,

11 tweets,

3 min read

Read on Twitter

Since we are getting much Monday morning quarterbacking on Argentina program, it's useful to recall the assumptions that underpinned the Program initiation document. Then we might ask how it ought to have been judged at the time.

For example, ARS was expected to reach about ARS30 by 2020 and the USD value of GDP increase to about USD730bn by 2023.

The current account in USD terms was expected to compress from a deficit of about USD30bn to about USD15bn; in percent of GDP the deficit would settle around 2%. So no external surpluses were expected.

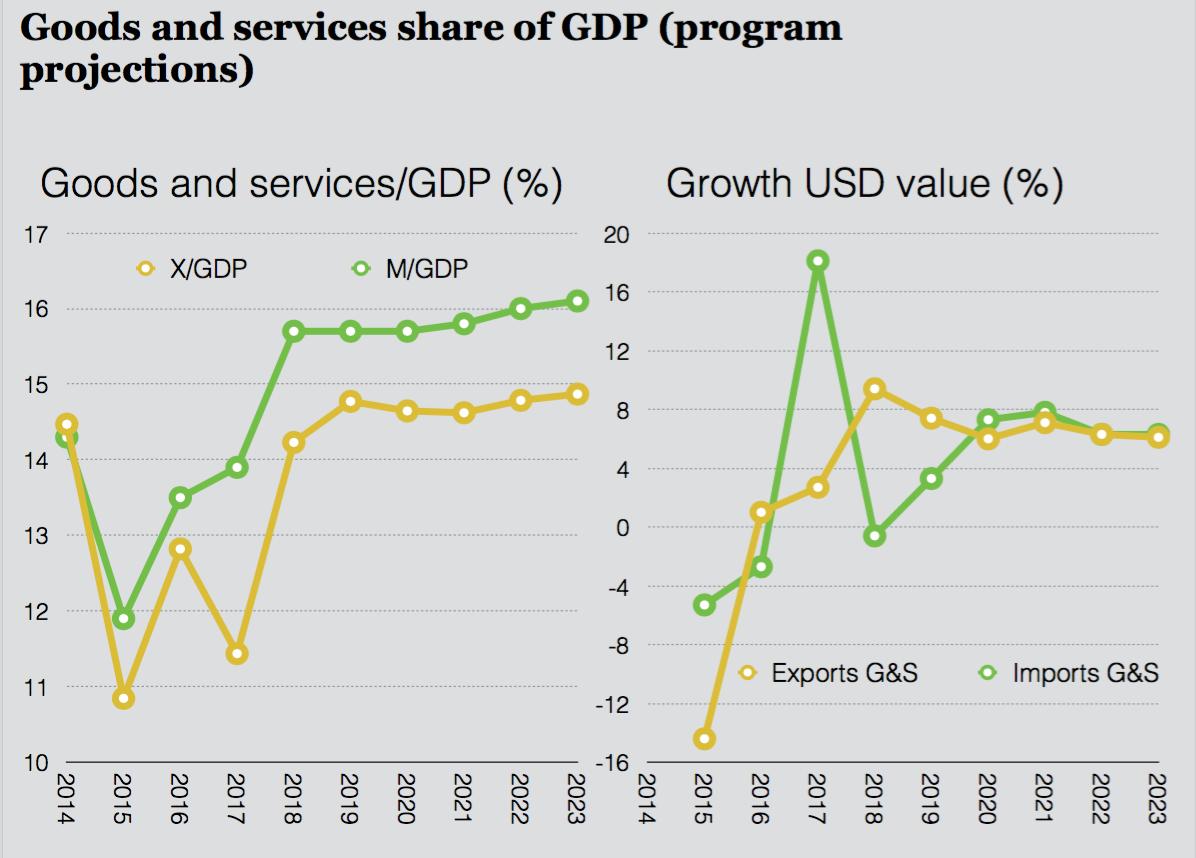

The CA adjustment of 3% of GDP, or USD15bn, was due to the goods balance coming in about USD8bn. But the largest contributor was primary income balance, meaning Argie was expected to earn larger income on external assets or the interest rate it pays abroad was falling.

USD value of imports never turned meaningfully negative, so there was minimal import compression factored in. Export growth was positive throughout.

There was about 4.5% of GDP primary balance adjustment, largely backloaded. The interest balance deteriorated to nearly 4% of GDP by 2022. The relative fiscal-current account adjustment implied private S-I balance was moving from surplus to balance, offsetting austerity.

The different between the external primary balance and the fiscal interest bill in % of GDP is striking. While the external interest balance is improving, the fiscal is deteriorating. (Similar assumptions underpinned the initial Greek program in 2010, FYI.)

External financing assumptions are interesting. Since reserve assets were to increase USD49bn over 6 years, other investment outflows continue, CA deficit financed, and the IMF repaid, there was assumed USD160bn in net private portfolio inflows and USD42bn in FDI.

In other words, there would be huge private capital inflows to continue to finance private investment and consumption, that would also finance the IMF funds and reserve asset accumulation, despite austerity. Moreover, the external interest bill was expected to be shrinking...

All of this is not to mention the fact that central bank was without capital and needed to monetise their interest bill...

The question for those looking at the Argentina program today and postulating about what was the right course of action upon initiation, it's best to begin whether the program assumptions made sense.

I know what I think.

I know what I think.