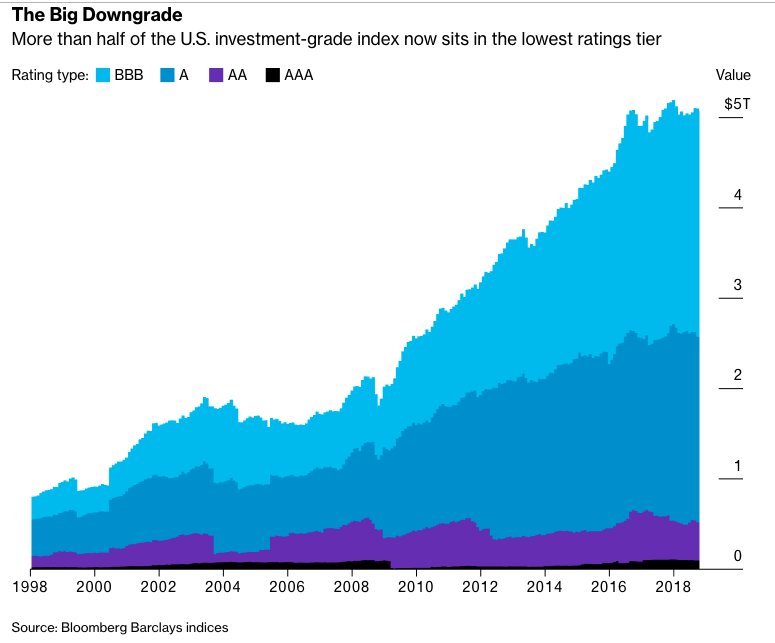

@dandolfa @arindube @1954swilliamson @gabriel_mathy @teasri @IvanWerning @farmerrf @Noahpinion @asymptosis Sure! First, here is aggregate corporate debt

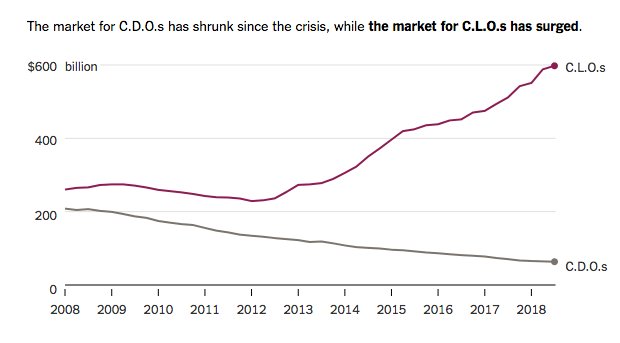

The riskier stuff consists of levered loans -- adjustable interest rate, low covenant protection -- and often securitized in CLOs (now CLO-squared too wsj.com/articles/hedge…)

The riskier stuff consists of levered loans -- adjustable interest rate, low covenant protection -- and often securitized in CLOs (now CLO-squared too wsj.com/articles/hedge…)

@dandolfa @arindube @1954swilliamson @gabriel_mathy @teasri @IvanWerning @farmerrf @Noahpinion @asymptosis This CLO market has grown a ton recently, assisted by their removal from risk-retention requirements

nytimes.com/2018/10/19/bus…

nytimes.com/2018/10/19/bus…

@dandolfa @arindube @1954swilliamson @gabriel_mathy @teasri @IvanWerning @farmerrf @Noahpinion @asymptosis To be fair, this stuff is commonly seen as safer and did not default much, even through crisis.

But the stuff we have today has the potential to be different. For one - the weak covenants can enable asset tunneling

bloomberg.com/news/articles/…

But the stuff we have today has the potential to be different. For one - the weak covenants can enable asset tunneling

bloomberg.com/news/articles/…

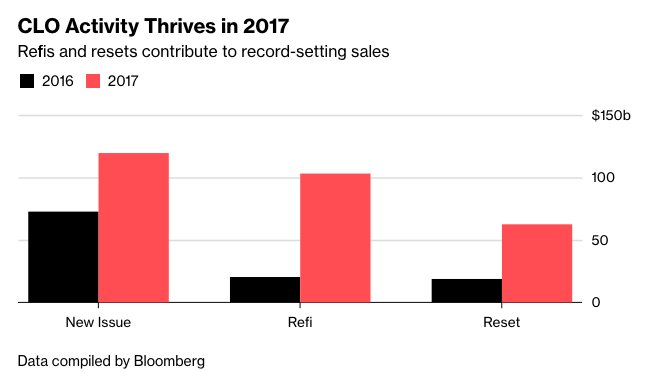

@dandolfa @arindube @1954swilliamson @gabriel_mathy @teasri @IvanWerning @farmerrf @Noahpinion @asymptosis Additionally there is this new "reset" market which is basically perma-refinancing of loans and so is vulnerable to market shutdown

bloomberg.com/markets/fixed-…

bloomberg.com/markets/fixed-…

@dandolfa @arindube @1954swilliamson @gabriel_mathy @teasri @IvanWerning @farmerrf @Noahpinion @asymptosis "Mark-to-market losses could spur fund redemptions, induce fire sales and further depress prices. These dynamics may affect not only investors holding these loans, but also the broader economy by blocking the flow of funds to the leveraged credit market."

ftalphaville.ft.com/2018/10/19/153…

ftalphaville.ft.com/2018/10/19/153…

@dandolfa @arindube @1954swilliamson @gabriel_mathy @teasri @IvanWerning @farmerrf @Noahpinion @asymptosis So holding structure can be risky if held by mutual funds (or potentially in this $.5t "liquidity fund" sector - regulatory arbitrage to not be classified as MMMF)

Or debt fund. Here is an example in commercial mortgages, a PIMCO fund holding with repo

psers.pa.gov/About/Board/Re…

Or debt fund. Here is an example in commercial mortgages, a PIMCO fund holding with repo

psers.pa.gov/About/Board/Re…

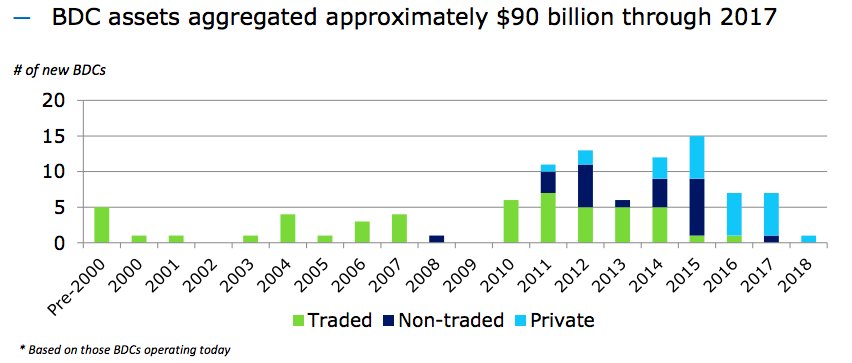

@dandolfa @arindube @1954swilliamson @gabriel_mathy @teasri @IvanWerning @farmerrf @Noahpinion @asymptosis There is another $100b or so of debt, often spun off from PE acquisitions, held in REIT-like capital market structures called BDCs

Maybe not super huge or risky - but the fact that this sector was 0 pre-crisis highlights the shift in corp lending

publiclytradedprivateequity.com/portalresource…

Maybe not super huge or risky - but the fact that this sector was 0 pre-crisis highlights the shift in corp lending

publiclytradedprivateequity.com/portalresource…