THREAD

Please do RT thank you 🙏

What Scholars actually ask for Shariah Compliance vs What they should be asking

#islamicbanking #Islamicfinance #Shariah

Please do RT thank you 🙏

What Scholars actually ask for Shariah Compliance vs What they should be asking

#islamicbanking #Islamicfinance #Shariah

OK, following on from my earlier thread on Murabaha, and how it breaks Shariah laws, and the realisation that scholars and academics and professors actually do not seem to know what market practice is, I decided to write a thread about it.

I will try to explain how and why such

I will try to explain how and why such

practice, even though it is absolutely against AAOIFI Shariah standards, can be approved by reputable scholars.

And then I will illustrate what scholars SHOULD be asking in order to get to the truth of things.

Here, I will talk about a standard commodity Murabaha (CM)

And then I will illustrate what scholars SHOULD be asking in order to get to the truth of things.

Here, I will talk about a standard commodity Murabaha (CM)

on the international markets – quite a few varieties exist, but they all MUST exhibit the same qualities I describe below.

In this case let us assume this CM is for a bank to deliver financing to a customer.

First of all, let’s establish what a simple CM looks like: I found a

In this case let us assume this CM is for a bank to deliver financing to a customer.

First of all, let’s establish what a simple CM looks like: I found a

Whenever I see a diagram like this, I realise the writer has no idea what he is talking about. Secondly, this is intentionally misleading, either through ignorance or deception. In addition, when I read the explanation and defence of CM on this site, it confirmed

confirmed the writer has no clue at all.

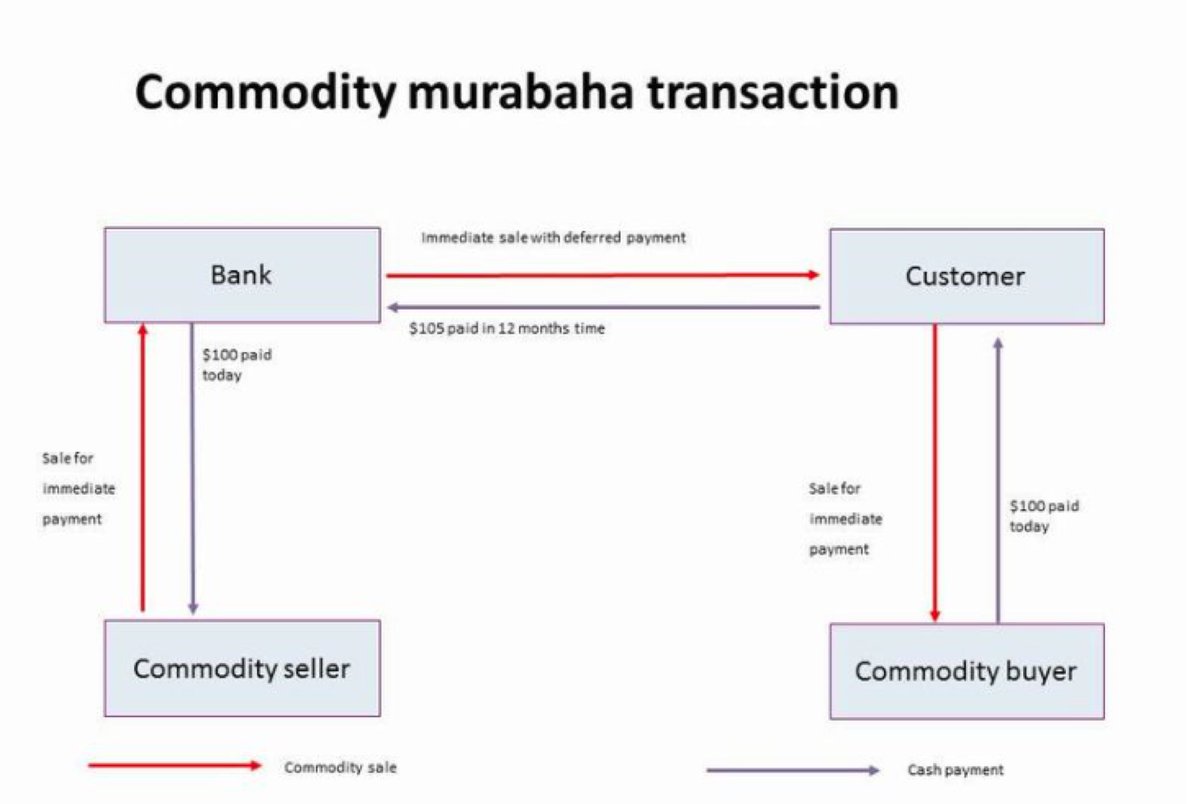

OK, so let’s find a better diagram:

This is from mohammedamin.com who is an experienced professional in Islamic banking.

@Mohammed_Amin

OK, so let’s find a better diagram:

This is from mohammedamin.com who is an experienced professional in Islamic banking.

@Mohammed_Amin

@Mohammed_Amin Ok we see the four parties, and we can see three transactions. Of course there is a fourth transaction, but when you are talking to scholars, it is best NOT to talk about this fourth transaction : )

Ok, so, in order - the transaction on the left occurs first, then the top one,

Ok, so, in order - the transaction on the left occurs first, then the top one,

then the right one. They have to occur in this order, to avoid the prohibition on short selling.

OK, so the bank here wants to get Shariah approval for this structure, this is what the conversation looks like:

What Scholars do – they ask questions like the following:

OK, so the bank here wants to get Shariah approval for this structure, this is what the conversation looks like:

What Scholars do – they ask questions like the following:

Scholar: What is the basis of this structure?

Bank: it is based on the Murabaha contract.

S: Ok, so the bank purchases commodity first?

B: Yes

S: And then sells it to the customer, on a deferred payment basis?

B: Yes

S: and the bank discloses the cost price, thus making this a

Bank: it is based on the Murabaha contract.

S: Ok, so the bank purchases commodity first?

B: Yes

S: And then sells it to the customer, on a deferred payment basis?

B: Yes

S: and the bank discloses the cost price, thus making this a

Murabaha sale transaction?

B: Yes

S: And the customer sells this on a spot basis to a third party?

B: Yes, to the Commodity Buyer as my diagram helpfully shows you.

S: Now, this buyer is not the same as party as the commodity seller is it? Because this would not be Shariah

B: Yes

S: And the customer sells this on a spot basis to a third party?

B: Yes, to the Commodity Buyer as my diagram helpfully shows you.

S: Now, this buyer is not the same as party as the commodity seller is it? Because this would not be Shariah

compliant!

B: Sheikh, Sheikh – of course not. They are two different parties.

S: Ok, and tell me about this commodity, where does it come from?

B: It is metal that is quoted on the London Metal Exchange?

S: I see, and this is an international market with established norms and

B: Sheikh, Sheikh – of course not. They are two different parties.

S: Ok, and tell me about this commodity, where does it come from?

B: It is metal that is quoted on the London Metal Exchange?

S: I see, and this is an international market with established norms and

controls?

B: Yes

S: Tell me, how does the bank calculate the mark up, or profit, on the second transaction, when you sell the commodity to the customer

B: It is simply a % of cost, Sheikh. And the parties negotiate and agree and then execute this transaction.

B: Yes

S: Tell me, how does the bank calculate the mark up, or profit, on the second transaction, when you sell the commodity to the customer

B: It is simply a % of cost, Sheikh. And the parties negotiate and agree and then execute this transaction.

S: Ok, now tell me, when the customer sells the commodity in the third transaction, do you act as the agent for the customer, because this is questionable in Shariah, if you do this?

B: (coughing slightly) ANSWER 1 – well Sheikh, once the customer is the owner of the commodity

B: (coughing slightly) ANSWER 1 – well Sheikh, once the customer is the owner of the commodity

, he has the choice to keep the commodity, or to sell it. If they choose to sell it, we very kindly offer our services to help the customer arrange this. After all, we are here to serve.

ANSWER 2 – Sheikh, these are transactions on international markets, and it is a requirement

ANSWER 2 – Sheikh, these are transactions on international markets, and it is a requirement

that we act as agent for the customer in this transaction, because the customer is unable to execute his own transaction. We are here to serve.

S: Ok, great, that is very helpful. I am happy with your answers, this is Shariah compliant.

S: Ok, great, that is very helpful. I am happy with your answers, this is Shariah compliant.

OK, now let us imagine a conversation that I would prefer occurs between the scholar and the bank:

Scholar: This is a Murabaha transaction?

Bank: Yes

S: Where does the commodity come from originally?

Scholar: This is a Murabaha transaction?

Bank: Yes

S: Where does the commodity come from originally?

B: The commodity seller is the owner, and he sells it to the bank, and then-

S: Stop. Does the commodity seller have ownership of this commodity when he sells it to the bank?

B: But of course, Sheikh, how can he sell what he does not own?

S: And how does the seller get hold of

S: Stop. Does the commodity seller have ownership of this commodity when he sells it to the bank?

B: But of course, Sheikh, how can he sell what he does not own?

S: And how does the seller get hold of

this commodity?

B: Sheikh, he is a commodity trader and his business is to buy and sell. He holds inventory as part of his normal activities.

S: A trader on which market?

B: The London Metal Exchange

S: He is an approved trader on this exchange?

B: Sheikh, he is a commodity trader and his business is to buy and sell. He holds inventory as part of his normal activities.

S: A trader on which market?

B: The London Metal Exchange

S: He is an approved trader on this exchange?

B: erm….

S: And he has purchased this commodity on this exchange?

B: erm…

S: So if I examine his books, I will see a large inventory of commodity there, large enough that he can support the billions of dollars worth of trades he does every day?

S: And he has purchased this commodity on this exchange?

B: erm…

S: So if I examine his books, I will see a large inventory of commodity there, large enough that he can support the billions of dollars worth of trades he does every day?

B: erm…

S: OK, so now tell me about when you sell the commodity to the customer

B: Of course Sheikh, of course. We agree a price and we sell it at a mark up. And we disclose the mark up so that –

S: Shut up. Tell me how you calculate this mark up?

S: OK, so now tell me about when you sell the commodity to the customer

B: Of course Sheikh, of course. We agree a price and we sell it at a mark up. And we disclose the mark up so that –

S: Shut up. Tell me how you calculate this mark up?

B: Well, it is simply expressed as a % of cost. It really is very simple.

S: Like what, like 5% profit for example?

B: Yes, something like that

S: and when does the customer repay you back

B: In the future

S: When?

S: Like what, like 5% profit for example?

B: Yes, something like that

S: and when does the customer repay you back

B: In the future

S: When?

B: Ah this is a commercial agreement between us and the customer, you need not concern yourself with that

S: Shut up. Run me through a sample transaction and your pricing and the relevant repayment schedule.

After giving some real life examples

S: So, the longer the time you

S: Shut up. Run me through a sample transaction and your pricing and the relevant repayment schedule.

After giving some real life examples

S: So, the longer the time you

give for repayment, the higher the profit you make?

B: Erm, yes, because…

S: Quiet, and your desired profit rate is calculated with reference to an ANNUAL rate, not a fixed rate regardless of repayment duration?

B: Erm, yes, because…

S: Quiet, and your desired profit rate is calculated with reference to an ANNUAL rate, not a fixed rate regardless of repayment duration?

B: Erm, yes

S: And you obtain a promise from the customer to purchase the commodity from you - you receive this promise BEFORE you purchase this commodity?

B: Yes, of course, so that-

S: and this promise includes reference to the sale price and thus the profit you will make?

S: And you obtain a promise from the customer to purchase the commodity from you - you receive this promise BEFORE you purchase this commodity?

B: Yes, of course, so that-

S: and this promise includes reference to the sale price and thus the profit you will make?

B: Yes

S: And this profit is calculated with reference to a rate that is dependent on time value of money?

B: Erm…

S: Or perhaps it is linked to some form of LIBOR?

B: Erm…

S: This is impermissible. Next, tell me what the customer does with the commodity

S: And this profit is calculated with reference to a rate that is dependent on time value of money?

B: Erm…

S: Or perhaps it is linked to some form of LIBOR?

B: Erm…

S: This is impermissible. Next, tell me what the customer does with the commodity

B: Well, he can choose to keep it or –

S: Don’t be stupid.

B: But, Sheikh –

S: Why are you entering into all these transactions? Did the customer approach you for a loan and then you create these transactions in order to deliver the financing?

S: Don’t be stupid.

B: But, Sheikh –

S: Why are you entering into all these transactions? Did the customer approach you for a loan and then you create these transactions in order to deliver the financing?

B Well, yes, of course

S: So, if the customer did not approach you for the loan, then it is fair to say the customer had no intention of buying or owning such commodity?

B: Well-

S: Shut up. So, now you are seriously telling me that he might want to choose to KEEP this commodity

S: So, if the customer did not approach you for the loan, then it is fair to say the customer had no intention of buying or owning such commodity?

B: Well-

S: Shut up. So, now you are seriously telling me that he might want to choose to KEEP this commodity

once he has purchased it from you?

B: Well it is his choice, surely! It is his commodity. He can choose to do with it what he wants.

S: Ok, tell me the price he would pay for the commodity.

B: Well, Sheikh, it depends on many things, the market price, volatility, trading

B: Well it is his choice, surely! It is his commodity. He can choose to do with it what he wants.

S: Ok, tell me the price he would pay for the commodity.

B: Well, Sheikh, it depends on many things, the market price, volatility, trading

conditions-

S: Tell me the price – let’s say he wants a loan of £50k for one year and your profit rate is 5% per annum.

B: Well, if he pays it all back after one year, we can sell it to him for £52.5k and he can pay us back after one year.

S: So he will pay you £52.5k.

S: Tell me the price – let’s say he wants a loan of £50k for one year and your profit rate is 5% per annum.

B: Well, if he pays it all back after one year, we can sell it to him for £52.5k and he can pay us back after one year.

S: So he will pay you £52.5k.

And how much did you just buy this same commodity for?

B: Well, we would have paid £50k for it.

S: So why is the customer paying you above market price here? Why can he not just buy the same metal as you did and just pay 50k, like you did?

B: Well, Sheikh, we are trading on

B: Well, we would have paid £50k for it.

S: So why is the customer paying you above market price here? Why can he not just buy the same metal as you did and just pay 50k, like you did?

B: Well, Sheikh, we are trading on

on international markets, and the customer has no access to them-

S: So you purchased this commodity on the LME?

B: erm…

S: Thought so. Or did you just buy the metal in a private transaction which had nothing to do with the LME?

S: So you purchased this commodity on the LME?

B: erm…

S: Thought so. Or did you just buy the metal in a private transaction which had nothing to do with the LME?

B: erm…

S: Let’s move on. So the customer can choose to keep it (!) or he can sell it, yes?

B: Yes, Sheikh

S: How on earth will a retail customer know how to sell such commodity?

B: Well, we aim to serve, so we can help him here…

S: You will act as his agent in order for him

S: Let’s move on. So the customer can choose to keep it (!) or he can sell it, yes?

B: Yes, Sheikh

S: How on earth will a retail customer know how to sell such commodity?

B: Well, we aim to serve, so we can help him here…

S: You will act as his agent in order for him

to sell it?

B: Yes

S: This is impermissible

B: Normally yes, of course, but AAOIFI make allowances for international markets where the customer is thus required to request us to act as his agent

S: So this is a transaction on the international markets?

B: Yes

S: This is impermissible

B: Normally yes, of course, but AAOIFI make allowances for international markets where the customer is thus required to request us to act as his agent

S: So this is a transaction on the international markets?

B: Well, the metal is quoted on the LME

S: Does this transaction take place on the LME?

B: Well, no, Sheikh

S: Or is this a private transaction that takes place between two private parties?

B: Sort of…

S: Does this transaction take place on the LME?

B: Well, no, Sheikh

S: Or is this a private transaction that takes place between two private parties?

B: Sort of…

S: Then the exemptions provided by AAOIFI do not apply in this case, do they?

B: erm…

S: And it is impermissible for you to act as the customer’s agent when he sells the commodity.

B: erm…

B: erm…

S: And it is impermissible for you to act as the customer’s agent when he sells the commodity.

B: erm…

S: Ok, next. At what price do you think the customer can sell the commodity for?

B: Well, this is commodity that is quoted, and the price can move, so-

S: Shut up. If the loan he applies for is £50k, then will you arrange for him to sell the commodity for £50k

B: Well, yes

B: Well, this is commodity that is quoted, and the price can move, so-

S: Shut up. If the loan he applies for is £50k, then will you arrange for him to sell the commodity for £50k

B: Well, yes

S: Who will be the buyer?

B: Sheikh, this is a complex process, but we have knowledge of the markets and can arrange an expert buyer here

S: And this buyer is not the same party as the commodity seller, as this would be impermissible?

B: Certainly not Sheikh!

B: Sheikh, this is a complex process, but we have knowledge of the markets and can arrange an expert buyer here

S: And this buyer is not the same party as the commodity seller, as this would be impermissible?

B: Certainly not Sheikh!

S: So this buyer has no relationship with the commodity seller?

B: Sheikh, these are two separate commercial entities

S: That is not what I asked. Do these two parties have any agreement that governs their actions in this structure?

B: Well Sheikh, this is a commercial matter

B: Sheikh, these are two separate commercial entities

S: That is not what I asked. Do these two parties have any agreement that governs their actions in this structure?

B: Well Sheikh, this is a commercial matter

between them

S: OK, let me ask you this way. Have you signed a contract whereby you, and those two parties are all signatories? And where all agree to do certain things at certain times in order to ensure this structure works as described?

B: Erm…

S: OK, let me ask you this way. Have you signed a contract whereby you, and those two parties are all signatories? And where all agree to do certain things at certain times in order to ensure this structure works as described?

B: Erm…

S: Is it true that these two parties are known in the market to operate together, and that there are several pairs of such parties that offer their services jointly?

B: Erm… are you thirsty, Sheikh, maybe a nice cup of tea?

S: And that you agree to pay a fee for their services

B: Erm… are you thirsty, Sheikh, maybe a nice cup of tea?

S: And that you agree to pay a fee for their services

, and you negotiate that with one of these parties who then ensures the other party is paid from the same amount?

B: erm… we have some nice biscuits.

S: Right. What will the commodity buyer do with the commodity?

B: Sheikh, I have no idea, he is a trader and he can do

B: erm… we have some nice biscuits.

S: Right. What will the commodity buyer do with the commodity?

B: Sheikh, I have no idea, he is a trader and he can do

what he likes S: He is an authorised trader on the LME?

B: erm, well he is a broker

S: He an authorised broker on the LME?

B: (quickly wondering if these lists are made public, and realising that they are) – erm…

B: erm, well he is a broker

S: He an authorised broker on the LME?

B: (quickly wondering if these lists are made public, and realising that they are) – erm…

S: You know it is impermissible in this structure for the commodity to go back to the original seller, the commodity seller?

B: Well, yes, but-

S: Shut up. Is it true that this commodity buyer will return the commodity to the commodity seller?

B: erm…

B: Well, yes, but-

S: Shut up. Is it true that this commodity buyer will return the commodity to the commodity seller?

B: erm…

S: This is impermissible. Now let’s look again at this third transaction. The customer agrees to pay £52.5k for this metal?

B: Yes, don’t you think it’s a little warm in here?

S: And then he sells it for £50k?

B: Yes

S: So the customer is making a loss of £2.5k?

B: Yes

B: Yes, don’t you think it’s a little warm in here?

S: And then he sells it for £50k?

B: Yes

S: So the customer is making a loss of £2.5k?

B: Yes

S: Why would anyone rationally enter into trades in order to make a definite loss?

B: Sheikh, trading is a risky business -

S: So you can make a loss by holding onto assets and they fall in value. But the customer already knows and agrees he is going to make this loss?

B: Sheikh, trading is a risky business -

S: So you can make a loss by holding onto assets and they fall in value. But the customer already knows and agrees he is going to make this loss?

B: erm…

S: Tell me what happens if the customer does not purchase the commodity from the bank in the second transaction?

B: Sheikh, we are doing genuine trades, and we take some risk of loss here

S: Really? How so?

S: Tell me what happens if the customer does not purchase the commodity from the bank in the second transaction?

B: Sheikh, we are doing genuine trades, and we take some risk of loss here

S: Really? How so?

B: Well, the price can fall, we may be forced to sell the commodity on the open market at a loss – we take genuine risk as we are obliged to do.

S: Really? You would sell the metal back to the market at the prevailing market price?

B: erm…

S: But you just told me you did not

S: Really? You would sell the metal back to the market at the prevailing market price?

B: erm…

S: But you just told me you did not

not buy it on the open market. You did not buy it on the LME. You bought it in a private transaction, off market, with the commodity seller. So now you are telling me you will now sell it on the open market?

B: erm..

B: erm..

S: Do you have an agreement with the commodity seller, or buyer, to purchase the commodity from you at cost price in case you are unable to sell it to the customer?

B: erm…

S: As such, is it fair to say that you have no meaningful risk at all in terms of ownership and loss in

B: erm…

S: As such, is it fair to say that you have no meaningful risk at all in terms of ownership and loss in

value?

B: Sheikh! We own the metal. While we are the owners, we take risk-

S: Shut up. Once you have purchased the metal, how long do you own it for, prior to selling it? One day?

B: Sheikh, we take a view based on market risk, market conditions-

S: Uskut, how long? 6 hours?

B: Sheikh! We own the metal. While we are the owners, we take risk-

S: Shut up. Once you have purchased the metal, how long do you own it for, prior to selling it? One day?

B: Sheikh, we take a view based on market risk, market conditions-

S: Uskut, how long? 6 hours?

B: erm..

S: 1 hour?

B: erm…

S: 5 minutes?

B: erm…

S: 1 minute?

B: erm…

S: 1 second?

B: erm..yes? or shorter, if possible.

S: 1 hour?

B: erm…

S: 5 minutes?

B: erm…

S: 1 minute?

B: erm…

S: 1 second?

B: erm..yes? or shorter, if possible.

S: So you buy commodity that you have already received a promise from the customer to purchase from you, at a profit that is a function of libor and time value of money. You also have a guarantee to sell this metal back to the seller as a back up. You own the metal for less than

1 second. You then MUST be the agent to ensure the customer sells it only to the commodity buyer. The commodity buyer has a financial arrangement with the commodity seller to ensure the commodity returns to the original seller. These transactions do not take place on any market

. The commodity buyer and seller are not brokers on any exchange. All transactions are private. The customer is required to make a loss. You are giving him £50k and he is paying you back £52.5k, which are the same cash flows for a Riba loan at 5% per annum.

Each of these steps breaks at least one AAOIFI rule. And you are asking me for Shariah approval?

B: Sheikh, look at the time, I have a conference call now, I have to run. My secretary will be in touch to resume our conversation.

B: Sheikh, look at the time, I have a conference call now, I have to run. My secretary will be in touch to resume our conversation.

Banker goes to google to search for available Shariah scholars.

Now, THIS is how scholars should conduct their due diligence when approving contracts and structures.

Now, THIS is how scholars should conduct their due diligence when approving contracts and structures.

SUMMARY

Put a Shariah scholar who is not an expert in finance, markets and trading, in front of a banker who knows basic Shariah, you will likely get what the banker wants.

How do I know this?

Well, take a guess…

Put a Shariah scholar who is not an expert in finance, markets and trading, in front of a banker who knows basic Shariah, you will likely get what the banker wants.

How do I know this?

Well, take a guess…

Put a Shariah scholar who also knows about markets and trading (in great detail), then you will get more robust due diligence. If the scholar does not have this skill, then you MUST partner him with a finance expert who is NOT commercially aligned with the bank.

ALSO – I dare anybody to find a commodity Murabaha contract that claims it is in compliance with AAOIFI Shariah Standards. I have seen one that made this claim….but guess what : ) It was a false claim.

/THREAD

/THREAD