FYI, latest #PMI surveys undermine claims that #NIprotocol / SM membership is helping the Northern Ireland economy to outperform...

NI was the second weakest region In May, with the least optimistic outlook for the next 12 months... (1/3)

#BrexitReality

NI was the second weakest region In May, with the least optimistic outlook for the next 12 months... (1/3)

#BrexitReality

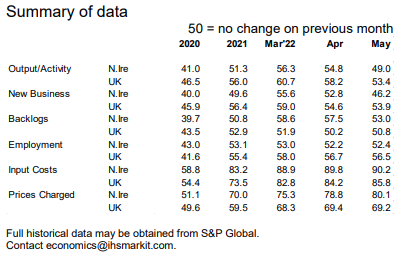

... detail shows Northern Ireland doing worse than the UK average on

❌ activity

❌ new business

❌ backlogs

❌ employment

❌ input costs

❌ prices charged (2/3)

❌ activity

❌ new business

❌ backlogs

❌ employment

❌ input costs

❌ prices charged (2/3)

... and this isn't a new development either 👇 (3/3)

sources: pmi.spglobal.com/Public/Home/Pr…

pmi.spglobal.com/Public/Home/Pr…

sources: pmi.spglobal.com/Public/Home/Pr…

pmi.spglobal.com/Public/Home/Pr…

• • •

Missing some Tweet in this thread? You can try to

force a refresh