Here's Comm'r @HesterPeirce's Safe Harbor for Fundraising by #Token Sale proposal 1/x:

https://twitter.com/crowdfundinside/status/1225765917721796608

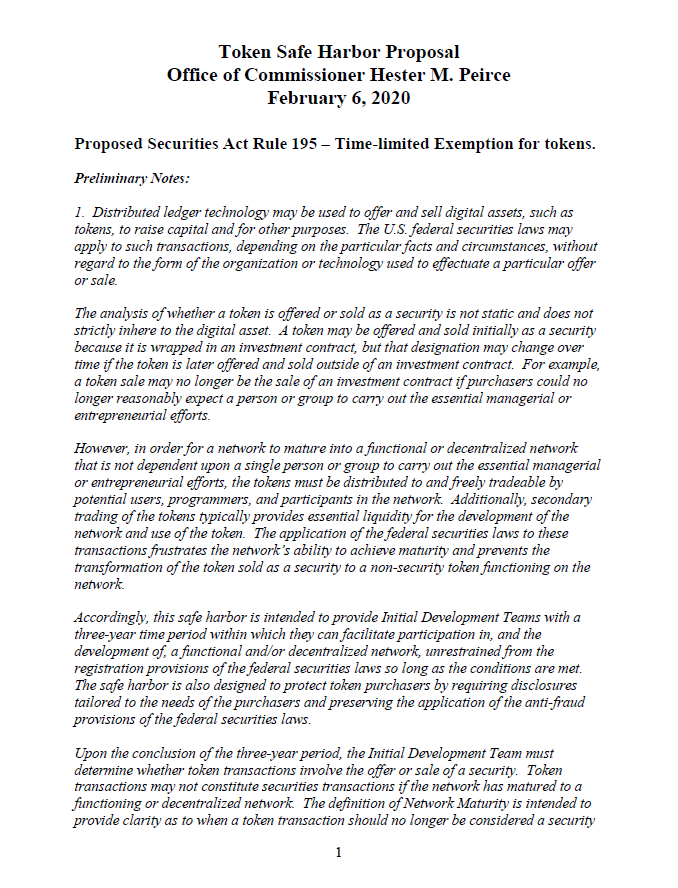

@HesterPeirce Let's dive in. The first thing that struck me was the tone/mission statement implied. This looks like "how do we make workable token sales that allow networks to develop" not "how do we apply the securities laws to issuers of instruments" Is this a policy shift?

@HesterPeirce or is this a new concept- that #crypto networks that require token distribution to boostrap into some non -investment-focused purpose needs to "get through" being a security to develop into a product/system that has an ultimate non investment purpose?

@HesterPeirce Interesting choice to allow the Initial Development Team to determine if transactions involve the offer of a security after 3 yrs- like private placement self-disclosure vs some RegA type qualification. Shifts burden from SEC staff while allowing enforcement for non compliance

@HesterPeirce Network maturity, the 2nd new gloss on "Reliance on the efforts of others" of Howey is defined- no control by a single logical entity or achievment of functionality as demonstrated by the ability of holders to use tokens in a manner consistent with the utility of the network. hmm

@HesterPeirce measuring "centralization" of control will continue to be difficult/fact sensitive, rely on disclosure of #governance, actual compliance with disclosed governance. The #crypto world has been famously terrible with this. cc: #TheDao, #Ethereum

@HesterPeirce the "Functional" prong is keyed on the "ability" of users to use tokens for non-investment purpose.... as opposed to the actuality of how investors are using the tokens. Sure, can be used to buy smart contract execution- but mostly is used as a substitute for currency.

@HesterPeirce and a lot of is used to speculate and trade on exchanges. (and yes, i'm picking on ETH and yes, ETH is only unique from other tokens because some holders of ETH ACTUALLY USE IT- but not as many as those who use it like money or to trade)

@HesterPeirce Sussing out reliable metrics to determine use for investment purpose versus actualization of the "ability" of users to use a token for non investment/non speculative purpose is a big challenge for the industry.

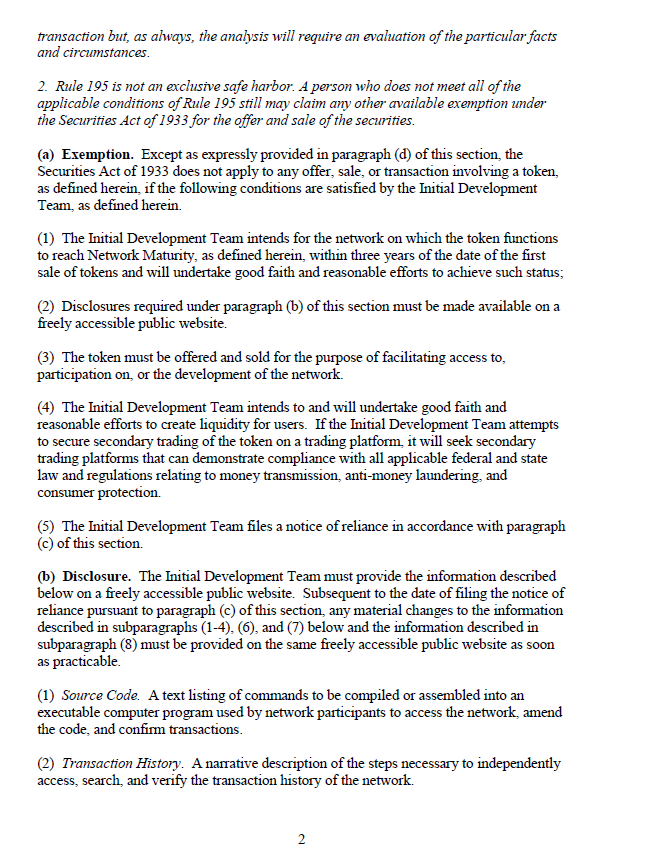

@HesterPeirce Section 4, pg 2 suggests that facilitating secondary liquidity is encouraged to "distribute the tokens" &that those tokens should be traded on platforms that comply with federal and state law & regs re: money transmission, AML, & consumer protection... blue sky may still apply

@HesterPeirce Issuers would be required to disclose "Source Code," defined as "a text listing of commands to be compiled or assembled into an executable computer program used by network participants to access the network, amend

the code, and confirm transactions." Does this disclosure /1

the code, and confirm transactions." Does this disclosure /1

@HesterPeirce obligation change over time? Is it static? Is there an obligation to update? Audit requirement? I can see this being abused.... & I see the SEC trying to balance between disclosing millions of lines of code vs. disclosing something useful/comprehensible to investors.

@HesterPeirce I can imagine the litigation over what a reasonable investor assumed the code disclosures meant versus what a coder understood them to mean. CC: @grimmelm

@HesterPeirce @grimmelm The "token economics" & "initial development team" defs. suggest that there may be prior distributions of tokens to founders/insiders before the safe harbor filing/issuance. Are we segregating classes of tokens btwn those restricted (i.e. RegD) & those issued via safe harbor?

@HesterPeirce @grimmelm Here's the provision on the notice to be filed including an obligation to update the notice when there's a "material" change in the information provided- what's a material change in source code? Imagine the litigation....experts....I'm glad I can still sorta read code!

@HesterPeirce @grimmelm If a narrow view of "material change" to code is taken, get ready for many, many lawsuits. If a broad view of "material change" is taken, get ready for many, many amendments to be filed.

@HesterPeirce @grimmelm It looks like sales may be made in reliance upon the safe harbor prior to the filing (this perhaps addresses my insider presale/ RegD vs. 195 classes of tokens concerns) - so if i'm reading this right, RegD's become freely tradeable upon the filing of the Notice contemplated....

@HesterPeirce @grimmelm Definition time! Token def suggests that a token "has a transaction history"- does this mean some amount of trading is required to claim the safe harbor? or that an existing system that facilitates trades is a predicate? call it the ERC20 minimum standard

@HesterPeirce @grimmelm "Token" excludes debt & equity, &instruments that represent an “entitlement to any interest or dividend payment” in a “partnership.” How do #POS systems fare under this rule? Tees up analysis of whether a given system creates a GP among its participants. Maybe bad news for #Daos.

@HesterPeirce @grimmelm Network Maturity- def not meant to preclude "network alterations achieved through a predetermined procedure in the source code that uses a #consensus mechanism and

approval of network participants" I guess forks & on chain governance are still ok!

approval of network participants" I guess forks & on chain governance are still ok!

@HesterPeirce @grimmelm Final question- what happens when the Initial Development Team realizes they can't execute- do they get a reset 3 years when they pivot?

• • •

Missing some Tweet in this thread? You can try to

force a refresh