I wrote a quick reaction to the 2020 methodology "discussion document" that #USS released yesterday, but I didn't go into detail on the claims I made. Allow me to do some of that in a thread now. 1/

medium.com/ussbriefs/the-…

medium.com/ussbriefs/the-…

There are three main problems I identified in #USS's document:

1. The dual-discount rate they illustrate is a very close match for their old methodology;

2. Test 1 has been replaced by Test 1 v2.0;

3. We are still hitting a brick wall when it comes to evidence.

2/

1. The dual-discount rate they illustrate is a very close match for their old methodology;

2. Test 1 has been replaced by Test 1 v2.0;

3. We are still hitting a brick wall when it comes to evidence.

2/

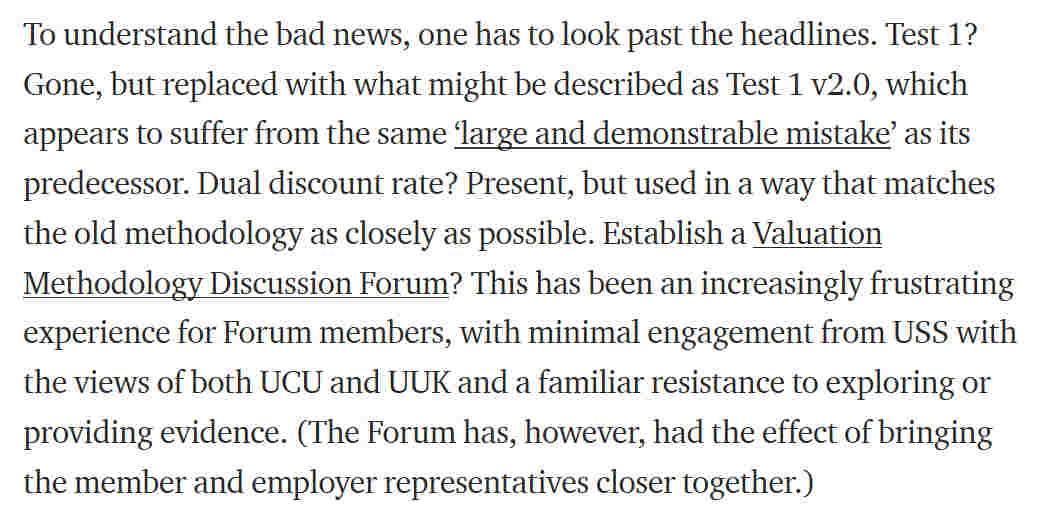

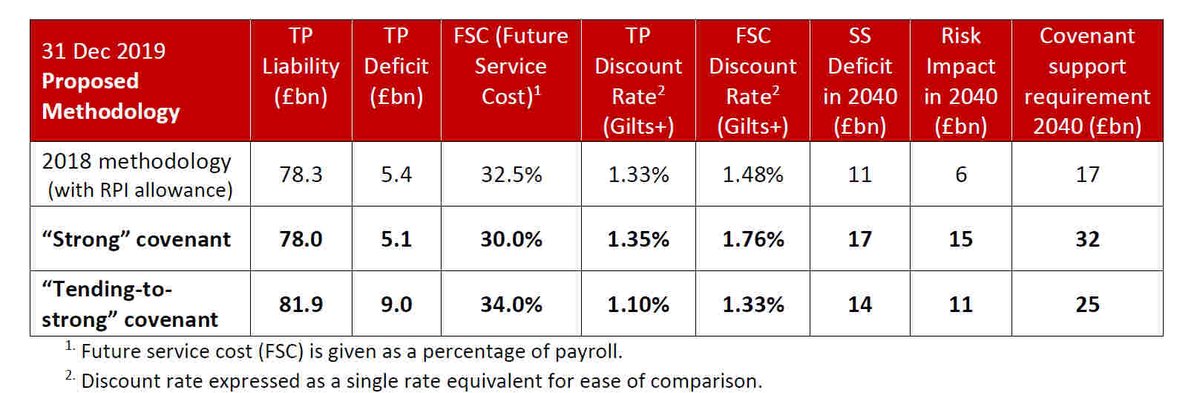

Let's start with the easy one: the dual discount rate that #USS is considering is (at best) equivalent to the 2018 valuation in terms of the calculation of liabilities. This is evident in Table 7.2 of the document (compare the deficits and TP discount rates in rows 1 and 2). 3/

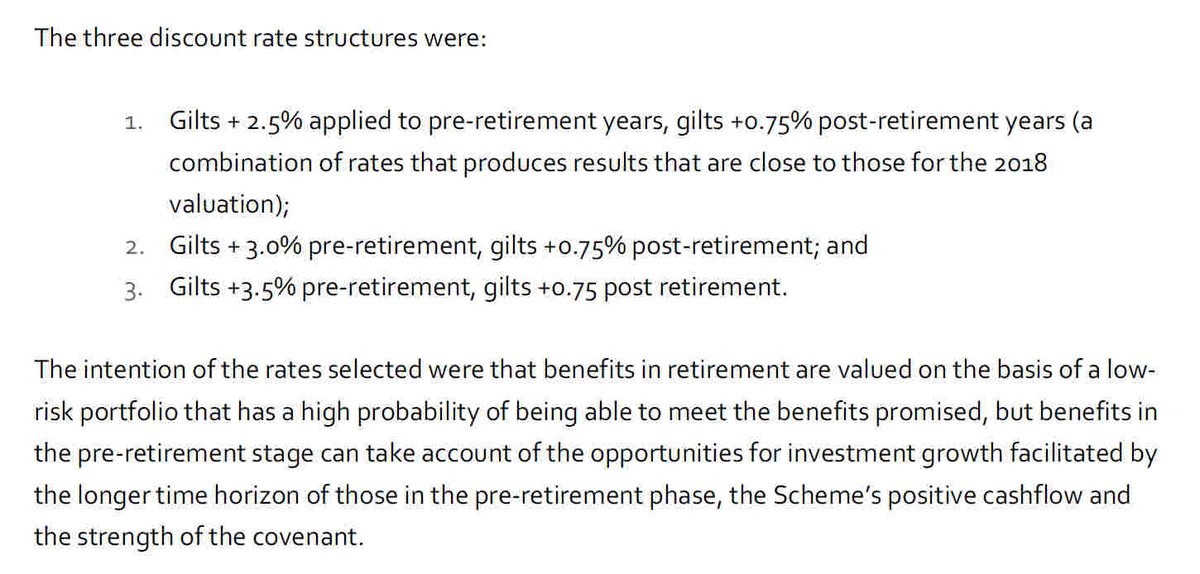

The Joint Expert Panel already pointed out this similarity. Row 2 is based on a pre-retirement discount rate of gilts+2.5% (post-retirement gilts+0.75%), which JEP described as "a combination of rates that produces results that are close to those for the 2018 valuation". 4/

The JEP elaborated further on gilts+2.5%/gilts+0.75%, saying this combination was at or below the upper quartile for other recently valued DB schemes. That is, on this basis #USS (uniquely strong in many ways) would be more prudently valued than over a quarter of schemes. 5/

Here's that table again. Note also row 3, which is what #USS plan to do if they can't get agreement from employers to tie themselves to the scheme indefinitely. This is way beyond what JEP felt fit to illustrate. 6/

Where the dual-discount rate does make a difference is in the future service costs, where it could (see row 2) reduce them by a couple of percentage points. Note, however, that on the rows shown in that table, deficit recovery payments (+4-6%?) would be added to the figures. 7/

So, in summary: the dual discount rate is in, but used so as to seemlessly move from the old approach to a "new" one.

What about Test 1?

8/

What about Test 1?

8/

#USS claim that they are "replacing 'Test 1' (used for previous valuations) with a 'check' that funding risk remains within appetite". This is disingenuous. What they are proposing seems to still involve an algorithm-driven investment strategy, a la Test 1. 9/

How does it work this time? The details are not clear (note that a similar lack of clarity was what enabled Test 1 to survive for so long). But it seems to go like this (buckle up): 10/

Step 1: establish the 'risk appetite' of employers. #USS illustrate two different figures here: £35bn and £25bn, corrsponding to 10% of salary over 30 or 20 years. This step is exactly the same as for Test 1, but the name 'reliance on covenant' has changed. 11/

Step 2: calculate the self-sufficiency liabilities at Year 20, and subtract the 'risk appetite' calculated in Step 1. (Again, this far we're applying the method of Test 1). This will give us a figure we'll use in Step 3. 12/

Step 3: Any potential investment strategy must satisfy the following requirement: assuming full-funding on a technical provisions basis at Year 20 (hello 'large and demonstrable mistake'!), subtracting a 1 in 20 shock must leave the assets no lower than the figure in Step 2. 13/

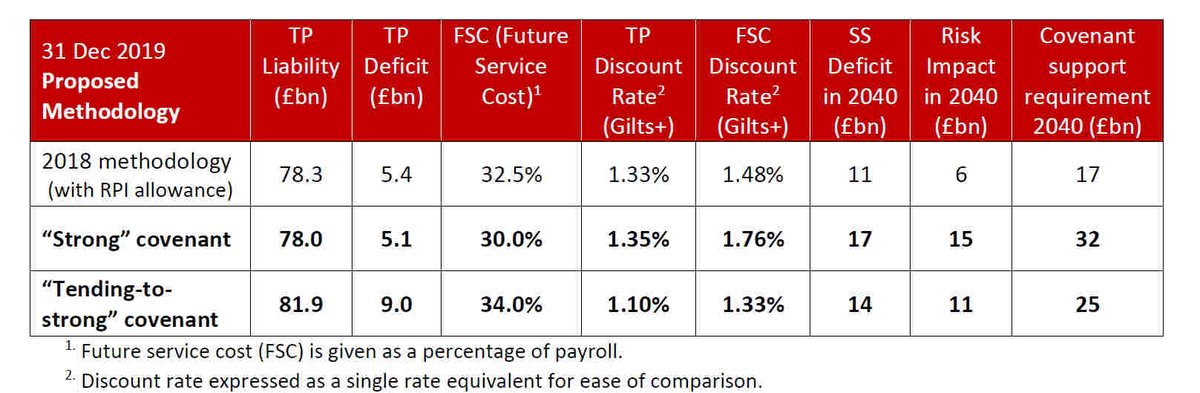

The effect this has on the dual discount rate approach is to 'de-risk' the pre-retirement portfolio (i.e. lower the pre-retirement dicount rate) until the condition in Step 3 is satisfied. Doing this with £35bn gives ~gilts+2.5%, and with £25bn gives ~gilts+0.75%. 14/

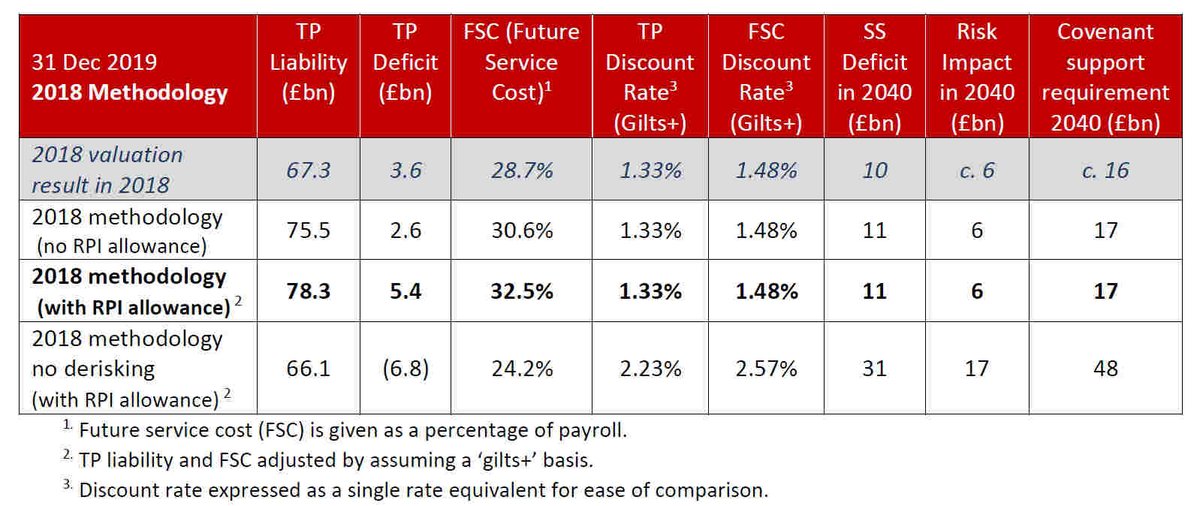

This is not a simple 'check': it forces de-risking. One way to see this is by looking at row 4 of Table 7.1. Here, the 'check' rules out an approach with no de-risking by virtue of the number in the final column being too large. Yet this number is the wrong one to look at! 15/

Note that the large number in the final column of row 4 is due mainly to a large Year 20 self-sufficiency deficit. But this is as a result of the 'large and demonstrable mistake' that #USS keep repeating. 16/

In order to end up with a self-sufficiency deficit of £31bn at Year 20 in the investment strategy corresponding to row 4, one would be paying a basic total rate of just 24.2% AND using the £6.8bn surplus to reduce this rate further. 17/

In other words, the table below does not compare like with like. The assumption of full-funding at Year 20 means that this table is not a sound basis for decisions. We, along with UUK, have repeatedly made this point to #USS at the Valuation Methodology Discussion Forum. 18/

Some of this we are told will follow by mid-March or later. A small amount made it into the document, but marginalised into a hurried appendix, and lacking the level of detail and clarity that would make it useful. 20/

I do not understand how #USS have managed to get away with years of providing substandard anaylsis and resisting calls for clear, unspun evidence (including from one of their own directors, which they later sacked) without any action being taken. 21/

This is now a huge test of our employers. Do you allow this scheme to continue being run in this way, or do you demand improvements? We are all being let down by what's going on within #USS. Just look at the damage it is causing. 22/22

PS: I am pretty sure there are errors in the data in the 'hurried appendix' I mentioned earlier (Appendix A). The table in question is Table A.1 below.

The errors appear to be in the 'Risk Impact' (with yield reversion) column. These numbers are identical to the ones in the tables from Section 7, yet it seems they shouldn't be: a 1 in 20 shock on what will be a bigger asset figure should be bigger.

You could think that this is an easy mistake to make, and I'd agree, except for the fact that an allowance for this increased 'risk impact' was made by the UUK representative who had to create similar figures in his spare time because USS weren't providing them.

The need for this increased risk impact was discussed at the VMDF meeting last week. It seems USS weren't listening. Unless I've missed something, it seems the work being done in people's spare time by UCU and UUK reps is outperforming that done by USS.

PPS I brought this potential error to the attention of USS yesterday lunchtime. No reply.

@threadreaderapp: unroll please!