Here are nominal returns for various investments during key periods of history. Note the 1940s' big returns for small caps and value. Bonds were repressed back then, with a cash-like return for a cash-like volatility. Could this be part of the Fed’s playbook in years ahead?

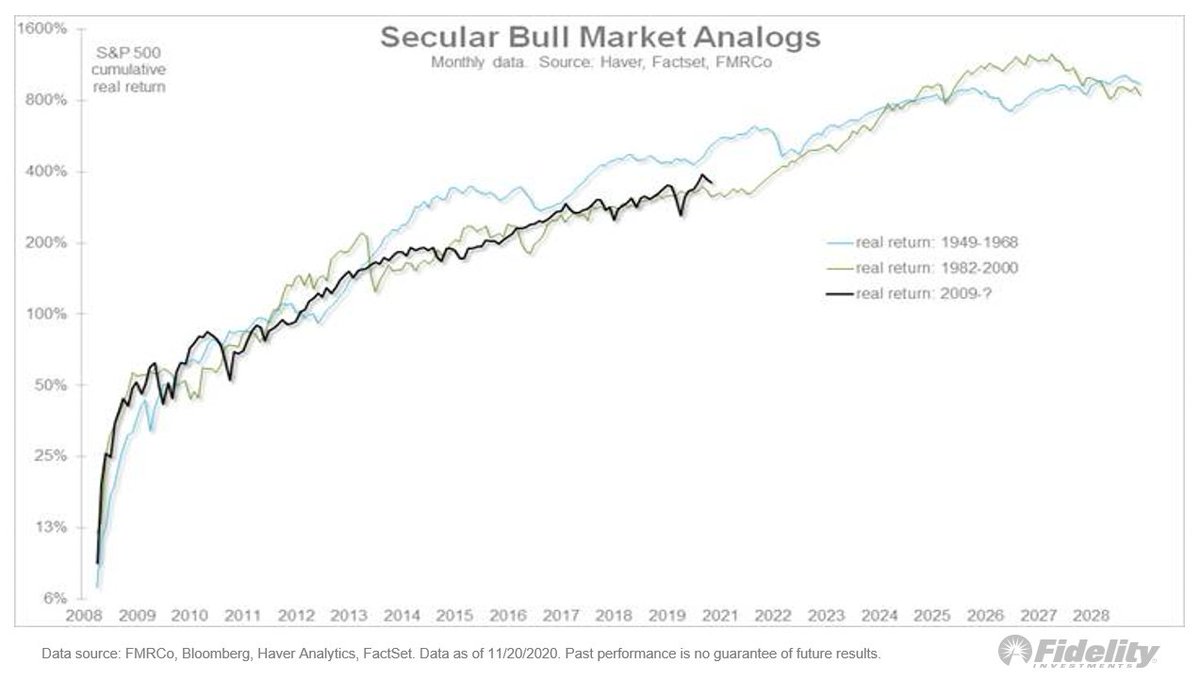

For clarification, I picked the 5 regimes for specific reasons to highlight possible analogs to today’s markets. 2009-2021 is the current post-GFC “monetary inflation” regime, which, in my opinion, is also a secular bull market that may have a ways further to go. (1/4)

1982-2000 was the previous secular bull market, driven in part by disinflation. 1949-1968 was the secular bull market before that, driven by post-depression/WWII productivity and demographics. (2/4)

1942-1951 was the “financial repression” regime, driven by fiscal/monetary policy coordination during WWII (including rate caps), and ending with the Fed’s new-found independence in 1951. (3/4)

Finally 1962-1985 was the “rising/high inflation” regime. Inflation was low-for-long during the 1950s and early 1960s, started a gradual climb during the late 1960s, and then rose rapidly during the 1970s. (4/4)

• • •

Missing some Tweet in this thread? You can try to

force a refresh