,

64 tweets,

12 min read

Read on Twitter

Thread on How #Aadhaar linkage can destroy banks

# @RBI is empowered by the Payment and Settlement Systems Act, 2007 to regulate payment systems in the country. rbidocs.rbi.org.in/rdocs/Publicat…

’s mission for payment and settlement systems requires compliance to international standards

In compliance with international standards, therefore, all key systems should be secure & reliable

have access controls, be equipped with safeguards to prevent external intrusions, provide audit trails bis.org/publ/bcbs98.pdf

Electronic funds transfers includes point of sale transfers, ATM transactions,

direct deposits or withdrawal of funds, transfers initiated by telephone, internet and, card payment

For over a decade banks have used RBI’s own payment system NEFT to facilitate your online money transfers rbi.org.in/scripts/bs_vie…

Your money is transferred to the recipient's account in hourly schedules to settle payables & receivables from each bank from in that hour

In case, your transfer fails, your money is back in your account

If you make larger transfers, say Rs2 lakh and above, then you will have to use RBI’s RTGS to make the transfer rbi.org.in/scripts/FAQVie…

In this case the gross amount is moved from your account to the recipient account directly

In case the transaction fails your money is reversed back to you

You need to be logged into your bank account to initiate an NEFT or RTGS transfers

Only a valid bank account can receive funds making electronic transfers the bank and the trace of money cannot be altered

As NEFT & RTGS transfers leave a audit trail that cannot be altered they cannot be used for money laundering

Aadhaar-Enabled Payment System or AEPS facilitates deposit & withdrawal from Aadhaar-Enabled Bank Accounts (AEBA) authportal.uidai.gov.in/home-articles?…

AEPS must be licensed by @RBI under the Payment and Settlement Systems Act, 2007 rbidocs.rbi.org.in/rdocs/Publicat…

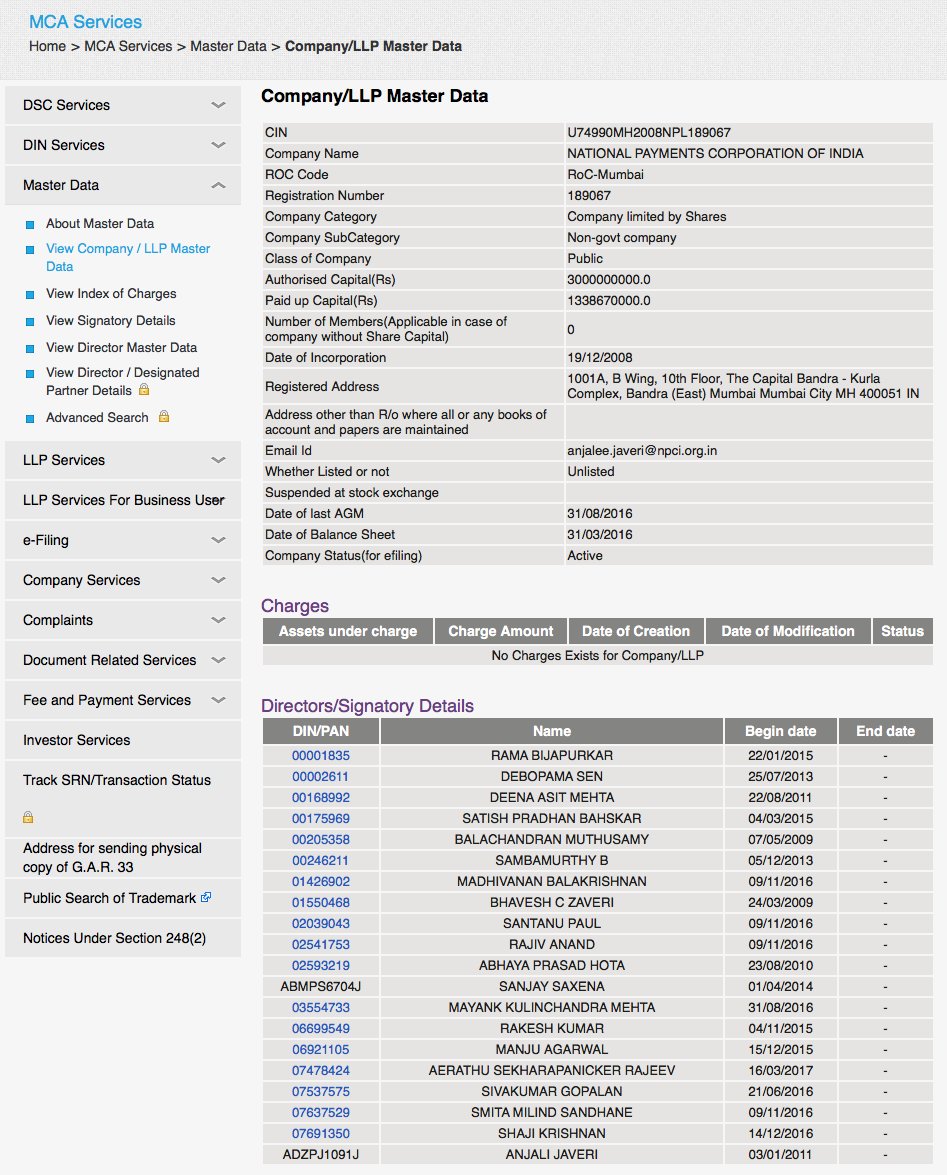

National Payments Corp of India or NPCI, a non government public company, runs the #Aadhaar Enabled Payment System (AEPS)

UIDAI has a MOU with NPCI. UIDAI has no responsibility for your transactions & NPCI has no obligation to @RBI uidai.gov.in/images/mou/par…

AEPS facilitates the withdrawal & deposit of money from AEBA accounts or bank accounts where an Aadhaar number is linked to the bank account

Linking #Aadhaar to a bank account is done through a process called as “seeding” an Aadhaar number to a bank account

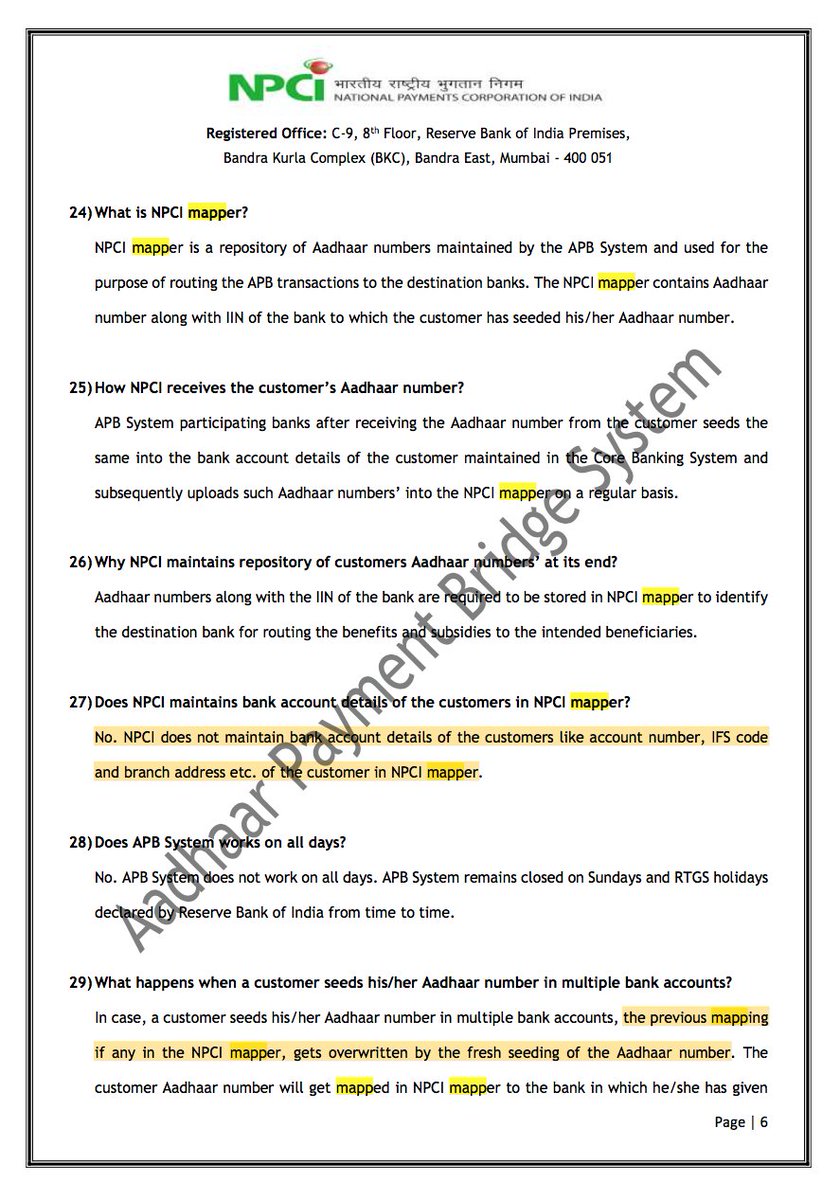

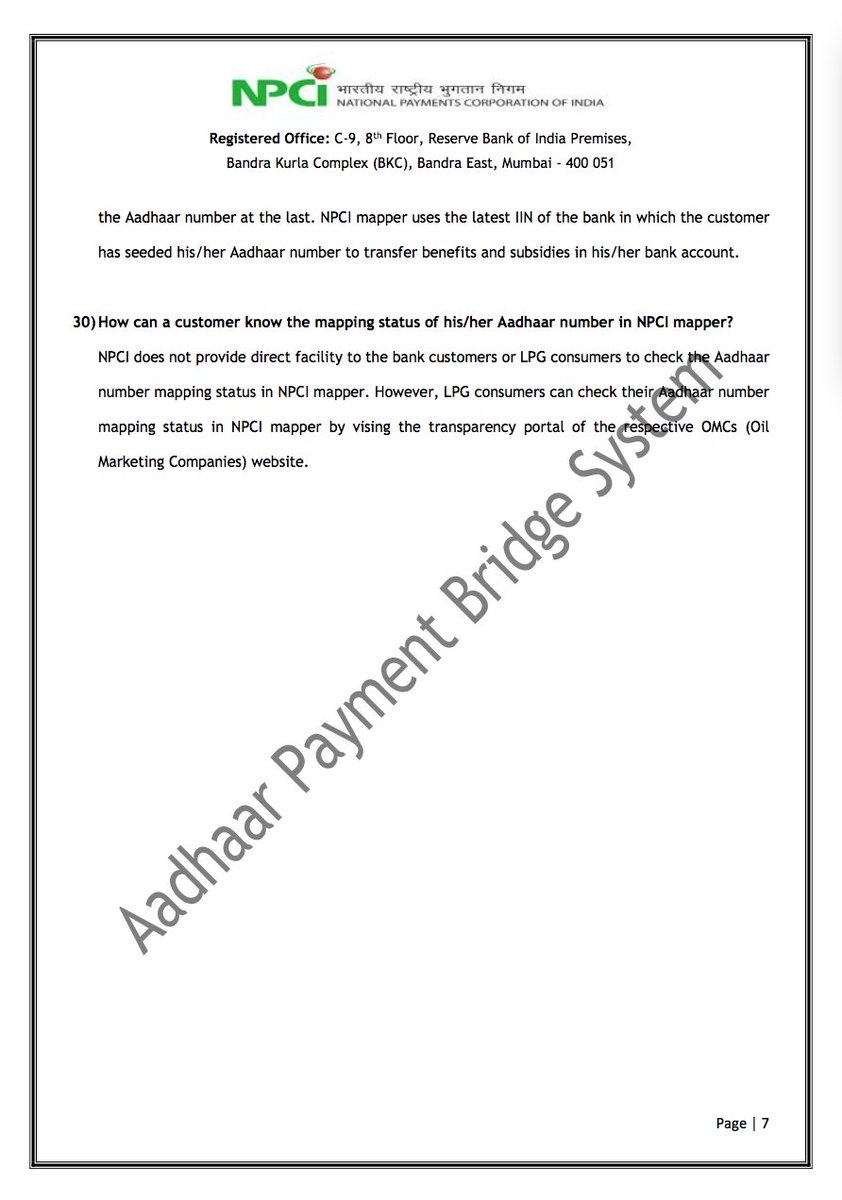

After receiving the Aadhaar number from the customer, the bank uploads such numbers’ into a “NPCI mapper” or a repository of Aadhaar numbers

The NPCI mapper is used for the purpose of routing transactions to the destination banks

The NPCI mapper contains Aadhaar number & IIN, a unique 6-digit number issued by NPCI to the participating bank npci.org.in/documents/Cust…

If anyone seeds a new bank AC with your #Aadhaar only that banks’ IIN will be associated with the Aadhaar iba.org.in/upload/MicroAT…

Once #Aadhaar enabled, you can make money transfers from your AEBA by providing the source and destination IIN and Aadhaar number

It is not impossible for anyone in possession of your #Aadhaar to open multiple accounts linked to your Aadhaar

It is therefore possible for alternate accounts to receive money transferred to your #Aadhaar

& then point the mapper back to your original account

This destroys the trace of which account the money was deposited to or even came from

Such un-traceability allows different accounts to “park” money at different times or even become conduits for money transfers

Such accounts can also become conduits to claim undeserved benefits from Consolidated Fund of India that would never be traced once released

Such a system would make it near impossible to detect fraud & crime

This is a recipe for embezzling government treasury with no complaints, no audit trail and no punishment

Bankers call any transactions that are not traceable as money laundering

# #AadhaarLeaks exposed hundreds of million #Aadhaar numbers & bank accounts that exposing them to such misuse

Even if Aadhaar numbers were proof of identity, which it is not, linking them to bank accounts is the best way to...

…park black money, make financial transfers unauditable, propagate money laundering and financial fraud

By enabling Aadhaar linkages with bank accounts, the government is enabling fraud propagation across the entire banking industry

...that will result in widespread and irreversible damage

PIL 932/2013 not heard since 2013 before the SC has challenged #Aadhaar linkages to banking and prayed for delinking Aadhaar from banking

If this investigation into #Aadhaar linkage is not sufficient to make a prudent banker lose sleep, we may not have any prudent bankers left

Do our policy makers have the time or inclination to apply themselves to protecting national interest & assets?

Or to reflect on the implications of their actions or to seek counsel & protect the nation and its assets?

Embroiling the unbanked & banked into this mess is no financial inclusion - it is a debt warrant

The government is subverting justice by not allowing the SC to hear & judge the matter

This is not a matter of deciding privacy, it is about national interest & our economy.

asserts that when impacts are not localized and non spreading, interdependence increases propagating impacts

This results in irreversible and widespread damage and the probability of devastation, ultimately to the point of certainty

#Aadhaar is propagating exactly such impacts that are not localised or non-spreading

Containing the nations risk from “black swans” requires applying the precautionary principle @nntaleb @yaneerbaryam fooledbyrandomness.com/pp2.pdf

An essential feature of a payment system is to guarantee the trace of payments should not be alterable

Another feature is that it should not be possible to freeze your bank account without recourse to redressal & justice

NEFT and RTGS are RBI’s own payment systems that have been time tested

There is no reason to switch public payments to any other payment system, particularly one run by non-government private companies

The replacement of a time tested standard under government regulation by a non-government company raises several questions…

…of public interest, propriety and conflict of interest

This thread is based on article previously published in Sep 2014 moneylife.in/article/how-aa… Scenario today worse as warnings have gone unheeded

The Aadhaar Act does not alter the questions raised in that PIL, they only get more serious

To know about how @RBI was undermined in causing #Aadhaar linkage for KYC, read sundayguardianlive.com/opinion/7100-p… Will do thread on that another time

Here is what the NPCI says about the Mapper

As @rossjanderson says, the problem is that when Alice guards a system & Bob pays the cost of failure, things break edge.org/conversation/r…

I just published “How does linking your Aadhaar to your bank account destroy the banking system?” medium.com/@anupamsaraph/…