ING Bank 1/4: #Eurozone: Waiting for the European phoenix

1Q21 will not be remembered as the finest hours of European politics. The glacial roll-out of vaccination programmes and the ‘crown jewel’ of the EU’s fiscal stimulus – the EU’s €750bn Recovery Fund –

1Q21 will not be remembered as the finest hours of European politics. The glacial roll-out of vaccination programmes and the ‘crown jewel’ of the EU’s fiscal stimulus – the EU’s €750bn Recovery Fund –

ING Bank 2/4: is gathering dust in a Karlsruhe courtroom stand in stark contrast to the achievements in the US. Yet all is not lost. European manufacturing is holding up well and there are signs of life in the EU vaccine roll-out.

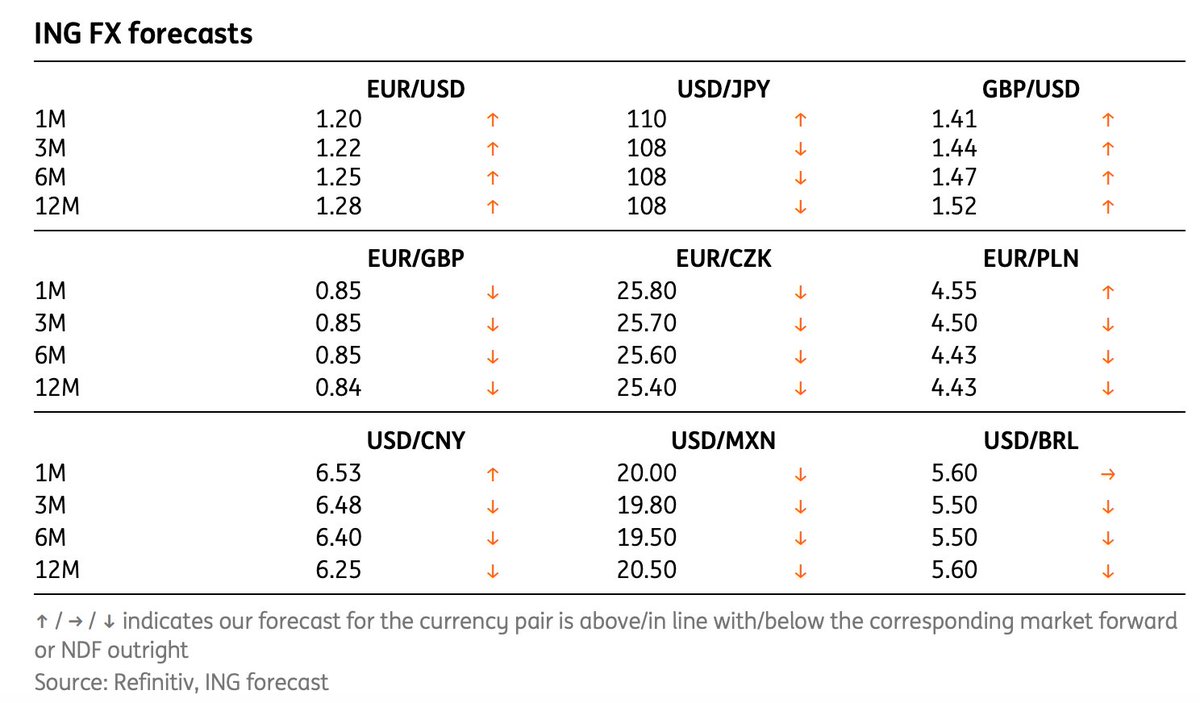

ING Bank 3/4: Our #EURUSD profile is slightly dimmed, but we still expect the #EUR to arise from the ashes of European policy. It should be in a position to challenge 1.25 – though probably not now until the third quarter.

ING Bank 4/4: This all assumes that the #Fed can withstand the coming tide of inflation and that US 10-year yields can move to 2.00% in an orderly manner.

• • •

Missing some Tweet in this thread? You can try to

force a refresh