,

28 tweets,

8 min read

Read on Twitter

Charlie Munger, nor I believe that rule to be sensible. Rather, both of us have

consistently thought that at Berkshire this mark-to-market change would produce what I described as “wild and

capricious swings in our bottom line.”

#WarrenBuffet 2018 Letter

consistently thought that at Berkshire this mark-to-market change would produce what I described as “wild and

capricious swings in our bottom line.”

#WarrenBuffet 2018 Letter

Our advice? Focus on operating earnings, paying little attention to gains or losses of any variety. My saying

that in no way diminishes the importance of our investments to Berkshire.

#WarrenBuffet 2018 Letter

that in no way diminishes the importance of our investments to Berkshire.

#WarrenBuffet 2018 Letter

Over time, Charlie and I expect them to

deliver substantial gains, albeit with highly irregular timing.

#WarrenBuffet 2018 Letter

deliver substantial gains, albeit with highly irregular timing.

#WarrenBuffet 2018 Letter

The fact is that the annual change in Berkshire’s book value – which makes its farewell appearance on page

2 – is a metric that has lost the relevance it once had. Three circumstances have made that so.

#WarrenBuffet 2018 Letter

2 – is a metric that has lost the relevance it once had. Three circumstances have made that so.

#WarrenBuffet 2018 Letter

First, Berkshire has

gradually morphed from a company whose assets are concentrated in marketable stocks into one whose major value

resides in operating businesses. Charlie and I expect that reshaping to continue in an irregular manner.

#WarrenBuffet 2018 Letter

gradually morphed from a company whose assets are concentrated in marketable stocks into one whose major value

resides in operating businesses. Charlie and I expect that reshaping to continue in an irregular manner.

#WarrenBuffet 2018 Letter

Second, while

our equity holdings are valued at market prices, accounting rules require our collection of operating companies to be

included in book value at an amount far below their current value, a mismark that has grown in recent years.

#WarrenBuffet 2018 Letter

our equity holdings are valued at market prices, accounting rules require our collection of operating companies to be

included in book value at an amount far below their current value, a mismark that has grown in recent years.

#WarrenBuffet 2018 Letter

Third, it

is likely that – over time – Berkshire will be a significant repurchaser of its shares, transactions that will take place at

prices above book value but below our estimate of intrinsic value.

#WarrenBuffet 2018 Letter

is likely that – over time – Berkshire will be a significant repurchaser of its shares, transactions that will take place at

prices above book value but below our estimate of intrinsic value.

#WarrenBuffet 2018 Letter

The math of such purchases is simple: Each

transaction makes per-share intrinsic value go up, while per-share book value goes down. That combination causes

the book-value scorecard to become increasingly out of touch with economic reality.

#WarrenBuffet 2018 Letter

transaction makes per-share intrinsic value go up, while per-share book value goes down. That combination causes

the book-value scorecard to become increasingly out of touch with economic reality.

#WarrenBuffet 2018 Letter

we expect to focus on Berkshire’s market price. Markets can be

extremely capricious: Just look at the 54-year history laid out on page 2. Over time, however, Berkshire’s stock price

will provide the best measure of business performance.

#WarrenBuffet 2018 Letter

extremely capricious: Just look at the 54-year history laid out on page 2. Over time, however, Berkshire’s stock price

will provide the best measure of business performance.

#WarrenBuffet 2018 Letter

let me remind you of our prime goal in the deployment of your capital: to buy ably-managed businesses, in whole or part, that possess favorable and durable economic

characteristics. We also need to make these purchases at sensible prices.

#WarrenBuffet 2018 Letter

characteristics. We also need to make these purchases at sensible prices.

#WarrenBuffet 2018 Letter

Abraham Lincoln once posed the question: “If you call a dog’s tail a leg, how many legs does it have?” and

then answered his own query: “Four, because calling a tail a leg doesn’t make it one.” Abe would have felt lonely on

Wall Street.

then answered his own query: “Four, because calling a tail a leg doesn’t make it one.” Abe would have felt lonely on

Wall Street.

Warren Buffett on..

stock-based compensation shouldn’t be

counted as an expense. (What else could it be – a gift from shareholders?) And restructuring expenses?

stock-based compensation shouldn’t be

counted as an expense. (What else could it be – a gift from shareholders?) And restructuring expenses?

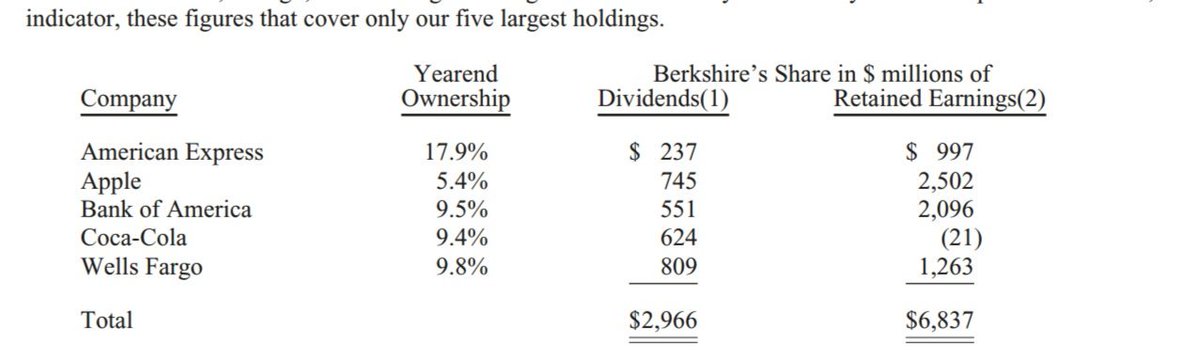

Retained Earnings is more than Dividends

Buffett on...

1) Guard against external calamitie.

2) Will never risk getting caught short of cash.

Learnings for Corporate America and Corporate India... like Reliance ADAG @Moneylifers

1) Guard against external calamitie.

2) Will never risk getting caught short of cash.

Learnings for Corporate America and Corporate India... like Reliance ADAG @Moneylifers

My expectation of more stock purchases is not a market call. Charlie and I have no idea as to how stocks will

behave next week or next year. Predictions of that sort have never been a part of our activities.

behave next week or next year. Predictions of that sort have never been a part of our activities.

Our thinking, rather,

is focused on calculating whether a portion of an attractive business is worth more than its market price.

Buffett Investment Philosophy

is focused on calculating whether a portion of an attractive business is worth more than its market price.

Buffett Investment Philosophy

You may ask whether an allowance should not also be made for the major tax costs Berkshire would incur if

we were to sell certain of our wholly-owned businesses.

we were to sell certain of our wholly-owned businesses.

Forget that thought: It would be foolish for us to sell any of

our wonderful companies even if no tax would be payable on its sale. Truly good businesses are exceptionally hard to

find. Selling any you are lucky enough to own makes no sense at all.

our wonderful companies even if no tax would be payable on its sale. Truly good businesses are exceptionally hard to

find. Selling any you are lucky enough to own makes no sense at all.

Berkshire’s value is maximized by our having assembled the

five groves into a single entity. This arrangement allows us to seamlessly and objectively allocate major amounts of

capital, eliminate enterprise risk, avoid insularity, fund assets at exceptionally low cost.

five groves into a single entity. This arrangement allows us to seamlessly and objectively allocate major amounts of

capital, eliminate enterprise risk, avoid insularity, fund assets at exceptionally low cost.

Obviously, repurchases should be price-sensitive: Blindly buying an overpriced stock is value-

destructive, a fact lost on many promotional or ever-optimistic CEOs.

destructive, a fact lost on many promotional or ever-optimistic CEOs.

The areas of bad corporate behaviour..

1) Trade-loading at quarter-end,

2) Turning a blind eye to rising insurance losses, or

3)Drawing

down a “cookie-jar” reserve –

1) Trade-loading at quarter-end,

2) Turning a blind eye to rising insurance losses, or

3)Drawing

down a “cookie-jar” reserve –

That record is no accident: Disciplined risk evaluation is the daily focus of our insurance managers, who know that the benefits of float can be drowned by poor underwriting results. All insurers give that message lip service.

At Berkshire it is a religion, Old Testament style.

At Berkshire it is a religion, Old Testament style.

As I have often done before, I will emphasize that this happy outcome is far from a sure thing:

"Usually Win, Occassionally Die"

"Usually Win, Occassionally Die"

What we see in our holdings, rather, is an assembly of companies that we partly own and that, on a wtd

basis, are earning about 20% on the net tangible equity capital required to run their businesses. These comp, also,

earn their profits without employing excessive levels of debt

basis, are earning about 20% on the net tangible equity capital required to run their businesses. These comp, also,

earn their profits without employing excessive levels of debt

On March 11th, it will be 77 years since I first invested in an American business. The year was 1942, I was

11, and I went all in, investing $114.75 I had begun accumulating at age six. What I bought was three shares of Cities

Service preferred stock. I had become a capitalist,

11, and I went all in, investing $114.75 I had begun accumulating at age six. What I bought was three shares of Cities

Service preferred stock. I had become a capitalist,

Over the next 77 years, however, the major source of our gains will almost certainly be provided by The

American Tailwind. We are lucky – gloriously lucky – to have that force at our back.

American Tailwind. We are lucky – gloriously lucky – to have that force at our back.

For 54 years, Charlie and I have loved our jobs. Daily, we do what we find interesting, working with people

we like and trust. And now our new management structure has made our lives even more enjoyable.

we like and trust. And now our new management structure has made our lives even more enjoyable.

@ThreadReaderApp unroll