,

28 tweets,

9 min read

Read on Twitter

You wouldn’t know it from looking at stock market indices, but this week has seen some MASSIVE moves beneath the surface - a “momentum crash” that is eerily reminiscent of the August 2007 quant quake. Here’s my FT take on.ft.com/2AaNqGI but it deserves a full thread. 1/n

Equities have bounced back from the August turbulence, thanks to expectations of central bank easing and a ratcheting down of trade tensions. But think of the stock market as a duck. It seems to be swimming along placidly, but beneath the surface the legs are paddling furiously.

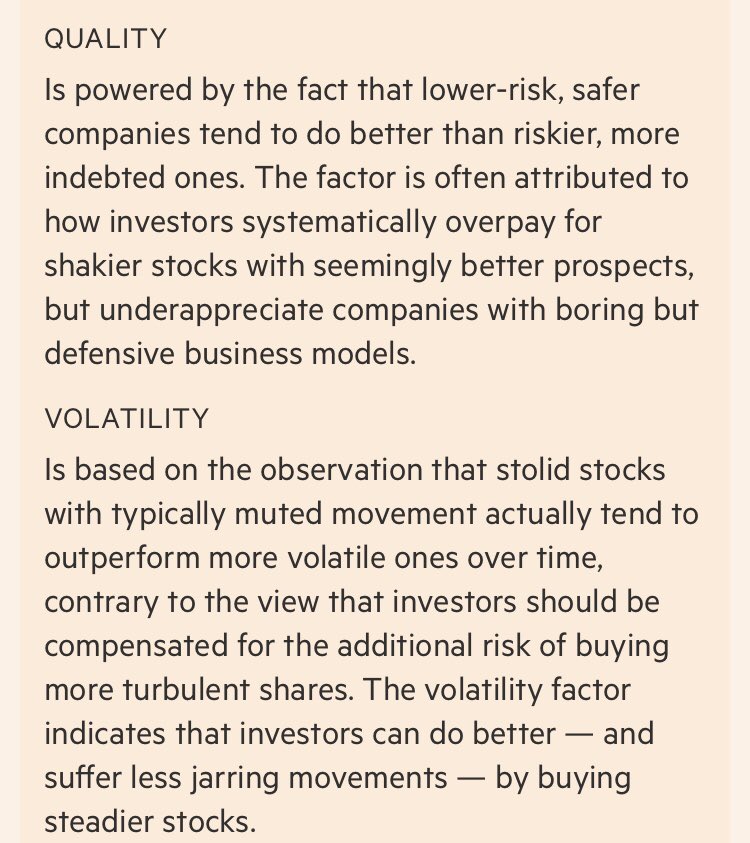

First an explanation of “factors”. Over the years financial academics have unearthed several stock characteristics that seem to generate - over time - better market returns. In theory they are extra returns that you get for accepting a certain risk.

For example, smaller company stocks are generally riskier and more volatile than bigger ones, and in the long run “small caps” have offered greater returns than “large caps”. Here are some nibs on the biggest generally-accepted factors.

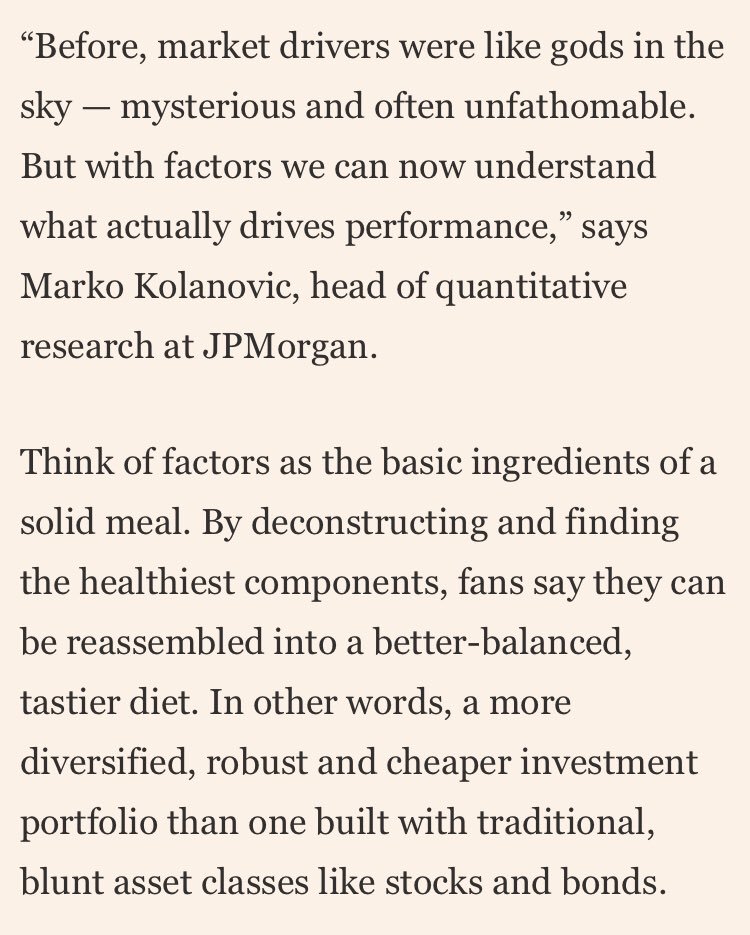

Factors seem weird, definitions differ, and most people still think about the stock market as a group of industries. But I’d argue that nowadays you cannot understand the stock market’s behaviour without also understanding factors. You can read more here on.ft.com/2NWIAVC

Let’s explore momentum a little bit further. Momentum is well-established factor (altho slightly controversial because people still disagree on what driver of it). But much simplified you can actually make money from jumping on securities with the wind in their tail.

David Ricardo, the 18th century economist, first formulated the basic rules as “cut short your losses” and “let your profits run on”, but since then quants have built all sorts of complex models to identify securities with budding momentum, and trade them systematically.

But crucially, factors aren’t static. A company that is small today might be huge in a decade, and a stock powering on might lose its mojo. So factor investors continually rebalance, and one factor can bleed into another. A stock can both be ‘quality’ and ‘momentum’, for example.

ANYWAYS, what happened this week was that momentum got absolutely SMASHED. I don’t mean a Mike Tyson haymaker right in the nose. It’s more like getting hit by a runaway train. Monday was one of the worst days in history for momentum stocks.

Several other popular factors, such as low-volatility and growth, also got whacked. But smaller companies and “value” stocks - generally cheaper, unloved companies and a factor that has been fizzling for large parts of the decade - have rocketed higher.

Here’s a Bernstein chart showing the move on Monday. Tuesday was also bad.

The US stock market was the epicentre of this factor earthquake, but it has also hit Europe, as this SocGen chart indices.

Basically almost everything that was hot is now not, and this year’s losers are soaring. For example, any popular hedge fund shorts have also enjoyed a renaissance, as this Goldman Sachs chart shows.

This will have hurt a lot of funds, especially trend-following hedge funds, quants that systematically mine factors, and more traditional L-S equity hedge funds that piled into hot trades that now have been trashed. Here’s a rundown from Credit Suisse.

What caused this? There are obviously whispers of a big hedge fund deleveraging, but IMO the moves are too big and wide - momentum got trashed in almost every market - to be plausible.

It’s likely that it was caused by another well-known pitfall: Crowding.

It’s likely that it was caused by another well-known pitfall: Crowding.

Remember that factors can bleed into each other. For ex, when everyone piled into high-growth tech in 2017, it meant that they scored well on growth, momentum AND low-volatility factors. That ultimately led to crowding and a ‘tech tantrum’ that summer: on.ft.com/2ZVnVbz

More recently, investors worried about weaker growth but turned off by evaporating bond yields have sought refuge in low-volatility and high-quality stocks (largely in more defensive sectors). Many are known as “bond proxies” for their steadiness and decent dividend yields.

That led them to enjoy positive momentum, leading in turn to even more crowding. But many of these stocks are *acutely* sensitive to bond yields, and with bond yields now inching higher it triggered a sudden break on Monday. From Bernstein:

So where does that leave us? The 2017 tech tantrum turned out to be a short-lived affair, and some analysts think investors should stick to defensive quality and low-volatility stocks despite the recent carnage.

But JPMorgan thinks this rotation out of momentum and quality and into value stocks could last a while.

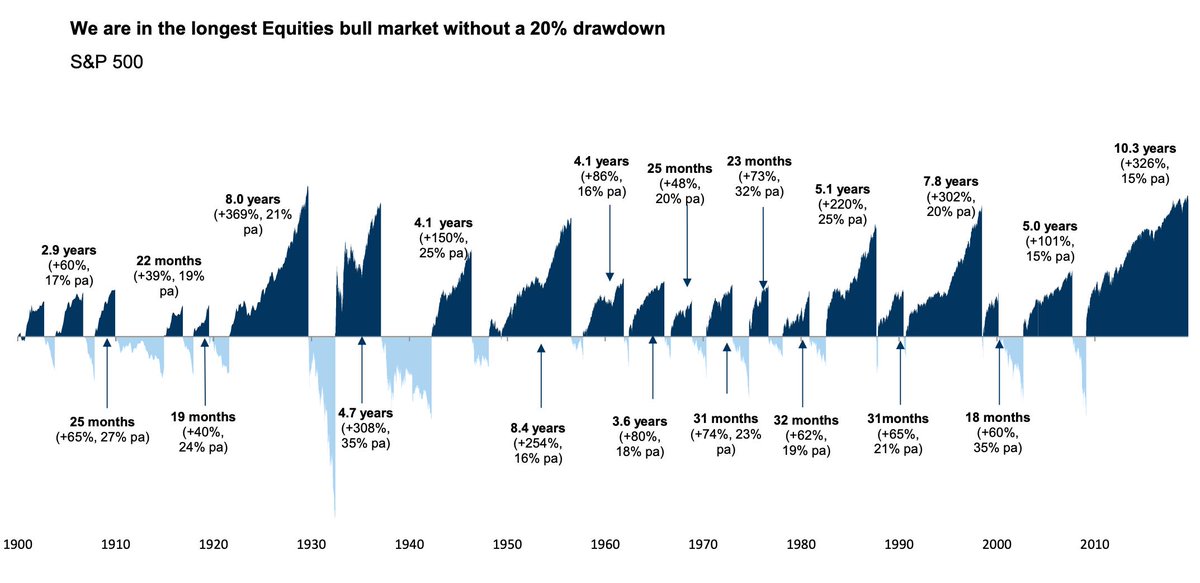

After all, value has underperformed momentum quite dramatically for a very long time, as this chart from Wolfe Research vividly shows: The recent correction hardy registers in the grand scheme of things.

But Wolfe’s quant guru Yin Luo is worried that a violent factor rotation can feed on itself and deepen. Even more worryingly, he points out the similarities to the “quant quake” of August 2007, when a lot of quantitative hedge funds suddenly saw shit go bananas.

(Here’s a piece I wrote a while back looking at the lessons of the quant quake.) on.ft.com/2Q4EaPn

Luo points out that the quant quake was arguably an early symptom of deeper problems in the financial system, and says that there is at least a possibility that the recent factor earthquake is another ill omen.

Important to note that hedge funds use a LOT less leverage than they did in 2007, so any losses won’t be nearly as bad. But this has been a *really* interesting week for markets.

Hopefully I haven’t screwed up this explanation too much. If I have them I hope @CliffordAsness @RobertoMCroce @amoralelite and other smarter people than me can weigh in!

Last chart, showing how market neutral momentum has been caned recently.

Frustrated FT value readers are all 😍😍😍 at momo getting brutalised tho on.ft.com/2LQaCPS