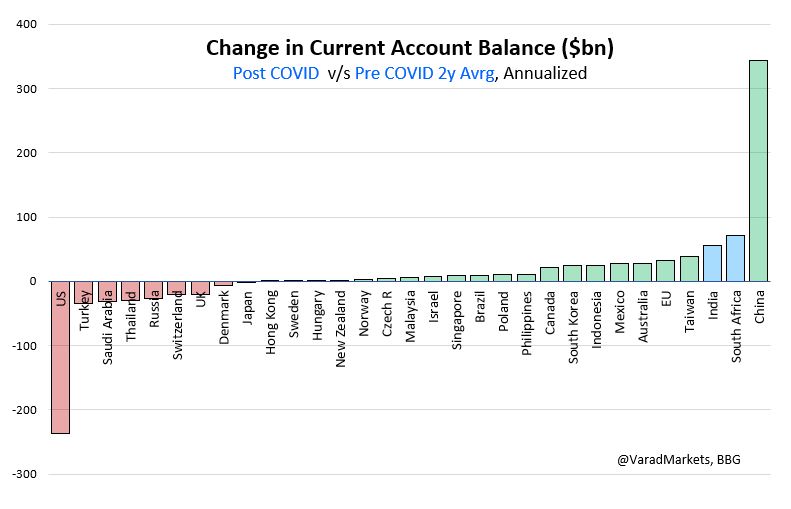

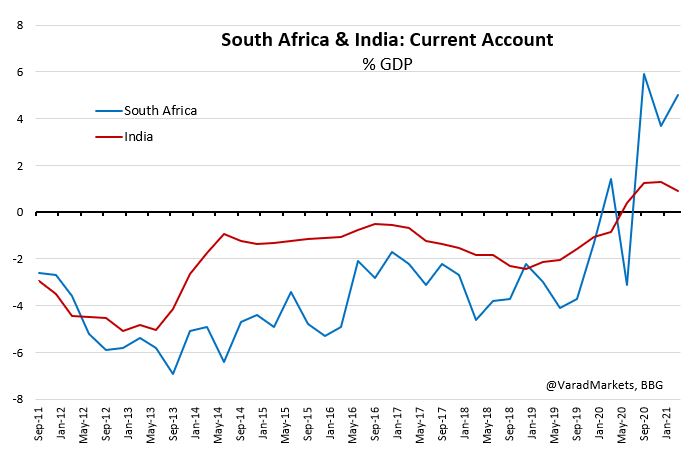

Current Account:

▪️ Few EM countries, led by #SouthAfrica & #India, have flipped to Current Account Surplus largely owing to import compression during COVID growth slowdown

▪️ South Africa feeling less vulnerable while India seems worried about potential capital outflows

1/3

▪️ Few EM countries, led by #SouthAfrica & #India, have flipped to Current Account Surplus largely owing to import compression during COVID growth slowdown

▪️ South Africa feeling less vulnerable while India seems worried about potential capital outflows

1/3

South Africa Central Bank confident; can weather taper tantrum

🔹 Strong Trade balance - additional boost to exports from surge in commodity prices (Platinum, Gold, Iron Ore)

🔹 Lower than expected fiscal deficit

2/3

ft.com/content/872790…

🔹 Strong Trade balance - additional boost to exports from surge in commodity prices (Platinum, Gold, Iron Ore)

🔹 Lower than expected fiscal deficit

2/3

ft.com/content/872790…

▪️ India reluctant to raise rates but significant FX Reserve build up

▪️ In any case, INR more of an Equity ccy than a Bond ccy => raising rates may not attract as much inflows (unlike other high yielders) but may hurt asset valuations leading to outflows

▪️ In any case, INR more of an Equity ccy than a Bond ccy => raising rates may not attract as much inflows (unlike other high yielders) but may hurt asset valuations leading to outflows

https://twitter.com/VaradMarkets/status/1408009666232160258?s=20

• • •

Missing some Tweet in this thread? You can try to

force a refresh