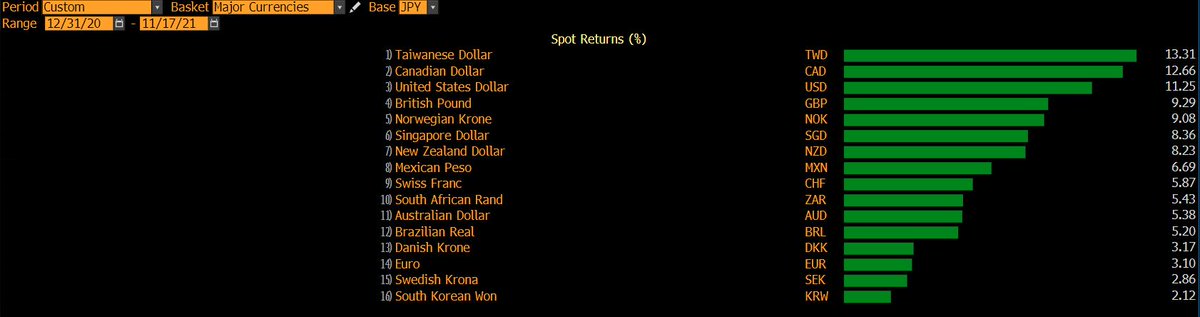

#Dollar (DXY) not driven by #RealRates recently

Since hawkish Jun FOMC, DXY +5.7% v/s 5y US Real yld 23bp lower

Dollar's resilience despite inflation spike in US & despite drop in US real rates further incentivizes foreign investors to buy more $ assets

Since hawkish Jun FOMC, DXY +5.7% v/s 5y US Real yld 23bp lower

Dollar's resilience despite inflation spike in US & despite drop in US real rates further incentivizes foreign investors to buy more $ assets

https://twitter.com/VaradMarkets/status/1460384338055368706?s=20

Basic Maths:

▪️ European investor invests EUR100 ($115 @ 1.1500) in 5y UST at 1.22%

▪️ Gets back ~$122 after 5y

▪️ If converts $ back to EUR at unch 1.1500=>EUR106.25

If $ strengthens to say 1.1000 (w/o FX adjustment despite rocket relative inflation), she gets back ~EUR 111.0

▪️ European investor invests EUR100 ($115 @ 1.1500) in 5y UST at 1.22%

▪️ Gets back ~$122 after 5y

▪️ If converts $ back to EUR at unch 1.1500=>EUR106.25

If $ strengthens to say 1.1000 (w/o FX adjustment despite rocket relative inflation), she gets back ~EUR 111.0

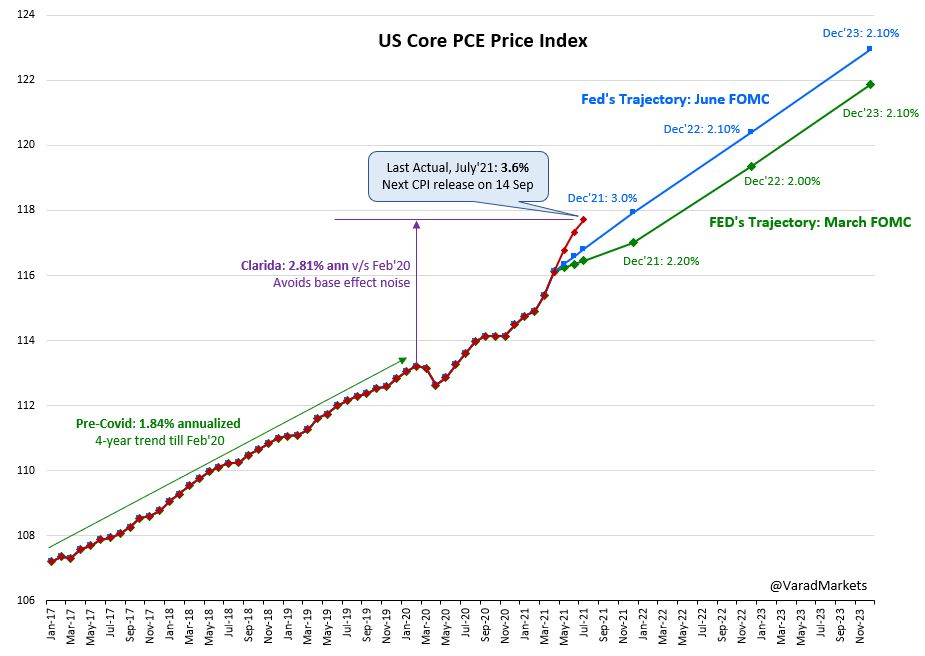

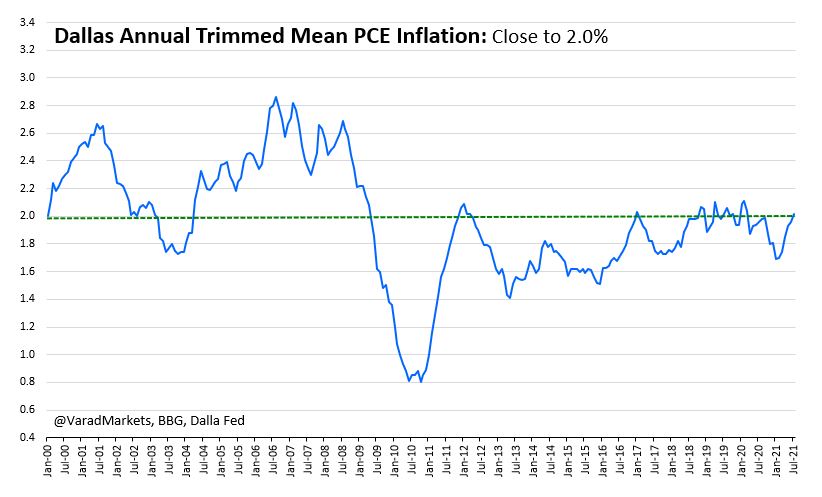

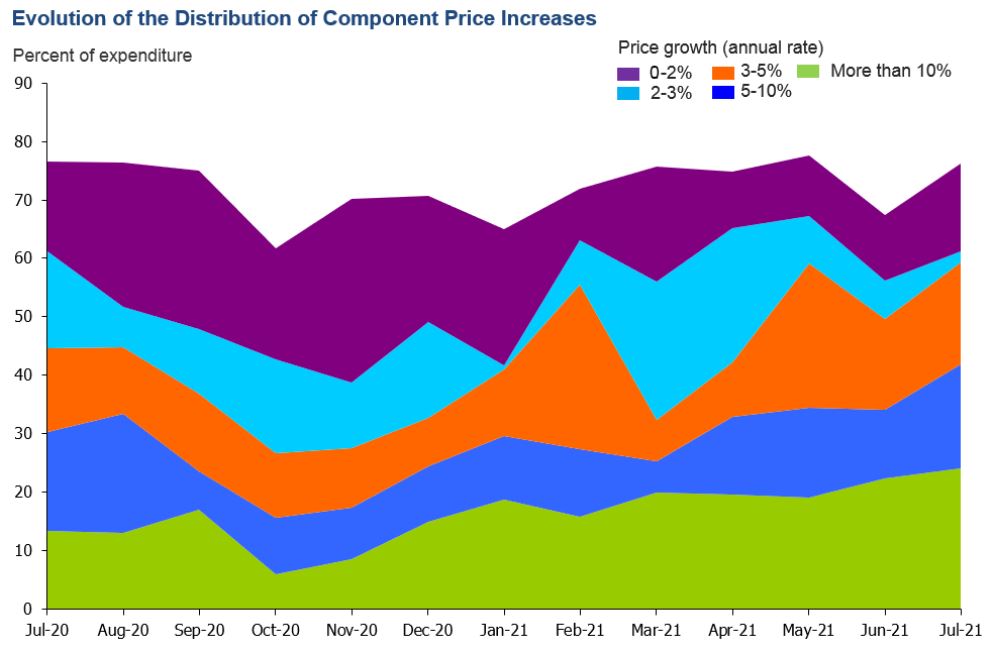

Steep term structure of US Real Rates partly reflecting expected 'transitory-ness' of inflation

• • •

Missing some Tweet in this thread? You can try to

force a refresh