,

20 tweets,

8 min read

Read on Twitter

#mangalamorganics

YTD EPS vaulted to 66. Q3 EPS is double of last FY EPS. It's even better if we consider the numbers are after adjustment of exceptional loss of 5.6 crs for the qtr.

Normalised for exceptional items Q2 EPS is at 16.54 vs Q3 EPS of 37.21, more than doubled.

YTD EPS vaulted to 66. Q3 EPS is double of last FY EPS. It's even better if we consider the numbers are after adjustment of exceptional loss of 5.6 crs for the qtr.

Normalised for exceptional items Q2 EPS is at 16.54 vs Q3 EPS of 37.21, more than doubled.

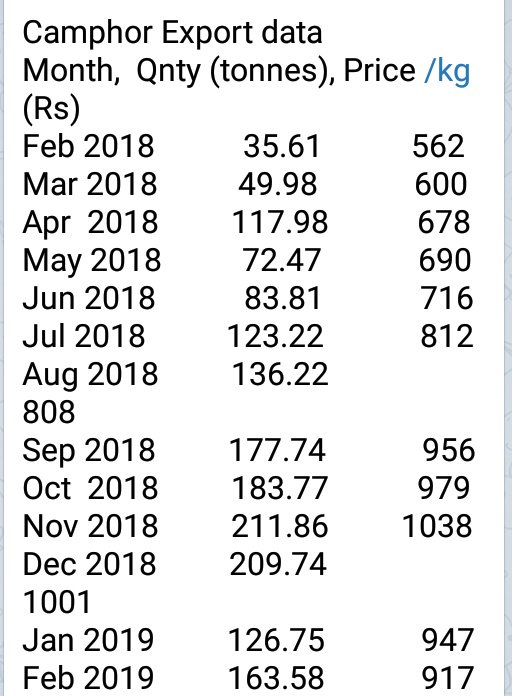

Firming up of camphor prices & DRT tie up helped post exceptional results. Have a feeling DRT tie up is not fully leveraged in this qtr & further EPS accretion in future quarters from this can't be ruled. Management commentary should provide some clarity.

#mangalamorganics

#mangalamorganics

In China, 98% of camphor produced is used for pharma, healthcare & hygiene. Where as in India, 98% of the produce is used for religious activity.

That untapped market is where the future growth is going to come in. Huge potential..

#MangalamOrganics

That untapped market is where the future growth is going to come in. Huge potential..

#MangalamOrganics

Why #MangalamOrganics can buck the trend, give seasonality a pass & produce a fantastic Q4 ?

India turned, net exporter of camphor on recent years & China has become net importer.

99% world's capacity in these two countries.

Camphor prices still holding & may go up by 50%

India turned, net exporter of camphor on recent years & China has become net importer.

99% world's capacity in these two countries.

Camphor prices still holding & may go up by 50%

#MangalamOrganics is moving in to retail with CAM+ segment - Pain relief sprays, balms, camphor cones, soaps etc

Has started producing specific products for DRT. Exports & DRT can take up Q4 slump in domestic demand

With no seasonality & improved earnings, PE rerating possible?

Has started producing specific products for DRT. Exports & DRT can take up Q4 slump in domestic demand

With no seasonality & improved earnings, PE rerating possible?

#MangalamOrganics has launched camphor soap bars in retail market under 'CAM+' segment.

Available in retail stores & also online in 'India's Apni Dukan' - Amazon.

Do check it out...

tinyurl.com/yxgrjmdg

Available in retail stores & also online in 'India's Apni Dukan' - Amazon.

Do check it out...

tinyurl.com/yxgrjmdg

#MangalamOrganics camphor products presence in consumer retail through CamPure & Cam+ brands:

-Puja Tablets

-Room Freshener Cone

-Insect Repellent Sticks

-Room Freshener Spray

-Cold or headaches Roll-on

-Cold Nasal Inhaler

-Pain relief Spray

-Bathing Soap Bar

-Puja Tablets

-Room Freshener Cone

-Insect Repellent Sticks

-Room Freshener Spray

-Cold or headaches Roll-on

-Cold Nasal Inhaler

-Pain relief Spray

-Bathing Soap Bar

Operating a 3 pronged strategy:

1. Direct Retail - Brand building, High Margins & variety

2. Bulk Sales - Firming up of wholesale rates helping margins

3. DRT Channel Sales - Exclusivity

#MangalamOrganics

1. Direct Retail - Brand building, High Margins & variety

2. Bulk Sales - Firming up of wholesale rates helping margins

3. DRT Channel Sales - Exclusivity

#MangalamOrganics

36,591 shares acquired by promoter between 26-28th Mar.

Definitely a good sign of times to come.

#MangalamOrganics

Definitely a good sign of times to come.

#MangalamOrganics

#MangalamOrganics launched 4 new camphor based products under their 'Cam+' line:

- Hand Wash

- Hand Sanitizer

- Pain Relief Balm

- Camphor Oil

All these are under B2C segment & available at Amazon.

- Hand Wash

- Hand Sanitizer

- Pain Relief Balm

- Camphor Oil

All these are under B2C segment & available at Amazon.

#MabgalamOrganics closed at new ATH. Uncharted territory ahead..

Camphor prices sustained elevated levels in March too. Expecting a good Q4.

Latest SHP reveals an interesting fact. Count & volume under <2 lac is lower vs last Qtr. Accumulation by strong hands ??

#TimeToFly

Camphor prices sustained elevated levels in March too. Expecting a good Q4.

Latest SHP reveals an interesting fact. Count & volume under <2 lac is lower vs last Qtr. Accumulation by strong hands ??

#TimeToFly

Despite being the weakest Qtr of the year in camphor business cycle Q4 FY19 shows ~3x increase in volumes and ~2x increase in price vs last yr Q4.

Game on #MangalamOrganics

Game on #MangalamOrganics

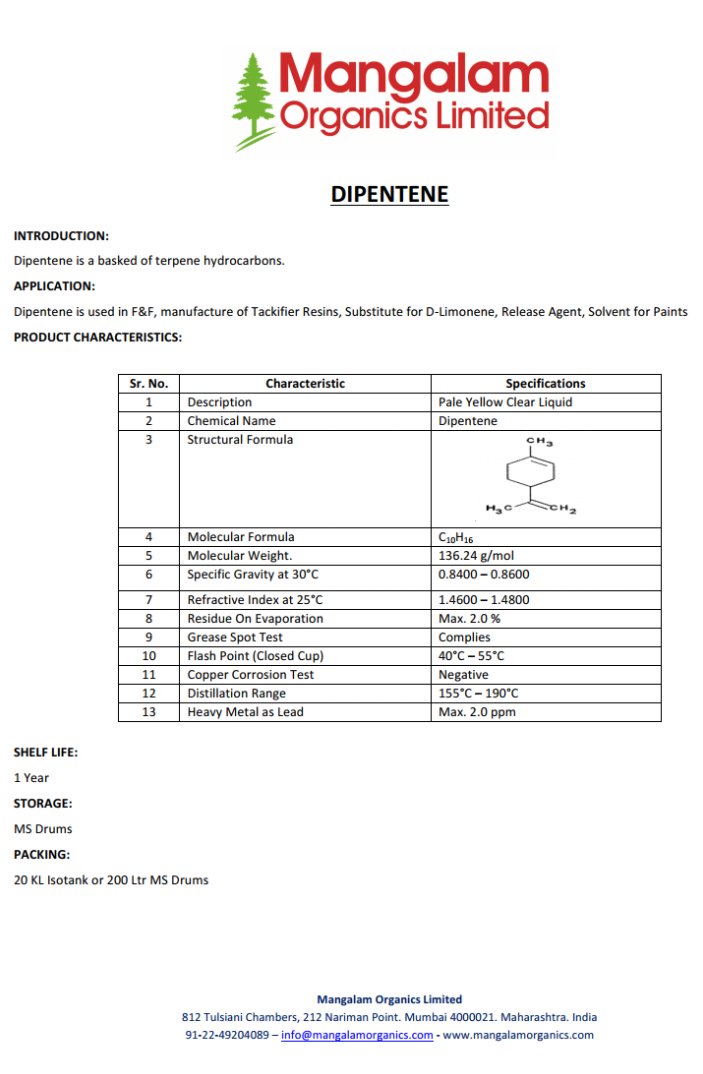

Dipentene the next leg of revenue driver for #MangalamOrganics , before incremental camphor & related products capacity kicks in..

#MangalamOrganics is one of the largest dipentene producers..

With DRT as their partner & sole distributor of their products in Europe, the volume game will kick in .

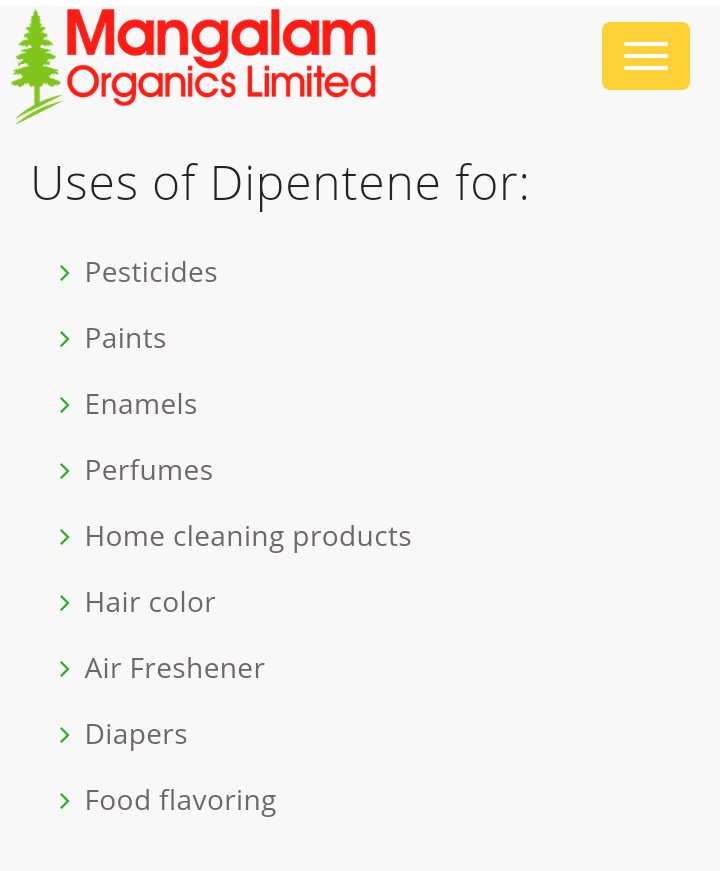

Dipentene is used in verity of applications..

With DRT as their partner & sole distributor of their products in Europe, the volume game will kick in .

Dipentene is used in verity of applications..

#MangalamOrganics - A very good Q4 despite being the weakest Qtr of the year.

YoY comparison makes sense for seasonal businesses rather than QoQ.

Revenue ⬆️ >100%

PAT ⬆️ >500%

Note:

1. Q4 has balance tax prov for the year - low tax provision made in earlier quarters

Contd..

YoY comparison makes sense for seasonal businesses rather than QoQ.

Revenue ⬆️ >100%

PAT ⬆️ >500%

Note:

1. Q4 has balance tax prov for the year - low tax provision made in earlier quarters

Contd..

2. Q3 low cost of material as a % of rev was an aberration due to accounting adj. Normalised in Q4

3. On full year basis EPS of Rs.84 vs Rs.14 for previous yr

4. YoY Increase in P&M to 51 cr from 33cr with 4 cr still in CWIP - Capacity expansion almost finished

Contd

3. On full year basis EPS of Rs.84 vs Rs.14 for previous yr

4. YoY Increase in P&M to 51 cr from 33cr with 4 cr still in CWIP - Capacity expansion almost finished

Contd

5. YoY inventory doubled from 33 crs to 66 crs - Getting ready for transition into a FMCG player from bulk commodity manufacturer - To drive margins

6. New capacity & full DRT sales to kick in from Q1 - To drive volume

Excited for management commentary & Q1.. #MangalamOrganics

6. New capacity & full DRT sales to kick in from Q1 - To drive volume

Excited for management commentary & Q1.. #MangalamOrganics

With Rs. 84 EPS for the year FY19, #MangalamOrganics is currently trading at ~5 PE.

Tailwinds :

- Capacity expansion

- DRT incremental volume

- Strong international camphor prices

- Value added products

- Retail expansion

Tailwinds :

- Capacity expansion

- DRT incremental volume

- Strong international camphor prices

- Value added products

- Retail expansion