THREAD

Today I want to talk a bit about bonds.

Sure, they contain interest and are impermissible for Muslims, but it is crucial to understand the finance markets and how they operate, before you can hope to understand wider issues relating to Islamic bonds – Sukuk.

Today I want to talk a bit about bonds.

Sure, they contain interest and are impermissible for Muslims, but it is crucial to understand the finance markets and how they operate, before you can hope to understand wider issues relating to Islamic bonds – Sukuk.

Claiming to understand Sukuk without knowing about bonds is the height of ignorance.

OK, so a bond is simply a type of debt. The issuer of a bond receives money, and agrees to repay this same amount back to the investor in the future.

OK, so a bond is simply a type of debt. The issuer of a bond receives money, and agrees to repay this same amount back to the investor in the future.

In addition, bonds will pay a regular interest amount, or coupon.

This coupon can be fixed rate or floating. The bond will have a fixed duration, for example 5 years.

Question – why do we not see 1 year or 2 year bonds?

This coupon can be fixed rate or floating. The bond will have a fixed duration, for example 5 years.

Question – why do we not see 1 year or 2 year bonds?

NOTE – I know not all bonds have this duration, for example perpetual bonds, and not all bonds pay a coupon (Zero Coupon Bonds) but this explanation is intended to be high level

OK, why are bonds important to know about?

OK, why are bonds important to know about?

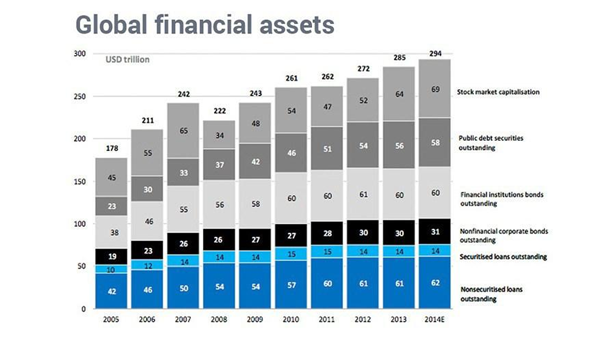

In 2014, bonds comprised around 51% of all global financial assets (Shares accounted for 23%), so they are literally huge in size.

Bonds are seen as more risky than cash deposits, but less risky (volatile) than stock markets and real estate. They have an important part to play

Bonds are seen as more risky than cash deposits, but less risky (volatile) than stock markets and real estate. They have an important part to play

play in the construction of a diversified portfolio for investors.

Ok, firstly, lets consider why an issuer may look to issue a bond as opposed to going to a bank for a direct loan.

Firstly, a loan is in fact preferred, if the duration is up to 1-3 years. For longer periods,

Ok, firstly, lets consider why an issuer may look to issue a bond as opposed to going to a bank for a direct loan.

Firstly, a loan is in fact preferred, if the duration is up to 1-3 years. For longer periods,

, bonds make more sense.

This is because, if you just get a bank loan, sooner or later you will use up your credit lines. Bonds enable an issuer to tap into a much wider investor base, such as funds, insurance companies, pension funds,

This is because, if you just get a bank loan, sooner or later you will use up your credit lines. Bonds enable an issuer to tap into a much wider investor base, such as funds, insurance companies, pension funds,

and also as a part of a diversified investment portfolio. This means an issuer has a higher chance of success in launching a bond.

Next, bonds are liquid instruments, that means that the owner of a bond can sell them on the open market. As we have seen, this market is huge.

Next, bonds are liquid instruments, that means that the owner of a bond can sell them on the open market. As we have seen, this market is huge.

. If a company takes a loan from a bank, it is much harder for the bank to sell off that loan in order to release capital.

Investors do have this option – they can quite easily trade in and out of bonds, either to release capital or to rebalance their portfolio.

Bonds are more

Investors do have this option – they can quite easily trade in and out of bonds, either to release capital or to rebalance their portfolio.

Bonds are more

more expensive to issue than a simple bank loan – there is documentation, and the launch process involves appointing investment banks to manage the process of launch and distribution.

As such, it makes little sense to issue small bonds, or bonds short in duration, as the fixed

As such, it makes little sense to issue small bonds, or bonds short in duration, as the fixed

cost element of issuance will then be too significant to absorb.

Ok, so a bond can have a fixed or floating rate coupon.

A fixed rate bond delivers the same amount of interest on a regular basis. The coupon can be 4% per annum, or 20% per annum. This will be paid regardless

Ok, so a bond can have a fixed or floating rate coupon.

A fixed rate bond delivers the same amount of interest on a regular basis. The coupon can be 4% per annum, or 20% per annum. This will be paid regardless

of the market price of the bond, and regardless of the global interest rate markets.

The coupon can be paid monthly, quarterly, semi annually, or annually.

NOTE – the coupon is expressed as a % of the face or par value of the bond, which is normally 100.

A floating rate means

The coupon can be paid monthly, quarterly, semi annually, or annually.

NOTE – the coupon is expressed as a % of the face or par value of the bond, which is normally 100.

A floating rate means

means the amount changes according to a specified benchmark. For example if the coupon is paid annually, the benchmark can be USD 12 month LIBOR.

Also, a spread is applied to reflect the credit risk of the issuer. A less risky issuer may only pay LIBOR +25 basis points, and a

Also, a spread is applied to reflect the credit risk of the issuer. A less risky issuer may only pay LIBOR +25 basis points, and a

more risky issuer may pay LIBOR +300 bp

(100 basis points = 1%)

Here we show the cash flows for a simple bond - can someone explain why the investor only paid $8,500 in this case and not face value (which is $10,000). This bond is paying 4% fixed rate.

(100 basis points = 1%)

Here we show the cash flows for a simple bond - can someone explain why the investor only paid $8,500 in this case and not face value (which is $10,000). This bond is paying 4% fixed rate.

This bond is paying 2.3% semi annually. In this case, the investor only paid 98.2 to buy it, and not 100.

How to value a bond?

Like all financial instruments, the value of a bond is simply the present value PV of all expected future cash flows.

How to value a bond?

Like all financial instruments, the value of a bond is simply the present value PV of all expected future cash flows.

Ok, trying to keep this simple.

If we are due to receive cash in the future, that is equivalent to receiving a LOWER amount today (the idea being that you can then deposit this lower amount in a risk free deposit to mature to the larger amount in the future).

If we are due to receive cash in the future, that is equivalent to receiving a LOWER amount today (the idea being that you can then deposit this lower amount in a risk free deposit to mature to the larger amount in the future).

So if we receive 100 in 5 years time, what is the PV today?

Well, we need to apply a discounting rate, and that depends on many things, such as the cost of funds and the interest rate environment. For example, if the annual interest rate is 5%, then we can place a deposit of 95

Well, we need to apply a discounting rate, and that depends on many things, such as the cost of funds and the interest rate environment. For example, if the annual interest rate is 5%, then we can place a deposit of 95

95 now, and receive (almost) 100 in one years time.

So we can say the PV of 100 is 95 (technically the PV of 105 is 100 but you get my point).

So, we have to look at all the future cash flows we are due to receive on a bond, and take the PV of EACH cash flow.

Then we add

So we can say the PV of 100 is 95 (technically the PV of 105 is 100 but you get my point).

So, we have to look at all the future cash flows we are due to receive on a bond, and take the PV of EACH cash flow.

Then we add

them all up and this is the expected value of the bond today.

PHEW, ok, let’s move on.

OK, so if the discount rate (market interest rate) is 5%, and the coupon is also 5%, then we can say that the bond should be priced at 100. That is because, this is really the same as

PHEW, ok, let’s move on.

OK, so if the discount rate (market interest rate) is 5%, and the coupon is also 5%, then we can say that the bond should be priced at 100. That is because, this is really the same as

placing a deposit of 100 with a bank at a rate of 5%.

Now, if the market rate was 4%, then the bond is paying more than market, so it is worth more than a deposit of 100 now, so the market value of the bond will be > 100.

Similarly, if coupon < market rate, then the value will

Now, if the market rate was 4%, then the bond is paying more than market, so it is worth more than a deposit of 100 now, so the market value of the bond will be > 100.

Similarly, if coupon < market rate, then the value will

will be <100.

Interest rates and bond prices

Now, let us consider how the price of a bond changes when interest rates change.

First of all, we have to see if the bond is paying fixed or floating rate. If it is a floating rate, there is no change in price. This is because the

Interest rates and bond prices

Now, let us consider how the price of a bond changes when interest rates change.

First of all, we have to see if the bond is paying fixed or floating rate. If it is a floating rate, there is no change in price. This is because the

the coupon is already designed to capture the new interest rate (plus the spread).

However, if the coupon is fixed rate, then the price of the bond WILL change when interest rates change.

OK, so let us assume a bond is paying 4% per annum, and the interest rates are also 4%

However, if the coupon is fixed rate, then the price of the bond WILL change when interest rates change.

OK, so let us assume a bond is paying 4% per annum, and the interest rates are also 4%

%, so this bond is trading at par value of 100.

Now, if the interest rates rise to 5%, the bond is still paying 4% coupon, which is $4. But if you place a deposit of $100 at a bank for 12 months, you would expect to get (in theory) 5% return. So the bond is now delivering a

Now, if the interest rates rise to 5%, the bond is still paying 4% coupon, which is $4. But if you place a deposit of $100 at a bank for 12 months, you would expect to get (in theory) 5% return. So the bond is now delivering a

a lower return than a $100 deposit. So it is worth LESS than this $100 deposit.

We can illustrate this simply, by saying we have to work out a price of the bond, when a $4 annual coupon would mean the investor is receiving a 5% return. We can see if the price of the bond moves

We can illustrate this simply, by saying we have to work out a price of the bond, when a $4 annual coupon would mean the investor is receiving a 5% return. We can see if the price of the bond moves

from 100 to 80, then the coupon of 4 now equates to 5% of the value of the bond.

In reality, it is more complicated, but this explains why a bond price falls when interest rates rise.

Conversely, the bond price rises when interest rates fall.

In reality, it is more complicated, but this explains why a bond price falls when interest rates rise.

Conversely, the bond price rises when interest rates fall.

Let us summaries some key aspects of bonds, now

1)Investor pays 100 to buy new bonds that are issued, par value 100.

2)Investor receives a pre agreed coupon, for the duration of the bond

3)Investor receives 100 when the bond matures and is “redeemed” by the issuer

1)Investor pays 100 to buy new bonds that are issued, par value 100.

2)Investor receives a pre agreed coupon, for the duration of the bond

3)Investor receives 100 when the bond matures and is “redeemed” by the issuer

Are bonds halal for Muslims?

No, as they pay interest.

Instead Muslims are allowed to invest in Sukuk, Islamic bonds.

However, if you think any aspect of a Sukuk is different to the key aspects of a bond, think again – they are designed, very carefully

No, as they pay interest.

Instead Muslims are allowed to invest in Sukuk, Islamic bonds.

However, if you think any aspect of a Sukuk is different to the key aspects of a bond, think again – they are designed, very carefully

, to behave in EXACTLY the same way as bonds, and thus MUST exhibit all the characteristics of bonds – INCLUDING the elements that are haram (Riba, interest).

There is much much more to bonds, and perhaps I will write another thread later about how bonds are used in financial markets

Thank you for taking the time to read.

/THREAD

Thank you for taking the time to read.

/THREAD

Unroll @threadreaderapp