,

52 tweets,

16 min read

Read on Twitter

Live tweeting the Stern Household Finance conference!

Thanks to @stroebel_econ and Theresa Kuchler for organizing

Thanks to @stroebel_econ and Theresa Kuchler for organizing

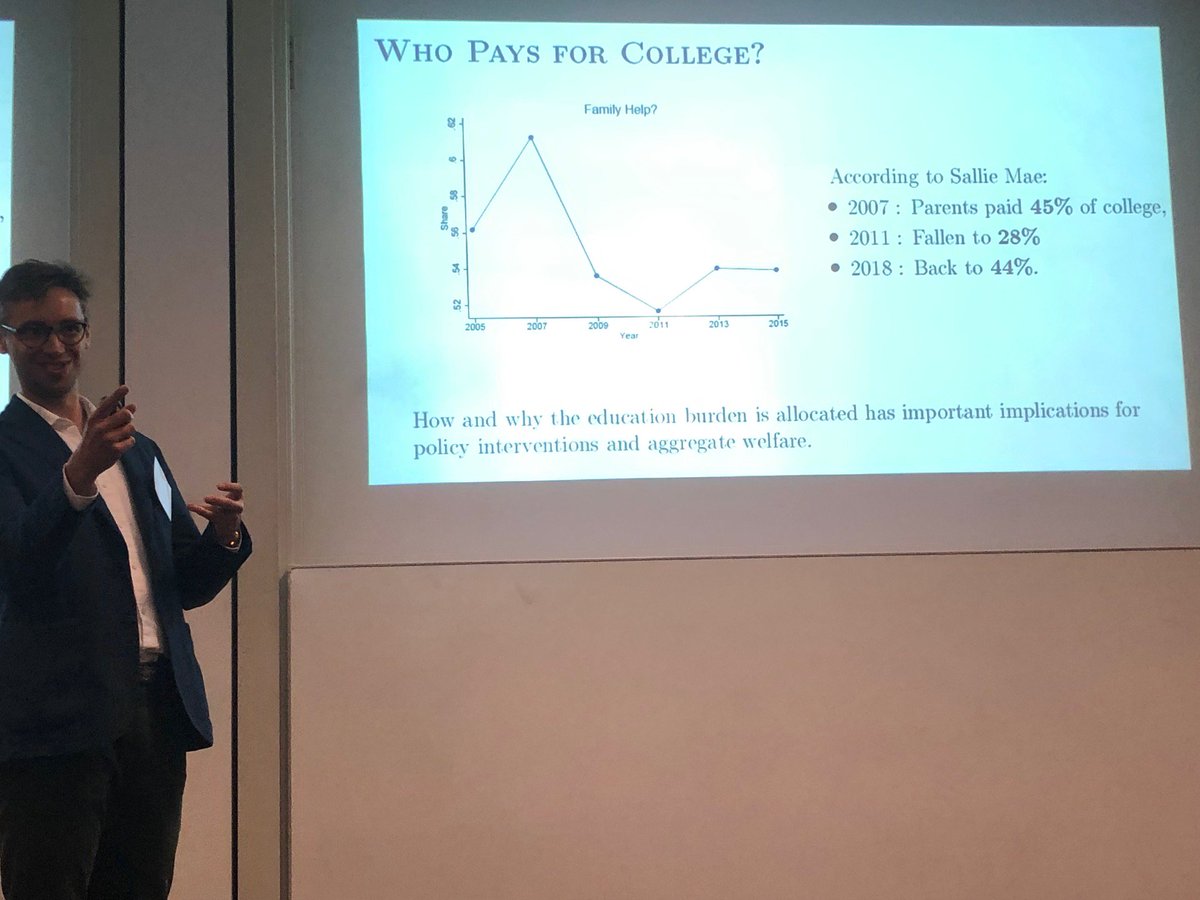

First up @Kutbil_Ik with Janice Eberly and Gene Amromin on a somewhat informatively titled paper: "Who Pays for College? The Effect of Liquidity Constraints and Student Loans"

Document that parental support for children varies with housing cycles

Document that parental support for children varies with housing cycles

Adds to long literature on how collateralized borrowing in real estate is special in allowing households to borrow much more, for lower interest rates, than uncollateralized lending.

Student loans also special, since not dischargeable in bankruptcy.

Student loans also special, since not dischargeable in bankruptcy.

Households that are more constrained in equity extraction take out less equity.

This doesn't affect college enrollment (interesting and well pitched null), but changes financing. Students take on more student loans. Parents spend more out of pocket.

This doesn't affect college enrollment (interesting and well pitched null), but changes financing. Students take on more student loans. Parents spend more out of pocket.

Argument by "look at my fixed effects."

Interesting inter-generational conflict here. Less housing wealth by parents -> more debt burden for children -> less burden for parents.

Next: @rebeccardiamond presenting "The Consequences of Housing Foreclosure for Owners, Renters, and Landlords"

Very nice paper on understanding causal effects of foreclosure on owners, renters, and landlords.

Very nice paper on understanding causal effects of foreclosure on owners, renters, and landlords.

Uses randomization of foreclosure judges in Cook county. Similar identification as in a paper by Munroe and Laurence Wilse-Samson (columbia.edu/~lhw2110/dm_lw…); or eviction judges in Cook county (johnerichumphries.com/Evictions_draf…).

Either judges allow foreclosure judgement (leads to foreclosure). If not, borrowers have more latitude to go through a short sale or other transaction; or else modification if they can't pursue the foreclosure.

Amazing data work here; using the very cool Infutor dataset (individual address history) matched with court records, deeds records, etc.

Foreclosure for owners leads to:

- smaller homes

- worse neighborhoods on income and intergenerational mobility

- higher divorce rates (15 percentage points!)

But not as bad for renters, or landlords.

-> Suggests the financial shock *and* eviction shock together is bad

- smaller homes

- worse neighborhoods on income and intergenerational mobility

- higher divorce rates (15 percentage points!)

But not as bad for renters, or landlords.

-> Suggests the financial shock *and* eviction shock together is bad

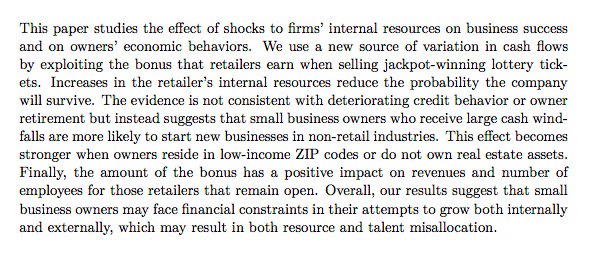

Jacelly Cespedes, Xing Huan, Carlos Parra: "More Cash Flows, More Options? The Effect of Cash Windfalls on Small Firms"

stern.nyu.edu/sites/default/…

Retailers that sell jackpot ticket -> get bonus -> affects firm decisions

stern.nyu.edu/sites/default/…

Retailers that sell jackpot ticket -> get bonus -> affects firm decisions

Similar to many papers using lotteries as windfall gains, my favorite of these include this work by David Cesarini and co-authors. Here on lottery winnings leading to more happiness (nber.org/papers/w24667).

Also see this @ProfEmilyOster paper (College thesis I think?) on how larger-stake lotteries are more progressive.

So you would in general think that more cash is good, but it turns out that retail owners close the business and start a new one in a different industry instead, often restaurants, which require initial capital.

The dog that did not bark: no lottery ticket sales in Las Vegas.

So these small, retail establishments selling lottery tickets are something like "gateway" entrepreneurs doing not a great business. But when they do well, they move on to possibly more value-add entrepreneurship.

Next: Constantine Yannelis and Holger Mueller

stern.nyu.edu/sites/default/…

On another topical student loan question: Income Based Repayment plans!

stern.nyu.edu/sites/default/…

On another topical student loan question: Income Based Repayment plans!

These plans are interesting by offering more implicit insurance to borrowers in times of poor income realizations. Australia uses them a fair amount; various schools have tried them in the US (Yale Law for President Clinton I believe); but credibility of repayment is issue.

This paper tests the take-up of these Income Repayment plans. Fits into this growing literature testing optimization frictions around program takeup, as in this nice paper by Amy Finkelstein and @ProfNoto (economics.mit.edu/files/15053). Here, randomized trial by a loan servicer.

The complexity of filling out these documents (do you want to fill this form out) seems sufficient to deter people from signing up for income repayment plans. Here, servicer pre-filled form for them.

Taking up the income repayment plans

- lower monthly payments

- basically eliminate loan delinquencies

- consumer more instead

- lower monthly payments

- basically eliminate loan delinquencies

- consumer more instead

What I think is most interesting is that the compliers, marginal people who take up the income-based plans, have low income ex post. Consistent with:

- moral hazard. work less, due to higher implicit marginal tax rates of income repayment plans

- moral hazard. work less, due to higher implicit marginal tax rates of income repayment plans

- OR, adverse selection. Borrowers who know they have greater income risk in future most likely to take up the plans.

Either case presents important potential frictions which may make income repayment plans work less well in general.

Either case presents important potential frictions which may make income repayment plans work less well in general.

Providing this insurance value to student borrowers would be nice; and lowering paperwork complexity is convenient way.

But as with any insurance plan some tricky hidden information/hidden action issues which would be great to see explored in future.

But as with any insurance plan some tricky hidden information/hidden action issues which would be great to see explored in future.

Job talk session:

Stephanie Johnson, "Mortgage Leverage and House Prices"

stern.nyu.edu/sites/default/…

Stephanie Johnson, "Mortgage Leverage and House Prices"

stern.nyu.edu/sites/default/…

It's been a recent focus of many people, such as in @ProfGreenwald's JMP (dlgreenwald.com/uploads/4/5/2/…); to look at payment-to-income constraints as a determinant of lending decisions.

Relevant for macro prudential policy as well, as in Stephanie's work with @Kutbil_Ik and @AnthonyDeFusco (files.consumerfinance.gov/f/documents/Pa…)

Here, exploiting this very nice DTI limit, resulting from adoption of desktop underwriting software, that applied to Freddie loans (relative to Fannie).

This sort of discontinuity is what we live for, we simple empirical household finance folk.

This sort of discontinuity is what we live for, we simple empirical household finance folk.

Credit constraints -> less lending -> house prices fall.

Reinforces idea that credit constraints, a key part of which is governed by payment size relative to flow income, pass through to house prices.

Reinforces idea that credit constraints, a key part of which is governed by payment size relative to flow income, pass through to house prices.

Payments has seen pretty interesting innovation in many developing countries. Think mobile money in Kenya (cnn.com/2017/02/21/afr…); or bank-account linked payments in India (en.wikipedia.org/wiki/JAM_Yojana).

Here, Mexican gov giving out debit cards.

Here, Mexican gov giving out debit cards.

Retailers (corner stores) took cards more often, which makes sense.

But then *other* consumers, not affected, also got cards -- a result of the network externalities in card payment technology.

But then *other* consumers, not affected, also got cards -- a result of the network externalities in card payment technology.

When Uber comes to town, people get auto loans to drive; less so if credit frictions apply.

Interesting to me -- rich people *still* buy cars, just use their own car less. So overall auto usage way up. Need congestion pricing for ride sharing to be sensible.

Interesting to me -- rich people *still* buy cars, just use their own car less. So overall auto usage way up. Need congestion pricing for ride sharing to be sensible.

Interesting boundary of firm questions. Should firm buy auto stock, or hire freelancers that are borrowing on their own credit?

+ view: leaves people with more assets, takes advantage of changing tech and frictions

- view: also leaves people with debt

+ view: leaves people with more assets, takes advantage of changing tech and frictions

- view: also leaves people with debt

2005 Bankruptcy Reform in Brazil (good year to reform bankruptcy) which improved creditor protections (previously very low recoveries in bankruptcy) and led to more borrowing capacity.

Increase employment, especially of *skilled* workers, suggesting capital-skill complementarity

Increase employment, especially of *skilled* workers, suggesting capital-skill complementarity

I would be interested to see: did this lead to *ex ante* greater human capital investment to acquire skills that are now valued, when financial constraints are not as binding?

Chile reduced interest rate caps by 20 percentage points. While this kind of price regulation might be potentially valuable to restrict "over borrowing"; here find:

- redistribution across borrowers

- substantial rationing, many fewer loans

- lots of bunching at new limit

- redistribution across borrowers

- substantial rationing, many fewer loans

- lots of bunching at new limit

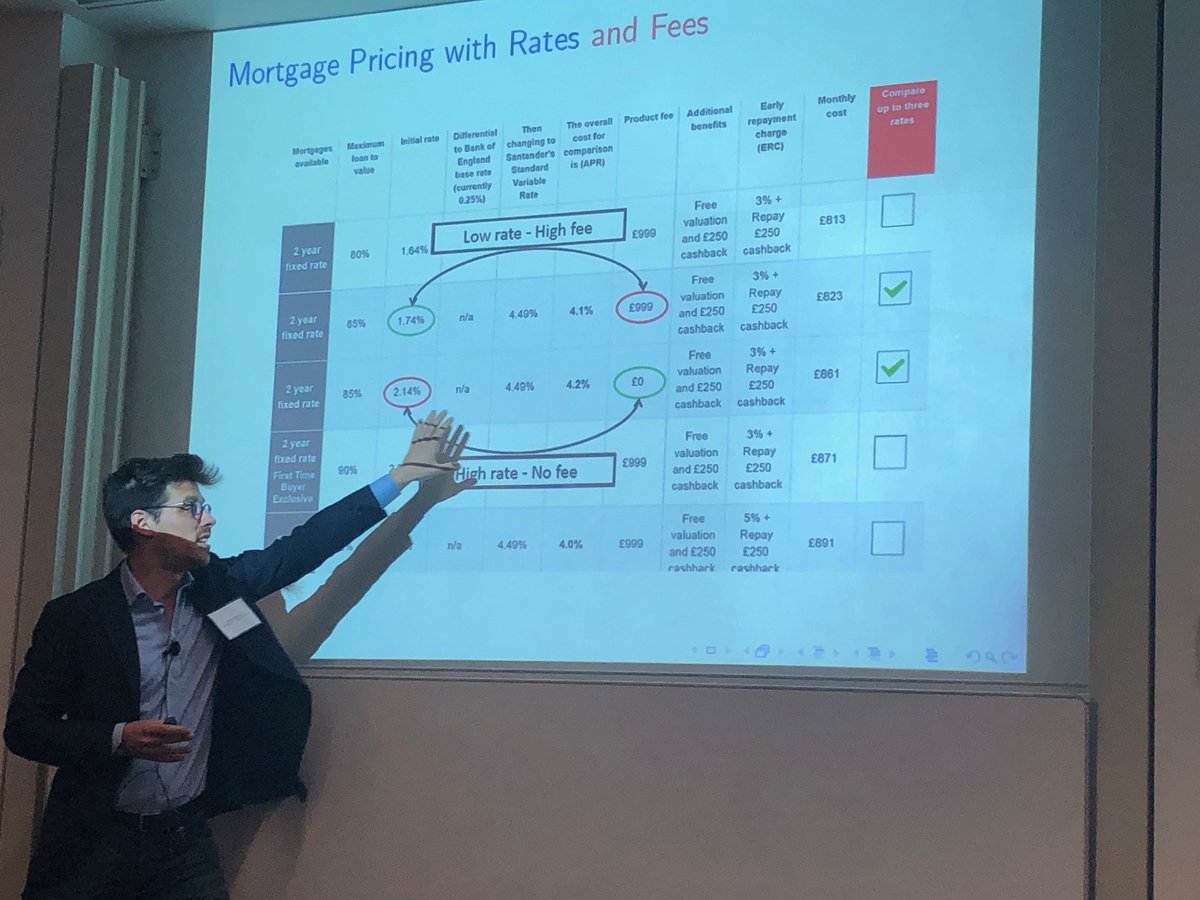

Next: @m_benetton "Mortgage Pricing and Monetary Policy"

We have two sets of regulatory bodies. Macro policies often oriented at increasing credit and lending. And micro regulators (such as the CFPB), who are often trying to lower lending on the grounds that borrowers are irrational/imperfectly informed etc.

The UK has a cool mortgage market; in which borrowers typically have what we would call "Hybrid ARMs" in the US. Short-term fixed rate, then reset to a variable interest rate (at which point people typically refinance personal.lse.ac.uk/ilzetzki/index…).

Mortgages have fees, which tend to be negatively correlated with interest rates. While interest rates go up with LTVs (risk), the fee does not (extracting surplus).

After the UK instituted Funding for Lending facility - lower interest rate pass through; but higher fees.

If you do both unconventional monetary policy and shut down ability of lenders to impose fees; reduces the market power of lenders. So monetary policy is even more effective; most passthrough of interest rates

Or -- lenders setting some fees that reduces effect of these policies

Or -- lenders setting some fees that reduces effect of these policies

Last! @paulgp on "Medicare and the geography of financial health" with Maxim Pinkovskiy and Jacob Wallace

Motivating graph: states which have higher near-elderly uninsurance rates have higher debt collection rates, as a proxy for financial distress

People get Medicare at age 65...

And then they have much less debt in collections (as measured by annual flow), which is mostly dominated by medical debts. Bigger change in places that had greater elderly uninsurance rates.

There is a nice state border strategy here to isolate the pure effects of state policy, as opposed to other sorting mechanisms of individuals across states. Suggests large variation in financial health outcomes across states is due to state health insurance policies.