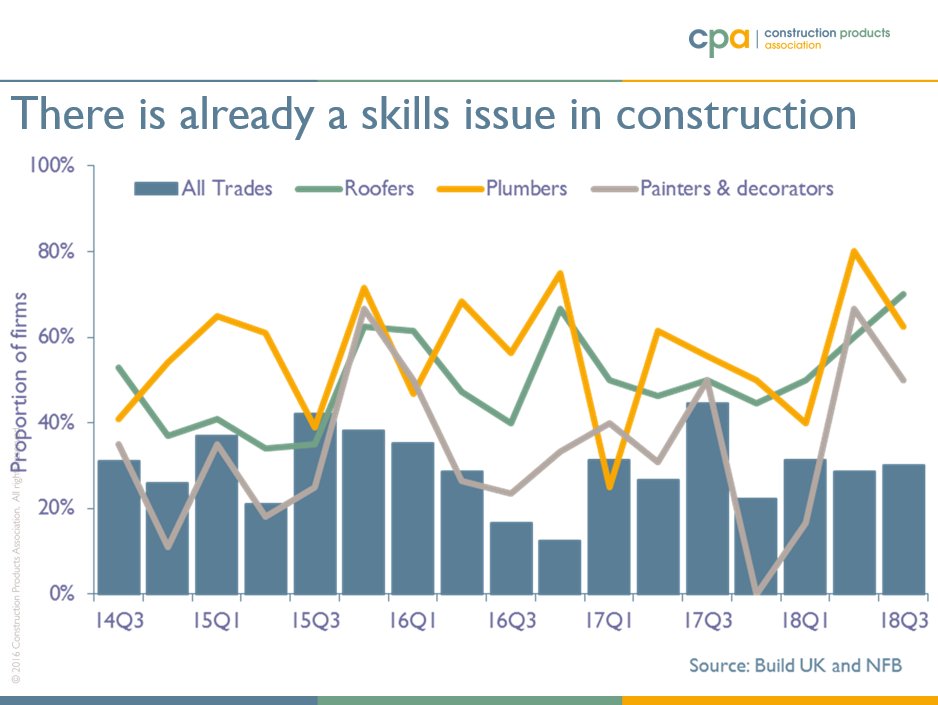

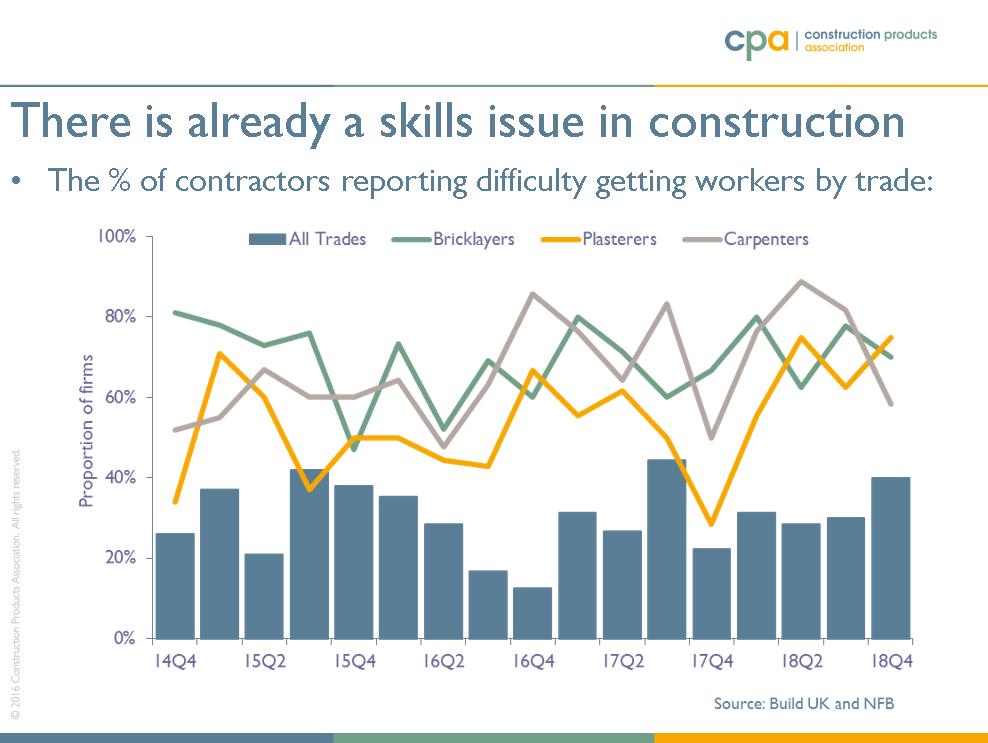

In terms of construction labour, there already is a skills availability issue in construction & it's a long-standing issue that was there before Brexit & will be there whatever type of Brexit there is...

#ukconstruction

#ukconstruction

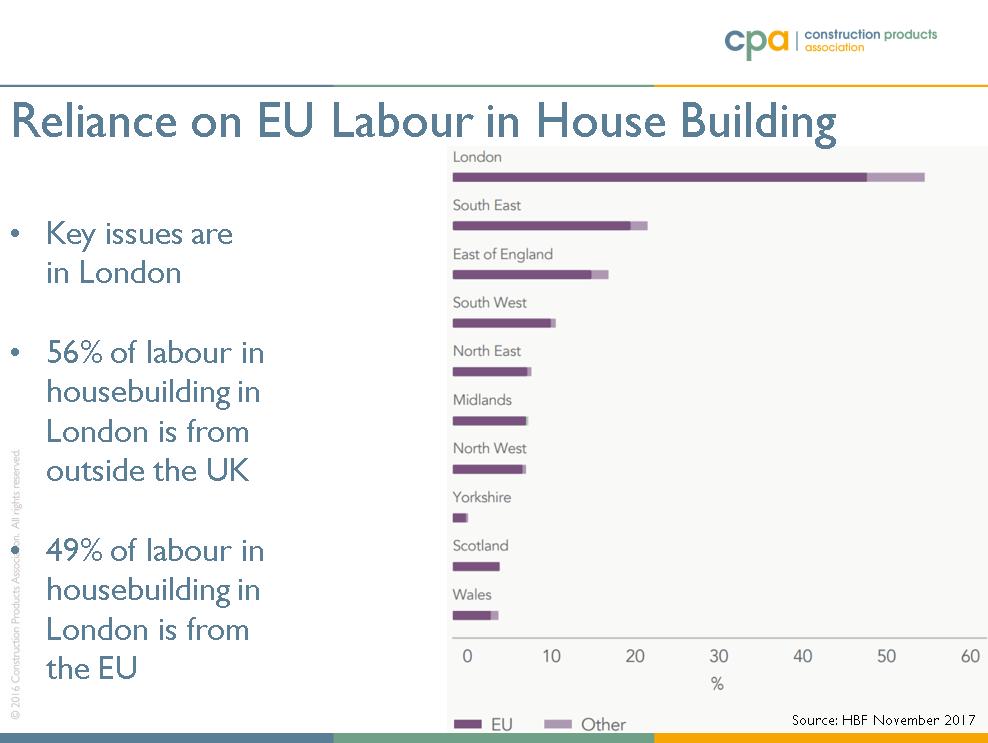

...but there is also a high reliance on EU construction labour, particularly in London, at a time of low domestic unemployment. Brexit & restricting the flow of workers will have impacts labour costs & project viability....

#ukconstruction #brexit

#ukconstruction #brexit

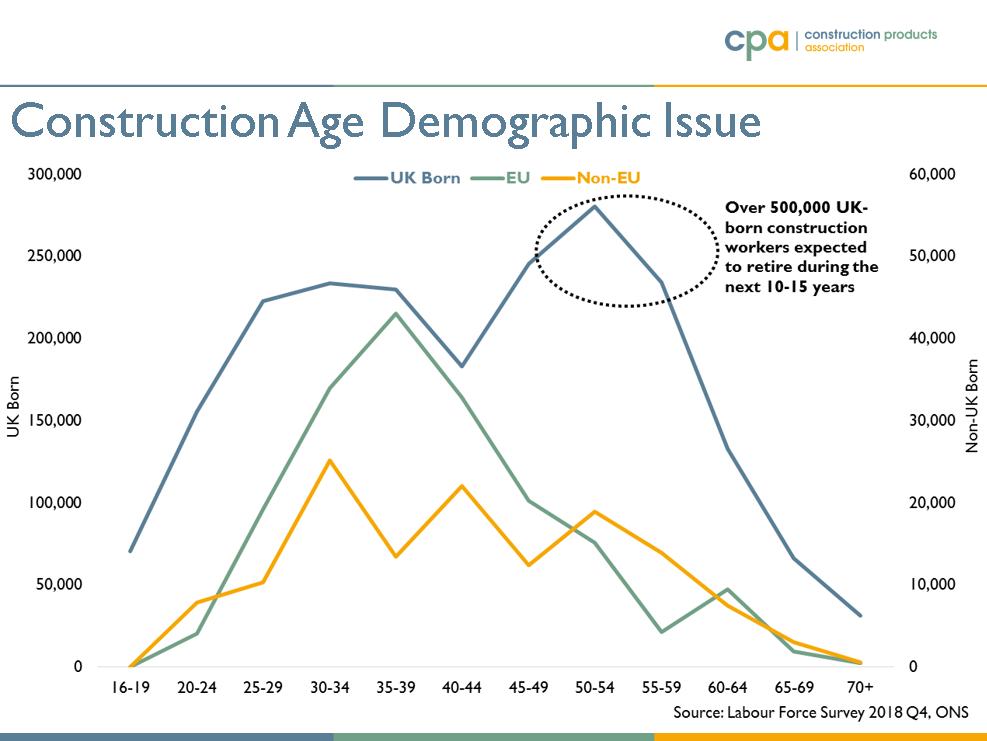

... especially given that the UK-born construction labour force has a demographic issue, with the big 'spike' being the 50-60 age group so this will have great impacts in the next decade once they retire.

#ukconstruction #brexit

#ukconstruction #brexit

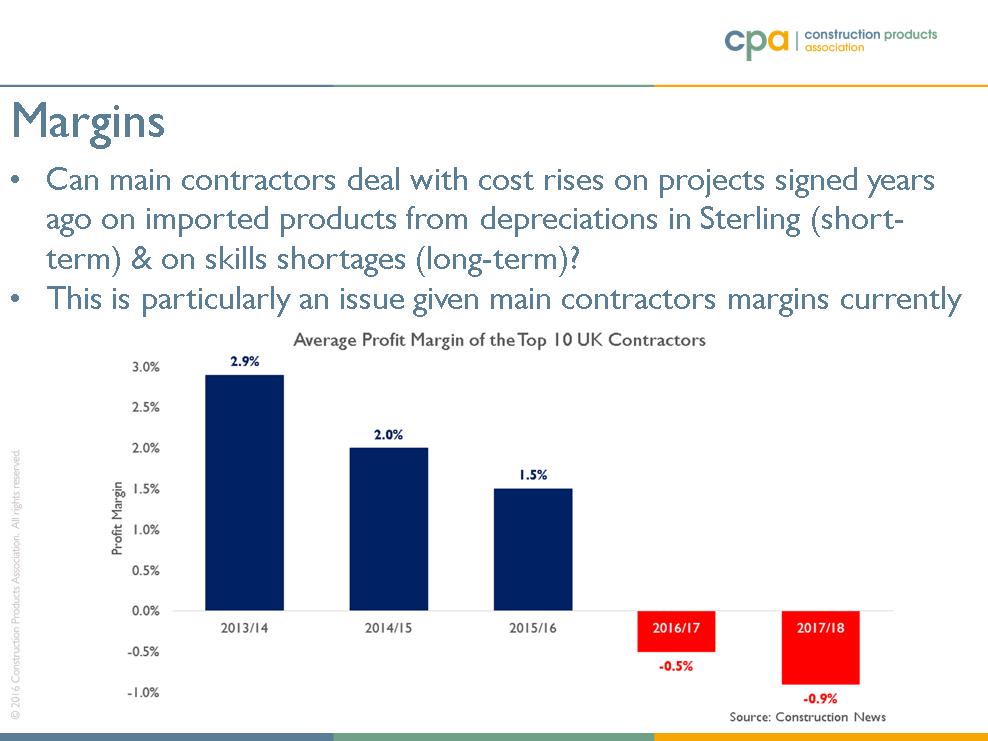

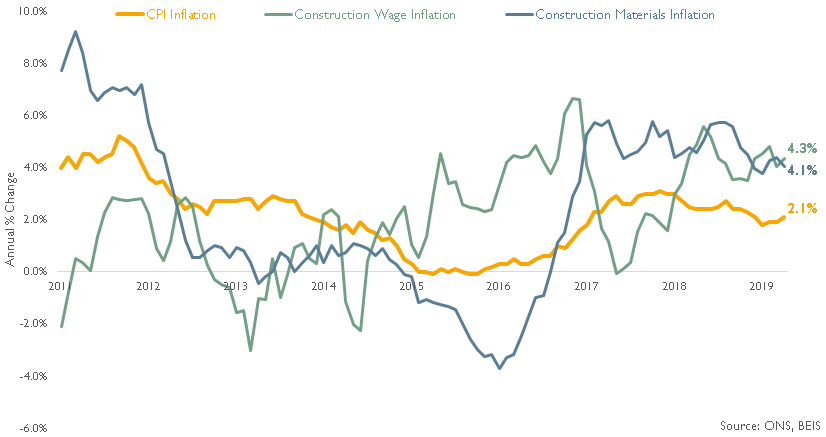

It's worth noting finally that sharp rises in labour & construction materials/products costs will be difficult for construction firms to deal with given that materials & wages inflation is already double CPI inflation...

#ukconstruction

#ukconstruction

...particularly for main contractors given that they are often working on long-term projects signed years ago & are already suffering low/negative margins (despite six consecutive years of growth in construction activity).

#ukconstruction

#ukconstruction