,

9 tweets,

4 min read

Read on Twitter

Let's tackle this. Ms. Ryan - a lobbyist for a $30B hospital chain - is dead wrong here, and she's not the only one.

Research finds that surprise billing has nothing to do w/ narrow networks, and any legislation to curb out-of-network payments will also cut insurer profits. 1/n

Research finds that surprise billing has nothing to do w/ narrow networks, and any legislation to curb out-of-network payments will also cut insurer profits. 1/n

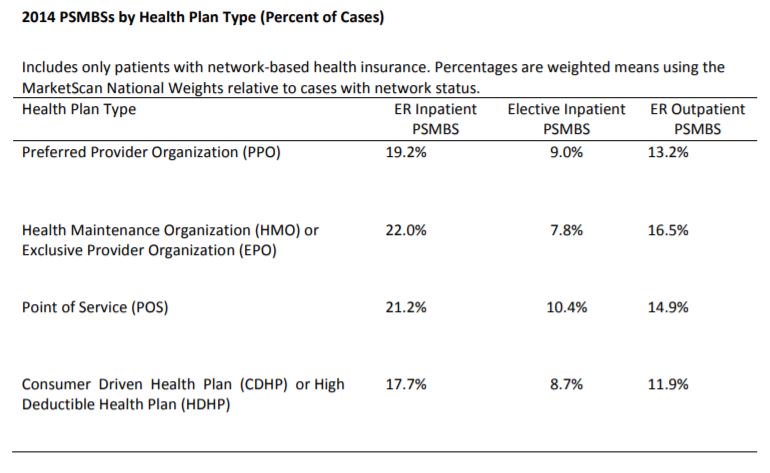

First, multiple studies have found little difference in the incidence of surprise billing across plan types.

For example, @cjrhgarmon & Ben Chartrock found that a 10th of hospital stays & 1 in 5 ER visits results in an OON bill, with no major differences by plan type (PPO etc).

For example, @cjrhgarmon & Ben Chartrock found that a 10th of hospital stays & 1 in 5 ER visits results in an OON bill, with no major differences by plan type (PPO etc).

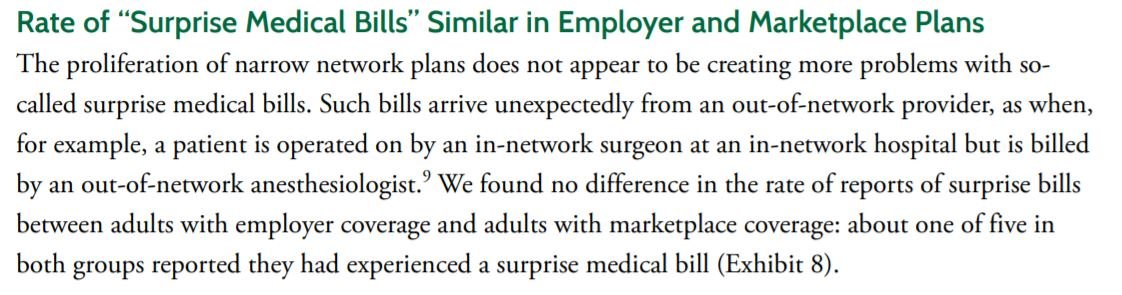

The @commonwealthfnd found a similar story when comparing employer-sponsored insurance (where broad PPO networks are common) and ACA marketplace plans, where many members choose narrow network plans.

commonwealthfund.org/sites/default/…

commonwealthfund.org/sites/default/…

Second, the argument is illogical. A network is only useful if patients *choose* in-network providers - that patient volume is the basis for the the plan/provider negotiation.

By definition, surprise bills occur when a patient has no choice, and hence network size is irrelevant

By definition, surprise bills occur when a patient has no choice, and hence network size is irrelevant

Put another way, would it make sense for a health plan to intentionally sign a contract w/ hospital X, and steer patients there, but exclude anesthesiologists staffing that hospital?

The patient & plan pay more for non-network anesthesiologists, so what purpose would this serve?

The patient & plan pay more for non-network anesthesiologists, so what purpose would this serve?

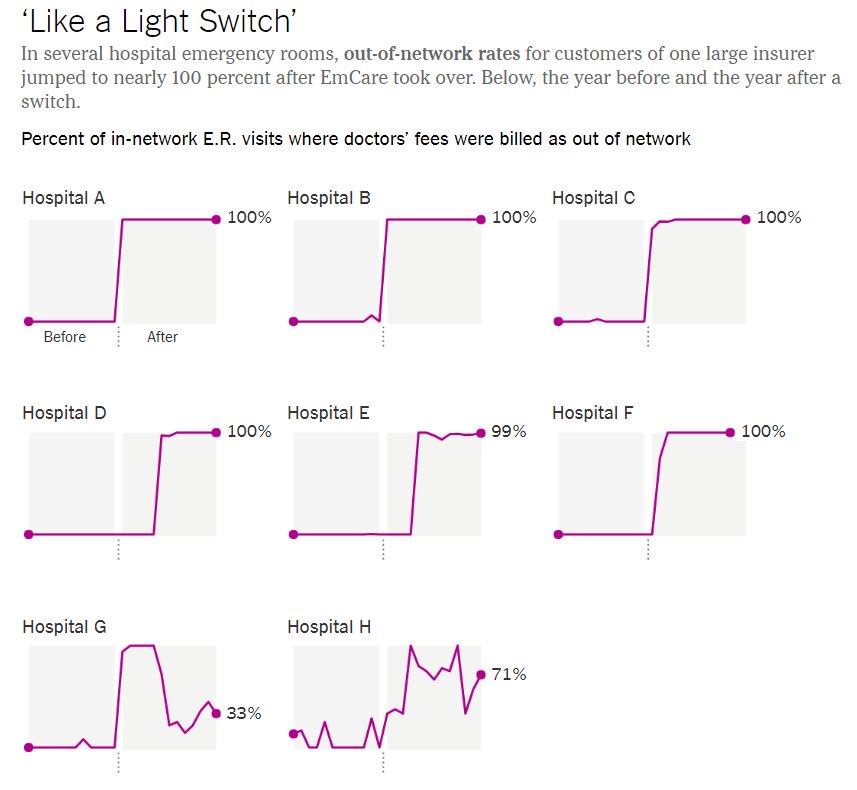

Third, the seminal research on this problem, by @zackcooperYale, @ProfFionasm & Nathan Shekita, found a clear pattern of abrupt network exits when certain staffing firms took over an ER. That is - surprise bills are triggered by decisions taken by providers, not health plans.

Finally, we turn to profits. For "fully-insured" private plans (80-90M Americans), insurers can only mark up the underlying provider reimbursement by a fixed %. Since a % of a smaller number is a smaller number, an insurer's revenues fall when underlying reimbursement falls.

For "self-insured" plans (the other ~100M privately-insured Americans), the employer pays the claims and then splits the overall bill with the employees, so any +/- in provider reimbursement is a +/- for the employer and the patient, and bypasses the insurer entirely.

All of the proposed federal laws would prohibit surprise billing in the self-insured market and portions of the fully-insured market.

Which means that any decrease in out-of-network reimbursement will also cut insurer profits. Any savings accrue to employers & patients. /n

Which means that any decrease in out-of-network reimbursement will also cut insurer profits. Any savings accrue to employers & patients. /n