1/ A Thread on Rebalance Timing Luck

- What is it?

- Does it matter?

- How do we solve for it?

- What is it?

- Does it matter?

- How do we solve for it?

2/ Rebalance Timing Luck ("RTL") is the unintended performance consequences due to the choice of when to rebalance a portfolio.

One might argue it is the result of unintended market timing.

One might argue it is the result of unintended market timing.

3/ AFAIK, it was first documented by Blitz, van der Grient, and @paradoxinvestor in their 2010 paper Fundamental Indexation: Rebalancing Assumptions and Performance (papers.ssrn.com/sol3/papers.cf…)

4/ Within, they demonstrate the performance dispersion that results due to the simple choice of when to rebalance a fundamental index portfolio.

5/ They suggest the use of "overlapping portfolios," achieved by equally dividing your portfolio into sub-portfolios that rebalance on different dates.

This is also called "tranching" or "staggered portfolios."

This is also called "tranching" or "staggered portfolios."

6/ @RA_Insights ultimately ended up implementing this exact solution: research.ftserussell.com/products/downl…

7/ As a side note, it is worth pointing out that while uncommon in public markets, this is a very common approach to implementing private investments.

Investors acknowledge market cycle risk and therefore tend to invest in multiple PE or VC funds over time to diversify the risk.

Investors acknowledge market cycle risk and therefore tend to invest in multiple PE or VC funds over time to diversify the risk.

8/ At Newfound, we first started writing about this effect back in 2013, having discovered it independently.

We wrote about it with respect to tactical portfolios, but over time appreciated that it affected almost *all* portfolios with a fixed rebalance schedule.

We wrote about it with respect to tactical portfolios, but over time appreciated that it affected almost *all* portfolios with a fixed rebalance schedule.

9/ Our research culminated in our paper "Rebalance Timing Luck: The Difference between Hired and Fired" which was published earlier this year

jii.pm-research.com/content/early/…

jii.pm-research.com/content/early/…

10/ We sought to address three points:

- Demonstrate that timing luck impacted something as simple as a 60/40 portfolio

- Prove that overlapping portfolios were the optimal solution

- Derivate an equation to estimate timing luck ex-ante

- Demonstrate that timing luck impacted something as simple as a 60/40 portfolio

- Prove that overlapping portfolios were the optimal solution

- Derivate an equation to estimate timing luck ex-ante

11/ The first was rather easy, and really only required us to generate different 60/40 portfolios rebalanced at different times in the year and plot the dispersion in their performance.

Remember: the only variable here is *when* portfolios are rebalanced.

Remember: the only variable here is *when* portfolios are rebalanced.

12/ Next, we proved that overlapping portfolios were an optimal solution.

I won't go into the proof here, but suffice it to say that I think the result is pretty intuitive. It's just diversification!

I won't go into the proof here, but suffice it to say that I think the result is pretty intuitive. It's just diversification!

13/ Finally, we wanted to derivate an equation for estimating the potential impact of timing luck.

The equation we derived is:

L = 0.5 x (T / F) x S

The equation we derived is:

L = 0.5 x (T / F) x S

14/ Here L is timing luck, T is annualized turnover, F is the # of rebalances that occur per year, and S captures how different our portfolio can be from one rebalance to the next.

15/ S is probably the hardest to interpret, so consider this example: a high turnover momentum portfolio.

If totally unconstrained, S will be very high. If highly constrained (e.g. implemented intra-sector), S will be much lower.

If totally unconstrained, S will be very high. If highly constrained (e.g. implemented intra-sector), S will be much lower.

16/ The intuition here is that high-turnover strategies, with few constraints applied, and which are rebalanced infrequently will have very high timing luck risk.

17/ I want to stress here that while the choice of rebalance frequency does impact timing luck, it should really be derived as a function of signal decay speed and cost.

e.g. a momentum portfolio likely has to rebalance more frequently than a value portfolio.

e.g. a momentum portfolio likely has to rebalance more frequently than a value portfolio.

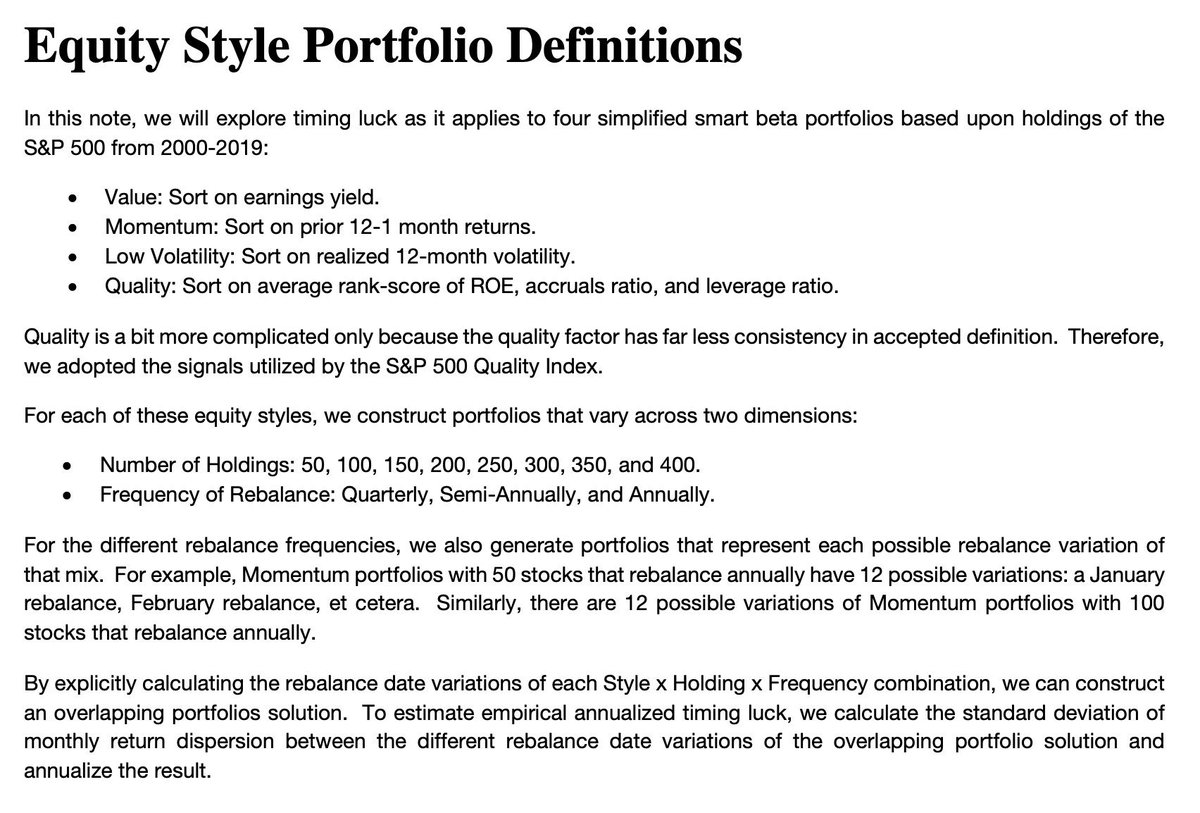

18/ In this week's commentary, I decided to tackle the empirical evidence of RTL's impact on smart beta returns by constructing 4 different styles, 8 concentration levels, and 3 different rebalance frequencies.

(Still with me? Here's a sneak peek: digioh.com/em/10484/17010…)

(Still with me? Here's a sneak peek: digioh.com/em/10484/17010…)

19/ Using these different portfolios, we can estimate the realized performance dispersion from a timing-luck-neutral implementation.

Our expectation is those strategies with higher turnover, less frequent rebalancing, and fewer constraints will exhibit more rebalance luck.

Our expectation is those strategies with higher turnover, less frequent rebalancing, and fewer constraints will exhibit more rebalance luck.

20/ And that's exactly what we found.

21/ But perhaps what is most staggering is the sheer magnitude of the timing luck here.

For a 100 stock value portfolio rebalanced semi-annually (hmm... sounds like most smart-beta products...), we're talking about 2.5% *per year.*

For a 100 stock value portfolio rebalanced semi-annually (hmm... sounds like most smart-beta products...), we're talking about 2.5% *per year.*

22/ And that's as measured against a timing-luck neutral benchmark. We need to multiple that by SQRT(2) to compare two non-neutralized portfolios.

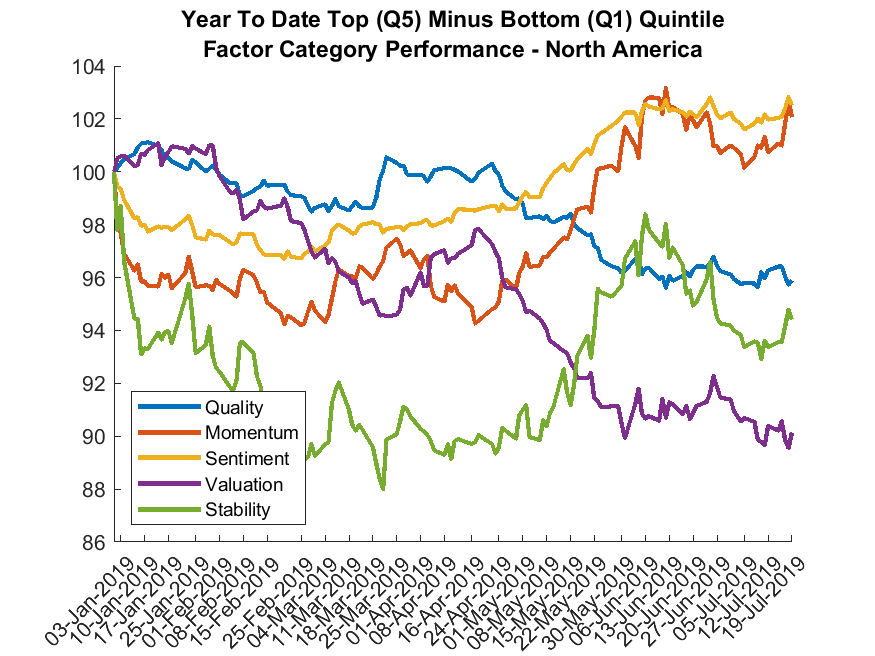

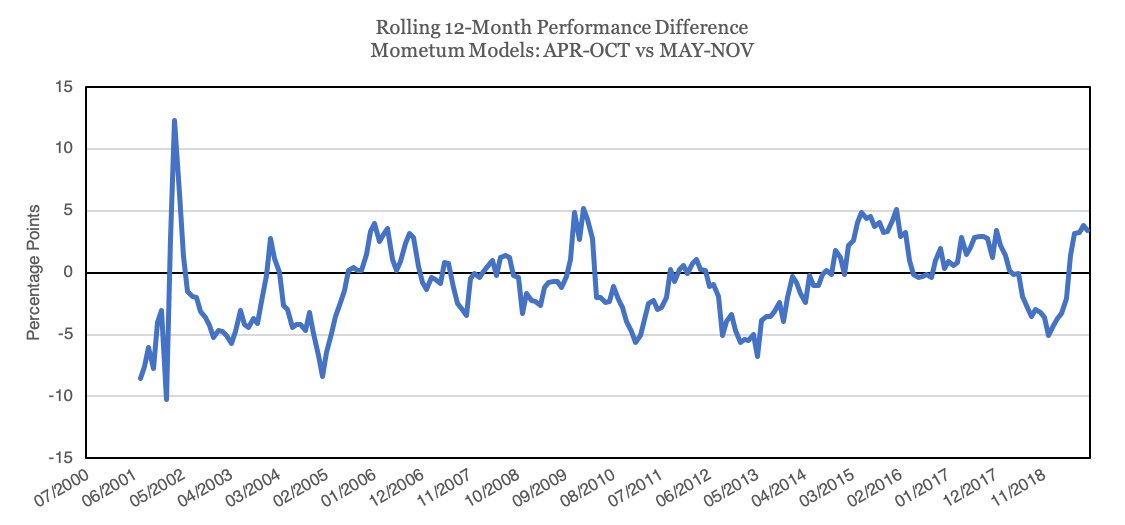

Just look at the dispersion realized in Momentum. We highlight the dispersion in the APT-OCT vs MAY-NOV implementations.

Just look at the dispersion realized in Momentum. We highlight the dispersion in the APT-OCT vs MAY-NOV implementations.

23/ But these are all hypothetical, right? Well, let's replicate some real-world examples.

Here are the various implementations of S&P 500 Enhanced Value, Momentum, Low Volatility, and Quality.

Here are the various implementations of S&P 500 Enhanced Value, Momentum, Low Volatility, and Quality.

23/ Perhaps the dispersion is made more clear by looking at their annual returns.

25/ The risk here is not really volatility, but a dispersion in terminal wealth.

Choose the wrong rebalance date and you end up with very, very different results.

Choose the wrong rebalance date and you end up with very, very different results.

26/ In conclusion: "when" is an under-discussed form of risk.

Or, put another way, "when" is a meaningful axis of diversification that we ignore at our own peril.

Or, put another way, "when" is a meaningful axis of diversification that we ignore at our own peril.

27/ I believe this evidence suggests that comparing strategies that are not timing-luck neutralized, or managers against benchmarks that are not timing-luck neutralized, is a fruitless endeavor.

Far too much noise comes from the impact of "when."

Far too much noise comes from the impact of "when."

28/ Some follow-up data Q&A I usually field.

Q: Are the results mean-reverting?

A: Augmented Dickey-Fuller tests suggest no. Random, but not mean reverting. This appears to be a totally uncompensated risk.

Q: Are the results mean-reverting?

A: Augmented Dickey-Fuller tests suggest no. Random, but not mean reverting. This appears to be a totally uncompensated risk.

29/

Q: What about seasonality?

A: Bootstrapped simulations suggest that there is no meaningful edge in selecting one rebalance date versus another.

But if there is, this data suggests the Sharpe is likely small.

Q: What about seasonality?

A: Bootstrapped simulations suggest that there is no meaningful edge in selecting one rebalance date versus another.

But if there is, this data suggests the Sharpe is likely small.