Fyi, no serious economist - including Patrick Minford - would think that £30-£40 billion of tax cuts would mean UK interest rates have to rise to 7%... 🙄

#RishiSunak #LizTruss #LeadersDebate

#RishiSunak #LizTruss #LeadersDebate

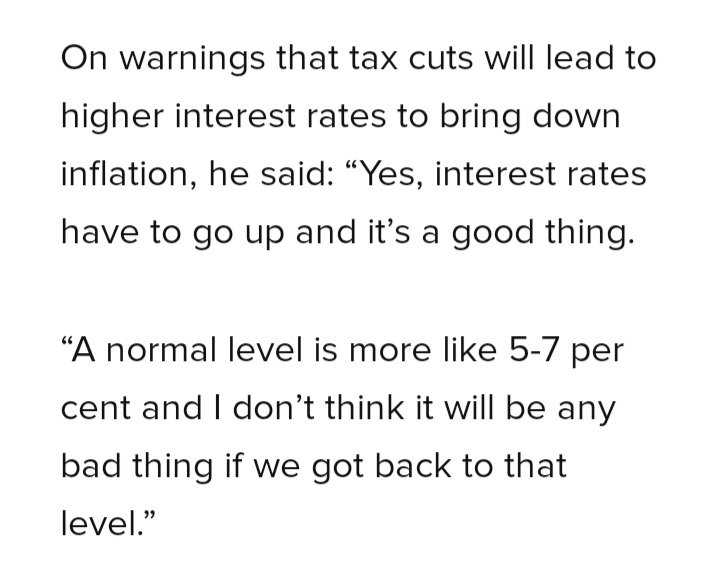

Ps. here's what #Minford actually said... 👇

(Most economists agree that UK interest rates are unsustainably low. In my view, the neutral rate would now be much lower than past norms of 5-7%. But Minford did NOT say that #Truss's tax cuts would raise them to 7%.)

(Most economists agree that UK interest rates are unsustainably low. In my view, the neutral rate would now be much lower than past norms of 5-7%. But Minford did NOT say that #Truss's tax cuts would raise them to 7%.)

pps. and since then (in a piece for the Mail), #Minford has clarified that he thinks the neutral rate is now more like 2-4%... 🤓

In short, poor from Rishi Sunak.

In short, poor from Rishi Sunak.

• • •

Missing some Tweet in this thread? You can try to

force a refresh