,

28 tweets,

3 min read

Read on Twitter

I shared this thread about myth of real estate investment yesterday. A few asked if I can mention other avenues to invest.

I am sharing some information / thoughts. Please note these are sourced from several online or print resources & from personal experience

In my opinion, nothing makes sense without a context. I am assuming some common denominators and giving some broad ideas.

There is no ‘Fill it, Shut it, Forget it‘ magic box of investment where you put your money, forget it & find a treasure after some years.

Let us discuss some of the common misconceptions. Savings, Investment and Insurance are three very different things

Savings is for short term. We save for purchases & emergencies. We put it in instruments that have low risk of losing value.

Investing is done to achieve long term goals like a retirement corpus or child’s higher education.

Insurance - The real purpose of life insurance is to help secure dependents financially in case of an unfortunate incident.

We should never combine Insurance and investment. Theoretically, insurance has nothing to do with investing.

Life cover policies come in different forms. The traditional endowment / money back policies on one side and Term policies on the other.

Traditional policies are badly structured. Most policies give a return of just 5-6% and invariably over a very long period say 20-30 years.

On the other hand pure Term insurance policies just address the insurance cover and are lot cheaper.

A combination of Term policy + PPF (Low risk) or Term policy + Mutual funds (if aggressive) can yield better insurance cover & returns

People who have already taken fresh policies and have not completed 3 yrs should just forget these payments and stop the premium payments.

The profits of switching from Endowment to “Term + MF” will be far greater than the loss from leaving Endowment policies .

People who have completed > 3 yrs - Either convert your policies to Paid-up or just surrender your polices and take the Surrender value

People near the Maturity - You have paid most of the premiums, so better stick with it, but insure yourself through a new term policy

I am not a fan of ULIPs. I always prefer to separate the insurance and investments. ULIP premiums are high. So are the charges

I know many who have committed to high insurance premiums. Along with Home Loan EMIs, this can adversely affect the monthly cash flows

After life insurance is taken care through a term policy, one should get a good Health Insurance policy for self and family

Only after these two steps *Life cover and Health insurance* are done, we can meaningfully discuss savings and investments

Next aspect is loans. If you have loans, it is advisable to repay / part prepay the loans instead of investing in other avenues

Prepaying a 9-9.5% loan Vs an expected return of 12% on investments may feel like a disadvantage but there are compelling reasons

The pressure of a liability hanging over the head makes the borrower uncomfortable. Prepaying loans is a better option,

Refinance your home loan at lower interest. Pay additional amounts over and above your EMI. Check

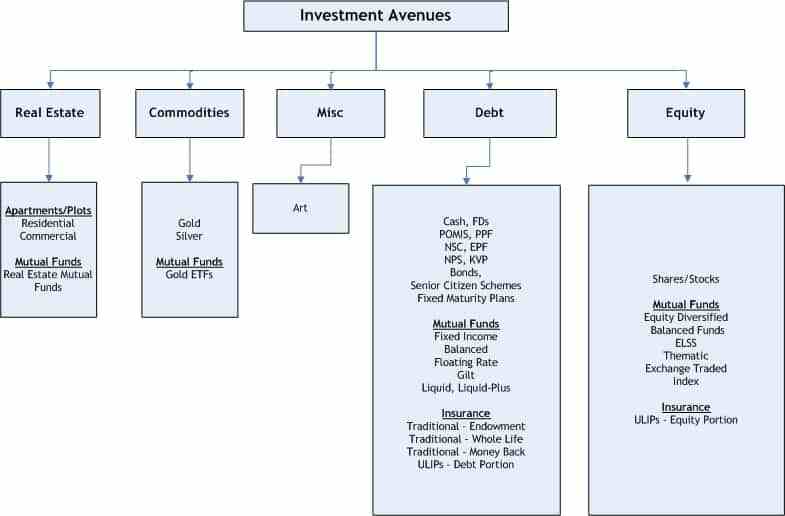

Now you are ready to evaluate the investment options. Investment avenues - got this pic courtesy wealthwisher

Some thumb rules -Combined EMIs of all loans should not be more than 45-50% of the total income, home liabilities not more than 35-40%

Next question is investments in Gold. Will continue the thread tomorrow. I will post tweet threads and will summarize as twitlonger later