Day 2 of the #CEPR Household Finance conference

Day 1 here

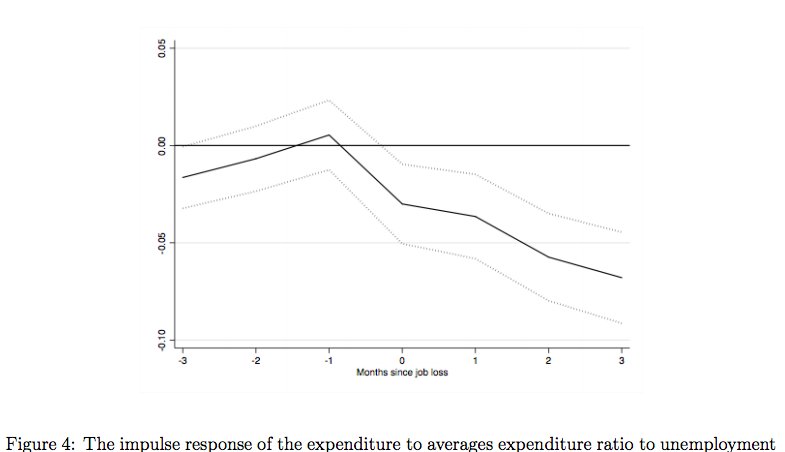

Credit Smoothing by Arna Olafsson, Michaela Pagel and Sean Hundtofte

Use of high interest borrowing (in Iceland, overdraft checking accounts):

- heavily used in good times (-> high fees)

- not used to smooth consumption in times of unemployment

Use of high interest borrowing (in Iceland, overdraft checking accounts):

- heavily used in good times (-> high fees)

- not used to smooth consumption in times of unemployment

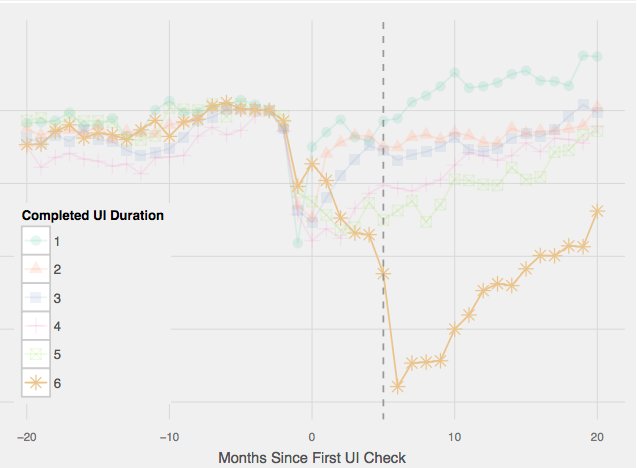

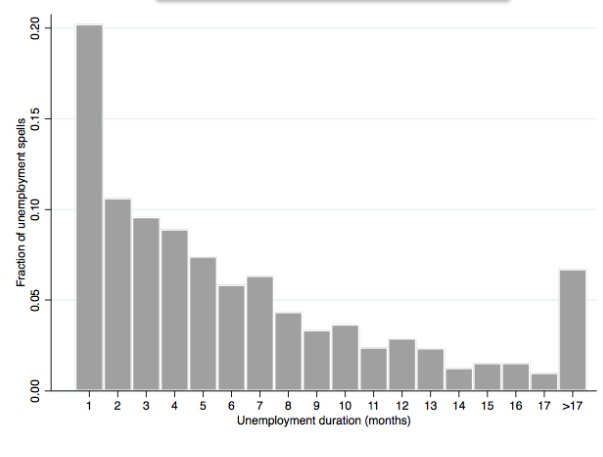

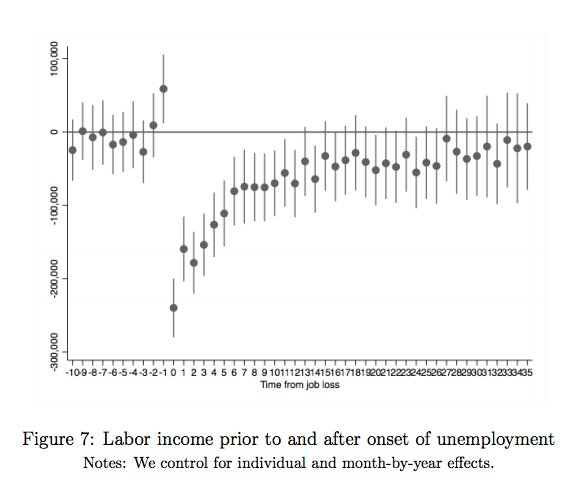

Similar data approach as @pascaljnoel and @p_ganong; use UI benefit receipts to identify unemployment spells; their work suggests individuals are incompletely insured against losing your job

scholar.harvard.edu/files/ganong/f…

scholar.harvard.edu/files/ganong/f…

Data based on Meniga financial aggregator (Mint equivalent); which has advantage of being more commonly used in Iceland; used by these co-authors in a number of cool papers

dropbox.com/s/1ya10trur7s4…

dropbox.com/s/1ya10trur7s4…

Spending falls 5% after unemployment, as in other contexts

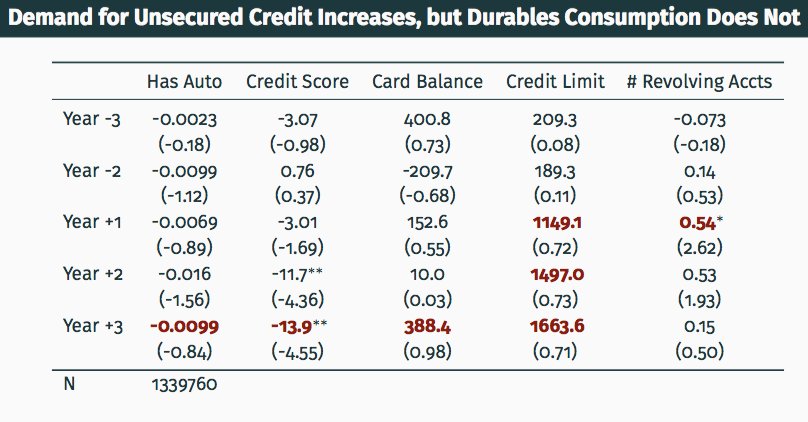

Overdraft usage up by about $175; not much and not significant

Overdraft usage up by about $175; not much and not significant

Unlike other settings (ie econ.ucla.edu/tvwachter/pape…); job loss in Iceland leads to only temporary loss of income.

-> people using high-cost borrowing, but not to smooth transitory shocks

-> people using high-cost borrowing, but not to smooth transitory shocks

Suggests demand for credit cards is precautionary in bad times -- I find similarly low evidence for credit utilization after cancer diagnoses

papers.ssrn.com/sol3/papers.cf…

papers.ssrn.com/sol3/papers.cf…

Why are people risk-averse in using high-cost cards in bad times, but willing to do so in normal times?

Harder to say, and large literature, but at least consistent with behavioral biases inducing myopic borrowing behavior

Harder to say, and large literature, but at least consistent with behavioral biases inducing myopic borrowing behavior

Alternative: people cut work-related consumption (as they do after retirement) faculty.chicagobooth.edu/erik.hurst/res…) and so are already pretty-well insured such that they don't need credit

Next: Mobility Constraints and Labor Market Outcomes: Evidence from Credit Lotteries

by Janis Skrastins, Bernardus Van Doornik, Armando Gomes and David Schoenherr

by Janis Skrastins, Bernardus Van Doornik, Armando Gomes and David Schoenherr

Randomized access to motorcycle results in:

- more formal employment

- higher wages (2.5%)

- longer commutes

- persistent: motorcycle lottery winners has 10-year persistent impact

- more formal employment

- higher wages (2.5%)

- longer commutes

- persistent: motorcycle lottery winners has 10-year persistent impact

Southern Italy is now one of the poorer parts of the EU. But wasn't always the case.

- Palermo had about 350k people in 1050, second largest city in Europe (after Cordoba)

- Naples one of the largest cities in Europe from 1500 on, industrialized under protectionist Bourbons

- Palermo had about 350k people in 1050, second largest city in Europe (after Cordoba)

- Naples one of the largest cities in Europe from 1500 on, industrialized under protectionist Bourbons

Why?

- Guiso, Sapienza, Zingales suggest social capital kellogg.northwestern.edu/faculty/sapien…

- People have pointed to institutional differences (competitive city-states in north; more autocratic "extractive" institutions in south due to foreign invasions

- mafia, corruption

- many others

- Guiso, Sapienza, Zingales suggest social capital kellogg.northwestern.edu/faculty/sapien…

- People have pointed to institutional differences (competitive city-states in north; more autocratic "extractive" institutions in south due to foreign invasions

- mafia, corruption

- many others

I'm struck by the comparison with the US -- an early industrializing north; more agricultural south which had difficulty adapting to modern economy

From this standpoint; the puzzle is more that the south didn't ever come close to parity with the north, despite wage differential

From this standpoint; the puzzle is more that the south didn't ever come close to parity with the north, despite wage differential

back to papers: From Saving Comes Having? Disentangling the

Impact of Saving on Wealth Inequality

by Laurent Bach, Laurent E. Calvet, and Paolo Sodini

cepr.org/sites/default/…

Impact of Saving on Wealth Inequality

by Laurent Bach, Laurent E. Calvet, and Paolo Sodini

cepr.org/sites/default/…

Savings rate in Sweden:

- decreasing with net worth up to 90th percentile of net worth (decreases wealth inequality)

- within wealth groups, a lot of dispersion in saving (widens wealth inequality)

- variation in returns drives wealth inequality

- decreasing with net worth up to 90th percentile of net worth (decreases wealth inequality)

- within wealth groups, a lot of dispersion in saving (widens wealth inequality)

- variation in returns drives wealth inequality

Comprehensive picture of wealth in this Swedish register data, including private equity, real estate; and security-level returns

The Scandinavian model of welfare state + free market features low income inequality, but high wealth inequality

The Scandinavian model of welfare state + free market features low income inequality, but high wealth inequality

My sense is that intergenerational wealth persistence is stronger in Europe than the US

One hypothesis: greater role for aristocratic landowners in Europe, and more persistence in real estate wealth (as opposed to owning one idiosyncratic factory)

One hypothesis: greater role for aristocratic landowners in Europe, and more persistence in real estate wealth (as opposed to owning one idiosyncratic factory)

Rich save less than the poor, which seems good for lowering inequality.

But the dispersion of savings rates within wealth means that the idiosyncratic savers grow their wealth

+ rich seem like they have access to better investment opportunities

But the dispersion of savings rates within wealth means that the idiosyncratic savers grow their wealth

+ rich seem like they have access to better investment opportunities

So unlike Piketty/Saez; wealth inequality grows not because aggregate wealth persistently grows at constant rate, but because of mobility (moderately wealthy save a lot) and heterogeneity in portfolio returns

Prior research by these authors finds that:

- low income hold cash

- middle class own real estate (levered, but not scalable, and can result in good returns)

- upper class own financial claims, commercial real estate, and privately owned business

- low income hold cash

- middle class own real estate (levered, but not scalable, and can result in good returns)

- upper class own financial claims, commercial real estate, and privately owned business

My paper with Chris Hansman:

Selection, Leverage, and Default in the Mortgage Market

cepr.org/sites/default/…

Selection, Leverage, and Default in the Mortgage Market

cepr.org/sites/default/…

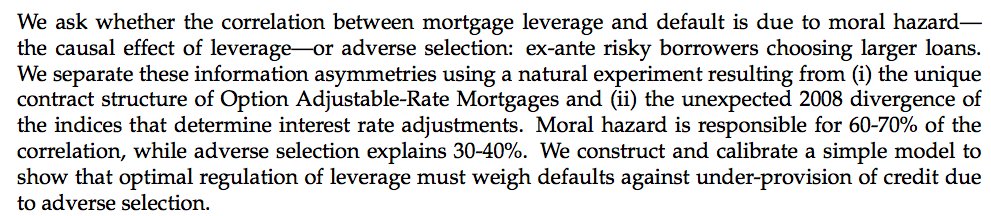

Our goal is to understand the strong relationship between leverage and mortgage default.

Understanding the sources of mortgage leverage, and regulation, has been a huge focus.

But information asymmetry strong in this context, and hard to understand.

Understanding the sources of mortgage leverage, and regulation, has been a huge focus.

But information asymmetry strong in this context, and hard to understand.

What are these asymmetries?

- moral hazard: higher loan balances induce strategic default

- adverse selection: riskier borrowers select higher leverage contract

-> which is dominant in explaining leverage has large impact on ideal regulation

- moral hazard: higher loan balances induce strategic default

- adverse selection: riskier borrowers select higher leverage contract

-> which is dominant in explaining leverage has large impact on ideal regulation

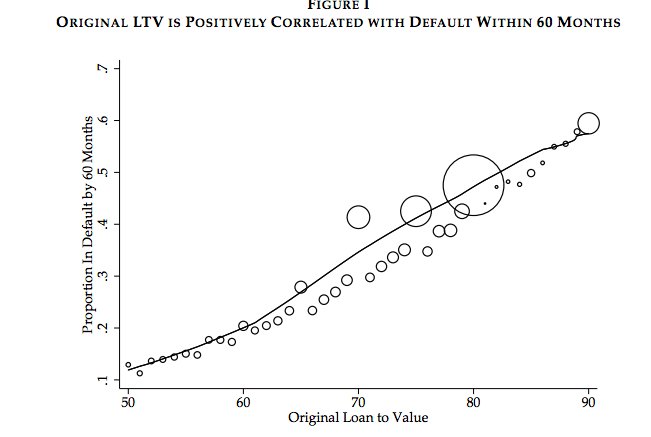

To look at these, we use the feature of Option ARM mortgages that they are tied to LIBOR or Treasury

surprising variation in the values of these indices results only in *balance* variation in Option ARMs (since payments are pre-set, and low - generally negatively amortizing)

surprising variation in the values of these indices results only in *balance* variation in Option ARMs (since payments are pre-set, and low - generally negatively amortizing)

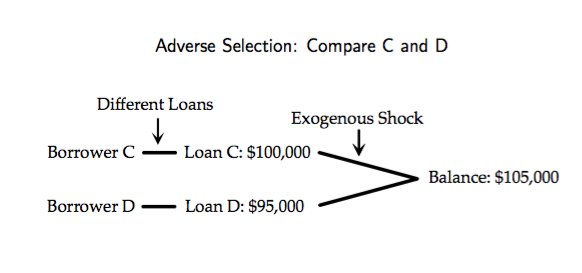

So moral hazard in this context is borrowers who take out identical loans in the same month; but are exposed to different balances ex post. If balance -> default, we think of that as strategic default/moral hazard.

Adverse selection is difference in default rates among borrowers who ex post face the same balance due to these balance shocks; but had selected different contracts ex ante.

Borrowers defaulting on mortgages due to a balance shock which does not affect their payment is evidence for strategic default effects

Disentangling the sources of default: about 2/3rds of leverage-default correlation is due to moral hazard and 1/3 due to adverse selection

Disentangling the sources of default: about 2/3rds of leverage-default correlation is due to moral hazard and 1/3 due to adverse selection

Why is it important to estimate these? We evaluate macro-prudential policy which is a common tool used to regulate leverage in these markets. We consider:

- no cap

- LTV cap at 90 (no selection)

- LTV cap at 90 (selection as calibrated in data)

- no cap

- LTV cap at 90 (no selection)

- LTV cap at 90 (selection as calibrated in data)

When there is an LTV cap without selection, borrowers just bunch right below the LTV cutoff.

But *with* selection, borrowers use down payments to screen themselves. So cap pushes riskier borrowers down in the distribution.

But *with* selection, borrowers use down payments to screen themselves. So cap pushes riskier borrowers down in the distribution.

Lenders reprice given these riskier borrowers, offering borrowers higher interest rates and lower balances. To separate themselves, borrowers move down the distribution taking a larger down payment. These borrowers are riskier, so there are knock-on effects.

As the result of a local cap in LTVs in the presence of adverse selection; *all* borrowers experience repricing which results in higher interest rates and lower balances.

-> default externality needed to make LTV cap welfare-neutral are calibrated to be 50% higher

-> default externality needed to make LTV cap welfare-neutral are calibrated to be 50% higher

Next: Education, Cognitive Performance, and Investment Fees

by John Beshears, James Choi, David Laibson, @BrigitteMadrian, William L. Skimmyhorn, Stephen Zeldes,

by John Beshears, James Choi, David Laibson, @BrigitteMadrian, William L. Skimmyhorn, Stephen Zeldes,

Household Finance distinguishes itself as a field, among other reasons, in focus on behavioral factors behind financial decisions

Financial decisions are not always salient, sometimes opaque, hard to calculate

-> suggests greater cognitive ability should limit mistakes

Financial decisions are not always salient, sometimes opaque, hard to calculate

-> suggests greater cognitive ability should limit mistakes

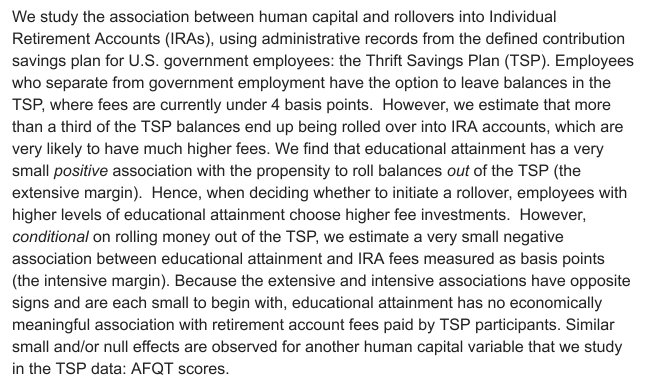

Very cool data here -- army personnel with TSP balances. Pretty good gov retirement plan, features low fees

Can roll these over (while employed by the army or when leaving) to IRA accounts, which generally have higher fees.

Q - does education, IQ explain rollovers?

Can roll these over (while employed by the army or when leaving) to IRA accounts, which generally have higher fees.

Q - does education, IQ explain rollovers?

Few people (1.8%) get an annuity, even though many people are near retirement and constant annuity income would be seemingly helpful for retirement.

Part of generic annuity puzzle nber.org/papers/w18575

Part of generic annuity puzzle nber.org/papers/w18575

Cool result here is that higher education, IQ (AFQT score) predicts greater rollovers. Not much difference in fees when you have rolled over by education/IQ.

Discussion: by @TRamadorai

- education could predict financial decisions causally (in which cases returns to education are even higher)

- education can be selected for by people who make good decisions

- education could predict financial decisions causally (in which cases returns to education are even higher)

- education can be selected for by people who make good decisions

Alternate view of education

Result similar to literature on financial education, which has not found large beneficial effects.

My takeaway in general is that financial decisions are hard, so generally people should make fewer decisions and we should focus on incentivizing/regulating intermediaries well

My takeaway in general is that financial decisions are hard, so generally people should make fewer decisions and we should focus on incentivizing/regulating intermediaries well

Also interesting here because inertia is often bad (ie, @TRamadorai on mortgage refinancing nber.org/papers/w21386); but here inertia is good

Alt interpretation: education gives you better understanding of performance + fees; but also generates overconfidence on ability resulting in bias for "active" decisions like trading, turnover, erc.

Increase in perceived signal precision -> "do" something

Increase in perceived signal precision -> "do" something

Cash extraction from retirement account also interesting -- higher for minorities, veterans, low education -- plausibly a "bad" decision holding fixed liquidity access

Aside from Achimedes’ principle, screw, the ship grappling claw, ship burning heat ray, odometer, etc. Archimedes also designed pulley systems - still in use in Sicily here

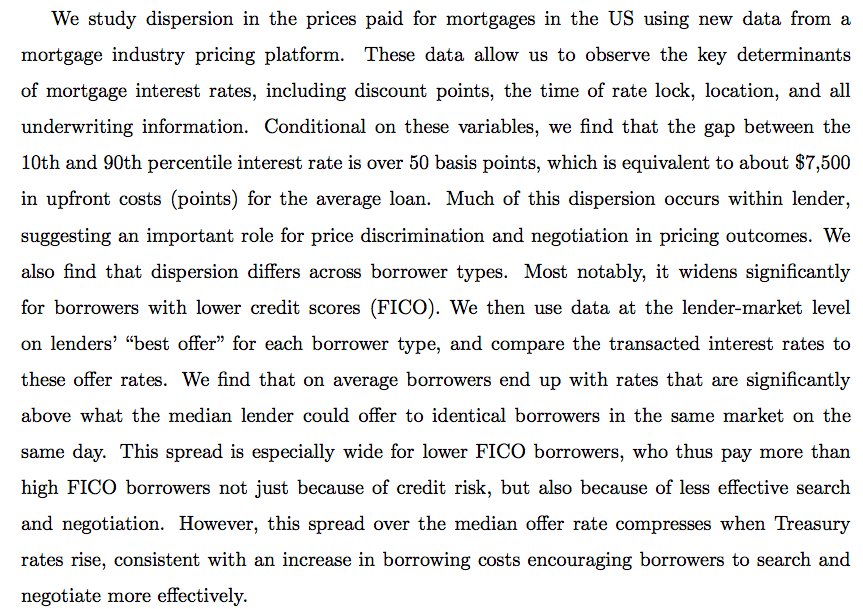

Okay last, but really cool paper -- Paying Too Much? Price Dispersion in the US Mortgage Market

by Neil Bhutta Andreas Fuster, and Aurel Hizmo

cepr.org/sites/default/…

by Neil Bhutta Andreas Fuster, and Aurel Hizmo

cepr.org/sites/default/…

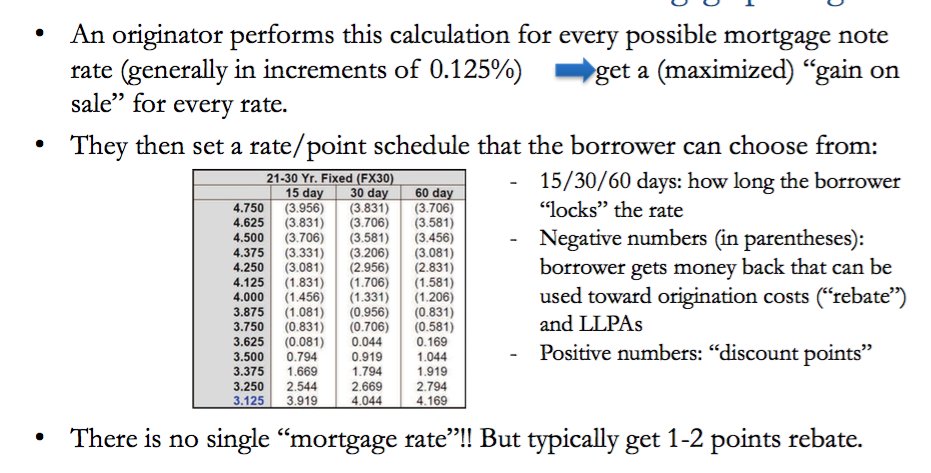

Goal of paper is to estimate whether borrowers pay different rates for same mortgage product. But really nice part of this paper is estimating mortgage points. These allow borrowers to pay down their interest rate (about 1/8th a % per percent of loan balance).

Basically, these deal with the fact that mortgages are typically priced in 5-point bins of LTV. So if you really prefer a 78% loan on house, no pricing advantage relative to 80%. But can pay 2% in points instead.

However, has been hard to measure historically.

However, has been hard to measure historically.

No such thing as a "mortgage rate" in the US. Have a menu based on the points, as well as the lock period. ie, longer you want to have the mortgage set for, the more points you give up.

So have more of a pricing curve offered to borrowers.

So have more of a pricing curve offered to borrowers.

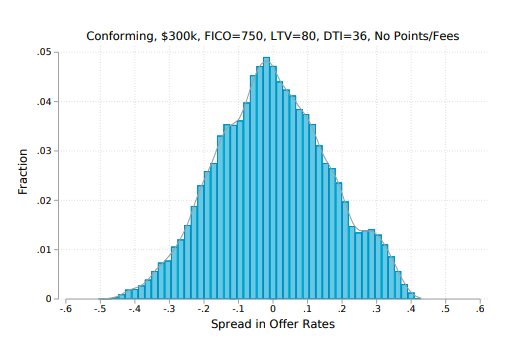

Accounting for those interest rate features -- winds up being huge dispersion in rates identical borrowers (in same market, same time) pay.

Even under monumental controls - suggests consumer search/negotiation

Even under monumental controls - suggests consumer search/negotiation

Who overpays?

- small loans (search morewith larger loan)

- low fico score borrowers already pay more for credit risk. But also pay more due to these search frictions

- borrowers in low rate periods (behavioral in some way - borrowers feel less need to keep shopping around)

- small loans (search morewith larger loan)

- low fico score borrowers already pay more for credit risk. But also pay more due to these search frictions

- borrowers in low rate periods (behavioral in some way - borrowers feel less need to keep shopping around)

So suggests another friction of passthrough of monetary policy on borrower rates